KeywordsAerospace Cluster Competitive Advantage Index Competitiveness Industry

JEL Classification M16, O14, P42, P47

Full Article

1. Introduction

The diagnostic analysis of the aerospace sector highlights the potential of the industry in Mexico, whose level of exports has registered a yearly average growth of more than 16% during the period 2004-2015 and, in the last year, it reached an amount of 6,686 million dollars (Secretariat of Economy, 2017). In addition, there is a window of opportunity in terms of the global air traffic growth and the need to replace the commercial fleet. According to the Mexican Federation of the Aerospace Industry, A.C. (FEMIA for its Spanish acronym), approximately 38,000 aircraft will be necessary before the year 2034 representing a market value of 5,600,000 million USD dollars (FEMIA, 2018).

Mexico, with the growth of the global aerospace industry and the strategies carried out over the years, is emerging as a privileged destination for the development of the industry, where its manufacturing, engineering and development vocation gives it a high strategic value thanks to the quality and competitiveness of the workforce (Niosi and Majlinda, 2005).

Throughout the country, there are more than 300 companies related to this industry, 80% are manufacturing companies, 11% of them are engineering and the remaining 9% are maintenance and repair support companies. The companies of the aerospace industry that are established in Mexico, a foreign majority, are located in 18 states (Table 1), they employ more than 43 thousand people and generate an amount greater than 3 thousand 200 million dollars in exports.

Table 1. Geographic location of companies in the aerospace industry in Mexico

| Location (State) | Frequency | Percentage |

| Baja California | 71 | 23.66 |

| Sonora | 52 | 17.33 |

| Chihuahua | 35 | 11.67 |

| Querétaro | 41 | 13.67 |

| Nuevo León | 32 | 10.67 |

| Coahuila | 7 | 2.33 |

| Tamaulipas | 11 | 3.67 |

| San Luis Potosí | 5 | 1.67 |

| Yucatán | 3 | 1.00 |

| Puebla | 2 | 0.67 |

| Ciudad de México | 10 | 3.33 |

| Estado de México | 12 | 4.00 |

| Guanajuato | 3 | 1.00 |

| Jalisco | 12 | 4.00 |

| Others States | 4 | 1.33 |

| Total = | 300 | 100.00% |

Source: own, from data of PROMÉXICO (2015) and FEMIA, (2018).

Exports in the aerospace industry have reached record figures in recent years, reaching more than 4 billion dollars. Mexico manufactures components and assembles the structures for the most important suppliers, and aircraft and helicopter manufacturers in the world, such as: Airbus, Bombardier, EADS, Eurocopter, Boeing, General Electric, Zafran, Cesna, Hawker Beechcraf and Rolls Royce.

The Mexican Federation of the Aerospace Industry, A.C., states that the preliminary data for 2016 indicate that the country exported 7,200 million dollars, which represented a growth of around 10% (in relation to 2015). Among the main products and services in the country are:

- Components for Propulsion System

- Aerostructures (sheet metal)

- Components Landing Gear

- Precision Machining

- Plastic Parts

- Surface treatments

- Electrical and electronic systems

- Composite parts

- Engineering and design

- MRO services

Similarly, it is highlighted that 10 of the 20 most important companies in the world of aeronautics have established operations in Mexico, which has come to consolidate the aerospace industry, both for the commercial and military sector. In addition, a young supply chain has been detected with opportunities for greater integration to national supplying, since, currently, on average less than 6% of the suppliers of an assembly company for a given model have a presence in Mexico (FEMIA, 2018).

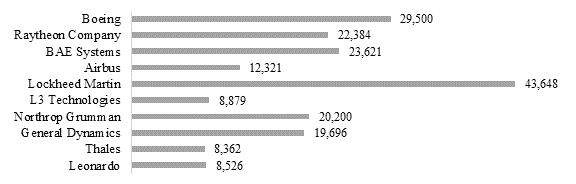

Thus, the top 10 places of the top 100 Global Aerospace Industry Defense Companies News 2017, are shown in Figure 1, where annual revenues are specified in millions of dollars, allowing to observe the expansion of the industry in Mexico.

Figure 1. Companies in the aerospace sector with operations in Mexico (Revenue in millions)

Source: Global Aerospace Industry Companies Defense News, 2017.

Finally, FEMIA proposes the following goals for the year 2020: that Mexico be among the 10 most important countries in the global aerospace industry, that the exports reach 12,000 million dollars, that there be more than 110,000 jobs and that 50% of the surplus balance value in trade balance be reached.

Statement of the Problem

Knowing that the five most representative states in terms of the grouping of 231 companies, representing 76.91% of the total number of companies and entities of the aerospace sector registered, it is important to mention that the state of Sonora includes 52 companies, equivalent to 17.33% of the national total. In that sense, it is imperative to calculate the Porter Competitive Advantage Index (IVC), to know the level of competitiveness of the companies of the aerospace sector of the state of Sonora.

It is necessary to increase the local certification capacity in order to attract companies from other sectors. Likewise, there must be a continuous supply of human talent to meet the needs of the aerospace industry. Similarly, regional comparative and competitive advantages should be optimized, such as geographical positioning, infrastructure connectivity, free trade agreements network, as well as the high capacity to react to immediate adaptation of products.

The research was based on two specific objectives:

1. The calculation of the competitiveness level of the companies in the aerospace sector at the state of Sonora, according to the Porter competitive advantage index (IVC) method;

2. In the analysis of the determinants of competitiveness according to primary information and company managers appreciation in the sector.

Both specific objectives, led to the achievement of the general objective: To develop a proposal based on the factors that determine the competitiveness of the Sonoran aerospace cluster for local producers who would wish to participate in the sector's value chain.

Based on the above, the following research question has been raised: what level of competitiveness does the aerospace sector represent for the state of Sonora?

2. Literature Review

The aeronautical sector is currently led by the two main global industries: Boeing and Airbus. Each of the related companies is supported by a considerable number of clusters due to the complexity and the arduous effort involved in the production of large-scale aircraft (Aguilera, 2010).

The growth of the national aerospace industry and its consolidation are an opportunity that is closely linked to the economic importance of the global aerospace sector. To achieve development in this industry, both in the state and in the country, government, industry and academia have been articulated to generate conditions and increase the existing capacities (Reyes and Vega, 2014).

The aerospace sector is responsible for the design, development, manufacture, assembly, marketing, repair and sale of aircraft. The product cycle consists of the development of design, manufacturing, assembly, testing and certification, and finally, maintenance activities (López, Elola, Valdaliso and Aranguren, 2012). Some specific features of this industry are:

- High scientific and technological intensity.

- High cost and risk programs.

- Long development cycles and a long return on investment.

- Production in short series and with high added value.

- International collaboration in design and development.

- Relevant role of the government as facilitator, customer, market regulator and defender.

- High market entry barriers.

- Critical importance of quality and safety.

- Very long life cycles and relationships between civil and military industry (Casalet, 2013; López et al., 2012).

The aerospace industry has activities around the world and is closely linked to global value chains where a small number of large companies with a high degree of specialization participate, which act as final consumers and those who request the activities carried out. In this industry, a low volume, and at the same time, a high mix of products with a high degree of planning, engineering and quality control are common and differentiated characteristics of this particular industry (Gomis and Carrillo, 2016).

2.1. The Aerospace Industry in Mexico

An exemplary case of progress and development, is precisely the Mexican Aerospace Cluster; which is developed based on the implementation of industrial strategies that involve the triple alliance (Government-academy-industry), promoting the joint work for the success of the aeronautical sector (Obregón, 2014). The Mexican aerospace industry began in the 50s and 90s through a series of unsuccessful efforts, executed by state entities not specialized in the sector, which conducted ineffective experiments. It was until 2010 that the sector was successful, following the creation of the Mexican Space Agency (AEM for its Spanish acronym, 2018).

The aeronautical industry in Mexico is recent, but its growth has been accelerated; this industry has become a strategic sector for national development, not only because of the investments it generates, but also because of the boost it gives to the generation of employment sources and technological development in the country. That is why Mexico has decided its growth by combining the efforts of federal and state governments, universities and companies in order to deploy the technical and infrastructure capabilities that allow manufacturing and designing products of the aeronautical sector in the country (Hernández, 2011).

This sector is becoming a strategic territory for European, American and Canadian aerospace industries, which, in the opinion of experts, will experience a great takeoff in the coming years, especially once that Mexico has obtained the authorization for the Bilateral Aviation Safety Agreement (BASA) of the U.S. Federal Aviation Agency (Hualde et al., 2007, p. 67).

The aerospace industry is composed of two large blocks: military aviation and civil aviation, the latter at the international level is divided into two large units: commercial aviation and executive aviation. For commercial aviation there are two main market niches, narrow-body or single-aisle aircraft and wide-body aircraft, while the executive or business type is made up of regional aircraft and executive jets (Airbus and Boeing, 2018).

The aerospace and aeronautical sector is considered strategic for economic development, since it is a relevant factor in terms of job creation and salary remuneration, which on average equals 1.5 times more than the rest of manufactures. It also maintains a strong link with other productive sectors, in such a way that it constitutes a development platform by generating a multiplying effect towards the related sectors (FEMIA, 2018).

The exports of the aeronautical industry reached 7 thousand 164 million dollars during year 2016, which meant a growth of 7.2 percent, with respect to the year 2015 and the expectation is that a positive behavior is maintained, driven mainly by the advance of passenger transportation flights (FEMIA, 2018). Of the total exports, 79 percent goes to the United States, while 73 percent of imports comes from this country, reflecting the interdependence of both economies.

2.2. Clusters in Mexico

Three specialized corridors have been established in the country (center, northeast and northwest) that place Mexico on the world stage as a viable regional cluster of the aerospace sector due to different factors. The interest in the Mexican cluster stems from the fact that it has been a potential sector that has presented an annual growth of 17.2% (Obregón, 2014).

- Baja California. According to information from the Secretariat of Economy (2017), the aerospace industry in this state has more than 76 companies focused on the sector, which register exports for more than 1,533 million dollars per year. The United States receives most of Baja California's exports; the rest goes to Canada, the United Kingdom, France, Germany, among other countries.

- Nuevo León. While the state of Nuevo Leon has more than 28 companies in the sector, which export their products mainly to the NAFTA market. This sector exports 651 million dollars per year.

- Chihuahua. In Chihuahua, there are more than 42 aerospace companies that generate 13,000 direct jobs in the industry, and a total of 1,500 million dollars of foreign and local investment. Among other capabilities, companies of composite materials, sheet metal, aerostructures, forging, smelting, thermal and surface treatments predominate. Exports of Chihuahua amounted to more than 1,000 million dollars per year. The main export destinations are the United States, Germany, France and Canada.

- Querétaro. The study of the Secretariat of Economy indicates that Queretaro has more than 30 companies in the aerospace sector, which register exports for 693 million dollars. The main exports of Querétaro are concentrated in merchandise for the assembly or manufacture of aircraft or aeroparts, turbojet engines of over 25 kN, landing gear and its parts, and goods destined for the repair or maintenance of aircraft parts or airplanes.

- Sonora. It houses one of the most important and integrated aeronautical machining clusters in the country. This entity has become a center of excellence for the manufacture of blades and components for turbines and aircraft engines (casting processes, machining, among others). It has more than 50 companies in the sector and exports about 190 million dollars, with the United States being its main export destination.

3. Research Methodology

The scope of the research is explanatory and proactive, using a mixed methodology; since a quantitative method was used to calculate the IVC, while the determinants of competitiveness are attributed to a qualitative method. In the first case, the IVC was quantified using information provided by the interviewees and statistics from the Secretariat of Economy of the State of Sonora. In the second case, the information obtained was processed through an in-depth interview where the opinion and assessment of certain factors that determine competitiveness for this type of company was requested through a Likert scale, and its processing was done using descriptive statistics.

3.1. Measurement, Research Instrument and Sample

The study required documentary research in a first stage and an arduous fieldwork in the second stage of the research project. The field work was carried out in five cities in the state of Sonora, where primary information was obtained from 30 companies (the sample size was determined using a population of 52 companies and with a confidence level of 90%), of a qualitative nature regarding the determinants of the competitiveness of the organizations visited, which was used to build the cluster model and quantitative information to measure the level of competitiveness of these companies and the cluster in general.

After achieving the application of the interviews, the information was captured in an Excel spreadsheet, for its data cleaning and transportation into the SPSS v.21 statistical program. In the Excel program, the competitive advantage index was calculated, while in SPSS crossed tables were built and trend measures were calculated to describe the main factors of competitiveness according to the opinion and assessment of the interviewees.

3.2. Data Collection

Next, the methodology used to calculate the competitiveness indices is explained, with the empirical data obtained.

Specifically, for the measurement of competitiveness, the methodology proposed by Porter (1991) was used, of the revealed competitive advantage index (IVC), which is currently a recurrent tool for measuring competitiveness. The sources of competitive advantage, in most of the literature, are based on the endowment of natural and labor resources. Porter, adopts a measure of competitive advantage calculated with the amount of exports, for an industry or by type of product. It is assumed that the exported amounts will increase and be competitive in international trade, among other things, due to low production costs and skilled labor. Therefore, competitiveness will be implicit in the increase of export amounts by sector or company. Specifically, the competitive advantage index of the aerospace sector in Mexico (IVCam) would be calculated, as shown in the following equation:

![]() (1)

(1)

Where:

Xam represents exports of the aerospace industry located in the country of Mexico; Xaw represents the world exports of the same product; Xm are the total exports of Mexico, and Xw are the total exports of the world. If the IVC is greater than one, then the aerospace industry located in Mexico will have an international comparative advantage.

The same reasoning was followed for the calculation of the IVC at company level of the aerospace sector, as can be seen in the following equation:

![]() (2)

(2)

Where:

Xae, are the exports of the company i belonging to the aerospace sector; Xae, are the total exports generated by the companies of the aerospace sector considered for this calculation; Xta, are the total exports of the aerospace sector of the State of Sonora, and Xts, are the total exports of the State of Sonora. With this last calculation, it will be possible to expand the analysis capacity, to mention an example, it will be possible to indicate which type of company within this sector is more competitive, that is, a higher competitiveness index in this industrial sector.

3.3. Hypotheses

The above, implies proving the first hypothesis:

H1 = If there is competitiveness in the companies that comprise the aerospace cluster of the state of Sonora

The condition for accepting the null hypothesis is that the IVC value calculated for most of the companies that comprise the cluster must be greater than one.

On the other hand, and according to Berumen, (2006), the competitiveness of companies depends on, among other things, the quality of the product, a competitive price, the degree of innovation and technological development and, where appropriate, the quality of the service. Returning to these theoretical arguments, a second hypothesis was raised.

H2 = The competitiveness of the companies in the aerospace cluster of the state of Sonora, is determined by the quality of the product, the price, the operating costs of the company, the degree of innovation of the product and the quality of the after sales service

To accept this hypothesis, it was necessary to calculate the central dispersion measures for each assessment assigned to the study variables by means of the Likert scale, and to determine that, those whose value is less than three, are relevant to competitiveness.

Finally, when analyzing the general significance of the applied instrument, the Cronbach's alpha index was greater than 0.7, which is why the criterion of validity and reliability of the measurement instrument's information is met.

4. Results

4.1. Business Competitiveness Index

This section shows the results of the competitive advantage indexes calculated for each of the 18 companies in the aerospace sector, which provided their information on the value of annual exports during the last year. The methodology section shows the equation used for the numerical generation of this indicator.

In some of the cases of the companies surveyed, the value of the IVC exceeds the value of one and in others its value is close to one, which makes it possible to generalize that this type of company is competitive. If the companies are grouped according to the value of their IVC and the activity to which they dedicate their production, the following findings were found.

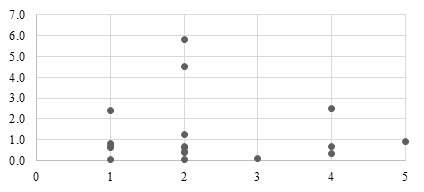

The following graph clearly illustrates how the activity of electronics is considered in this sector as the most competitive, since most of the companies in this field have a level of competitiveness close to or greater than one. However, it is necessary to remember that this type of company produces in a diversified way, that is, only a part of its production corresponds to products of the aerospace sector. Therefore, it cannot be assured that in terms of the level of exports, its competitiveness derives solely from the aerospace sector.

Figure 2. Dispersion of companies IVC by sub-sector

Source: Own. Sector 1 corresponds to metalworking, sector 2 to electronics, sector 3 to smelting, sector 4 to the activity of special processes and sector 5 to that of compounds.

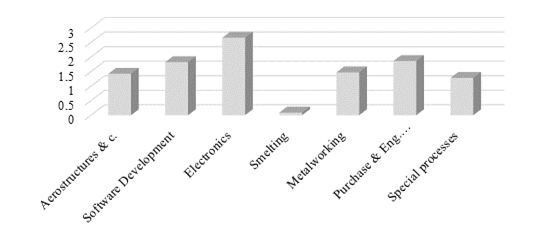

Additionally, an average IVC was generated by activity type, which confirms the trend shown in Figure 3. That is, the companies that perform activities related to electronics for the aerospace sector, apparently are more competitive than the rest of the companies. The above can be the result of the diversification conditions of this type of company, since historically, these companies were the first to settle in Sonora, also, the one which stated to export their production to a greater number of countries and, obviously, only a percentage of its production corresponds to the aerospace sector. Therefore, it is important to note that the activities of special processes and metalworking are and will be the activities that will sustain the growth of this sector in the future.

Figure 3. IVC Comparison by Company Activity Type

Source: Own.

The degree of diversification is decisive in the competitiveness of companies, since when associating the degree of diversification of the companies studied, with the value of the competitiveness index, it was found that the greater degree of diversification, the higher level of competitiveness. The degree of diversification was built through a binary variable, where the value of 1, was assigned to companies that had two or more countries as an export destination for their product; and the value of 0, for companies that send 100% of their exports to the United States of America.

4.2. Analysis of Descriptive Statistics to Establish Determining Factors of Competitiveness

To verify the second hypothesis, a simple qualitative analysis of the opinion of the executives of the companies visited was conducted, who provided assessment through a Likert scale, seven variables determining competitiveness. In this sense, a value of one is equivalent to the fact that the variable is an important factor, while five is equivalent to a non-important factor. The quantitative condition that must be met to assume that the analyzed variable is determinant of competitiveness in the aerospace sector of Sonora, is the following:

Value of the determinant meanx < 2.5

After capturing the opinions of the interviewees, the means and standard deviations of six determinants or variables were calculated, as shown in the following table.

Table 2. Mean of the competitiveness determinant variables

| Variable | N | Mean | Std. Deviation |

| Technology | 30 | 2.033 | 1.0334 |

| Government support | 30 | 3.100 | 1.4704 |

| Quality of post-sale service | 30 | 1.600 | 0.7240 |

| Guarantees offered | 30 | 1.733 | 0.9803 |

| Price of the product | 30 | 2.2667 | 1.36289 |

| Operation cost | 30 | 1.4667 | 0.73030 |

Source: Own.

As it can be seen, the variables that meet the quantitative condition are: Technology, Quality in the after sales service, Guarantees offered, Price of the product and Operating costs. It is not strange, that costs are a determinant of competitiveness, not only because it corroborates some previous publications and studies, but because some of the interviewees expressed that the decision to settle in Sonora and its industrial parks, was mainly due to the costs of establishing and operation, since one of the characteristics of dispersion of the companies in each of the cities, is associated with the contracting of the service of Shelter companies, who ensure the procedures of set up and rent of the infrastructure within the already consolidated industrial parks, which facilitates procedures and reduces costs for foreign companies.

On the other hand, the fixing of wages tends to be more flexible and in favor of workers, in cases where Shelter companies do not intervene with the outsourcing service, that is, in some companies installed in the cities of Nogales and Hermosillo, Sonora.

The newly established companies within this cluster, have specialized in the production of aerostructures. So it can also be inferred that the technological degree is decisive in the competitiveness of this conglomerate.

When analyzing the information obtained through in-depth interviews with the results of the assessment shown in Table 2, it is observed that companies with an extremely high technological level which value significantly the quality of the product, the service and the price, as determinants of competitiveness, makes them a very compact group, to which local suppliers will hardly be able to enter, since national companies wishing to enter as suppliers for this type of company will need to be highly innovative companies with the capacity to cover the highest standards of quality, demonstrate it through the obtaining of international certifications and with an optimal use of the resources that guarantee the fixing of a competitive price.

5. Discussion and Conclusion

The state of Sonora is considered one of the largest in Mexico, if to this we add that the aerospace cluster is distributed geographically in five cities and that their average distance may well be the diametrical distance of a small state like the State of Querétaro, it can be described in principle, that the aerospace cluster in Sonora is geographically wide.

The main cities where the installation of the 52 companies in this sector is concentrated, are five: Nogales, located to the north of the state, Hermosillo, Guaymas and Empalme in the center of the state, and finally, Ciudad Obregón located to the South. One of the dispersion characteristics of the companies in each of the cities is associated with the contracting of the service of Shelter companies, who insure the set up and rental procedures of the infrastructure within the consolidated industrial parks.

That is why the companies located in Empalme and Guaymas are the most representative of this case and therefore, show a greater degree of geographical concentration. Unlike Nogales, given the nature of the production and the year of start of operations of the companies in this sub-cluster, it is dispersed in different areas of the city.

When associating the type of activity or sub group of production of these companies, to the generation of employment, it was found that the industry or companies of the subgroup of electronics, located in the periphery (Nogales) of the cluster is the largest generator of employment. Which makes sense, considering that at a higher level and technological development, the greater the use of sophisticated machinery is, and therefore, the less use of labor is required. However, the type of labor required in the subgroup of aerostructures requires a higher level of specialization or training. Academically speaking, the minimum studies tend to be high school for the companies of the aerostructures group, while the electronics companies hire with a minimum of junior high school (secondary) studies.

On the other hand, the fixing of salaries tends to be more flexible and in favor of the workers, in cases where Shelter companies do not intervene with the subcontracting service. Namely, in some companies installed in Nogales and Hermosillo. And in the opposite case (they have a subcontracting service) are most of the companies located in Guaymas and Empalme.

Companies recently installed in the state, specializing in their production, with a single destination market for export, were classified as specialized emerging companies (EEE for its Spanish acronym), which are associated with the production of aerostructures and, to a lesser extent, with high precision machining and metal-mechanic. The companies installed in the state before 2006 and which have diversified their export markets, were classified as diversified consolidated companies (ECD for its Spanish acronym).

Although the companies of the electronics subgroup are not characterized by the use of a high technological level in their productive processes, it is important to mention that this is the industry with the highest generation of employment, historically with more presence in the state and that has sought to diversify its export market, as well as to adapt its production processes to meet the demand of the aerospace sector.

When analyzing the assessments of the determinants, performed by the managers of these companies, it was observed that there are three groups of companies that coincide in their way of seeing competitiveness. A first group is made up of companies that value the quality of the product, of service and price, as determinants of competitiveness, but which are characterized by producing a technological good that guarantees the placement of their offer. By relating this type of company with the opening period in our country, we can associate it with the classification of recently installed companies specialized in the production of goods from the aerospace sector. This group will seek to integrate new companies that only guarantee the provision of inputs with a high degree of innovation and technological development.

The second group is composed of companies that value the quality of the product and service, but do not consider that the price is determinant of competitiveness and at the same time they do not produce highly technical goods. This can be explained because a good number of them belong to the electronics sector, which are characterized by being consolidated companies (with greater seniority and experience) and the export destination of their production is diversified. That is, they seek to cover the demand of companies that need quality, more than price. If Mexican companies wish to join this type of cluster they will need to prepare themselves in terms of certifications, in order to comply with the international quality standards established for this type of companies and be accepted as suppliers in this value chain.

The third group is comprised by companies with a very high technological level, which significantly value the quality of the product, the service and the price, as determinants of competitiveness which makes it the most selective group. National companies wishing to enter as suppliers of this type of company, will need to be highly innovative companies, with the capacity to meet the highest quality standards, prove it through the obtaining of international certifications and with an optimal use of the resources that guarantee fixing a competitive price.

Finally, the results of this research confirm that the competitiveness of companies in the aerospace sector in Sonora is high and that their competitiveness is determined mainly by the technological development of their products, the quality of the service, the guarantees offered, the price and operating and production costs.

It can be concluded that there is a highly technological sector with export levels that turn them into competitive companies at the national level, according to the results corresponding to the competitive advantage index of the companies in the aerospace sector. Similarly, the values of the IVC by company, surpass the national average for this competitiveness.

5.1. Theoretical Contributions

The advantages in Sonora are reflected in low operating costs, high quality and low cost of labor, proximity to the main global aircraft market and government support; however, this sector lacks national, and much more local, certified suppliers.

The issue of generation of suppliers is very complex, since for their creation in the aerospace sector, the degree of demand for the quality of the products and the requested certifications is very high. Therefore, the participation of government institutions and advisory or consulting companies will be fundamental for the achievement of certifications by national and/or local companies. However, this may not be in the short term, since, currently, in the state of Sonora, companies in the aerospace sector use local suppliers exclusively for services such as: security, catering or food service, stationery, minor supplies, etc.; as well as other inputs that allow its operation as a company, but that are not incorporated in the production process to obtain the final product.

Then, how is it possible for national companies to integrate into the value chain within the aerospace cluster? To join the first group identified, national companies should consider that this type of conglomerate will seek to integrate new companies that guarantee the supply of inputs only with a high degree of innovation and technological development. Once again, the intervention of governmental institutions to promote investment and innovation, as well as research centers, will be decisive in the development of new national companies. Reason why it is suggested to strengthen the link between companies and universities, especially looking for technological institutes that, in coordination with Mexican companies, patent or register machinery and equipment, aimed at facilitating production processes in the aerospace sector.

In the second group, the presence of companies in the electronics sector stands out, which are characterized for being consolidated companies and having a diversified export destination of their production. That is, they seek to cover the demand of companies that need quality, more than price. If Mexican companies wish to join this type of cluster they will need to prepare themselves in terms of certifications, in order to comply with the quality standards handled in this type of cluster and be accepted as suppliers in this value chain. In this case, there is an area of opportunity for management and advisory companies in the field of international certifications such as ISO 9001, AS 9100 and NADCAP, who can offer their services to new national companies wishing to join this type of cluster and, thus, require to obtain this type of certifications to be considered as suppliers by foreign companies.

The third group is composed of companies with a very high technological level, which value significantly the quality of the product, the service and the price, as determinants of competitiveness, which makes the cluster more selective. The national companies wishing to venture as suppliers for this type of company, will need to be highly innovative companies, with the capacity to meet the highest quality standards, demonstrate it through the obtaining of international certifications and with an optimal use of the resources that guarantee the fixing of a competitive price. The challenge to enter this type of cluster is greater, so national companies wishing to join this type of cluster should prepare with a long-term vision and taking the previous suggestions as reference.

5.2. Managerial Implications

It is expected that in the future local companies that have an innovative and competitive offer, will be able to insert themselves in this production process and find markets in the national and international scope. In addition, these development opportunities are having an impact on the society of Sonora, since the set-up of research centers, training centers and universities to cover the labor demand of the aerospace sector has increased the study and work options. The generation of quality jobs is necessary in this sector due to the technological development of the aerospace industry, which requires skilled labor.

In terms of advantages, Sonora has comparative advantages, above all, qualified labor and low operating costs and set up of infrastructure. However, efforts should be channeled to generate competitive advantages. Reason why, it is concluded that according to the existing competitiveness in this industrial sector, the next step will be the generation of national suppliers that generate a true transfer of technology and industrial knowledge, for the regional development of the State of Sonora.

5.3. Limitations and Future Research

One of the limitations of the study was the lack of openness of the companies to respond to the structured interview and to the questionnaire that was developed with the purpose of gathering information from the sector. However, we thank the 30 companies that participated in the research. As a future line of research, one could consider conducting comparative analyzes between the 5 states of the country that are most representative with regards to aerospace activity and to determine which state has the highest competitiveness index.

References

- Agencia Espacial Mexicana (AEM), 2018. Catalogo y Análisis de Capacidades de Investigación y Desarrollo Tecnológico Espacial en México. [online] Available at: http://www.gob.mx/aem [Accessed 12 January 2018].

- Aguilera, C. M., 2010. Past, present and future of the Andalusian aeronautical cluster. España: Network-Centric Collaboration.

- Airbus, 2018. Airbus demonstrates 40 years of innovation and shaping efficiency. [online] Available at: http://search.proquest.com/docview/446139790?accountid=143348 [Accessed 31 January 2018].

- Berumen, S., 2006. Una aproximacion a los indicadores de la competitividad local y factores de la producción. Cuadernos de administración. Universidad Javeriana 19(31), pp. 145-163.

- Boeing, 2018. Boening. [online] Available at: www.boeing.com [Accessed 31 January 2018].

- Casalet, M., 2013. Actores y redes públicas y privadas en el desarrollo del sector aeroespacial internacional y nacional: el clúster de Querétaro, una oportunidad regional. In M. Caselet (Ed.). La industria aeroespacial: complejidad productiva e institucional, pp. 93-134, Mexico: Flacso.

- Federación Mexicana de la Industria Aeroespacial, A.C., FEMIA, 2018. Dirección General de Industrias Pesadas y de Alta Tecnología. [online] Available at: http://docs.google.com/viewer?url=http://femia.com.mx/themes/femia/ppt/femia_presentacion_tipo_esp.pdf [Accessed 6 February 2018].

- Global Aerospace Industry Companies Defense News, 2017. Global Aerospace Industry Companies Defense News [online] Available at: http://people.defensenews.com/top-100/ [Accessed 6 February 2018].

- Gomis, R. and Carrillo, J., 2016. The Role of Multinational Enterprises in the Aerospace Industry Cluster in Mexico: The case of Baja California. Competition & Change, 20(5), pp. 337-352.

- Hernández, J. 2011. Transfer of knowledge in the aerospace industry: the case of bombardier aerospace, Queretaro. Revista de Economía del Caribe, 7, pp. 231-269.

- Hualde, A. and Carrillo, J., 2007. La industria aeroespacial en Baja California: características productivas y competencias laborales y profesionales (1a. ed.). Tijuana, BC, México: El Colegio de la Frontera Norte.

- López, S. M., Elola, A., Valdaliso, M. M. and Aranguren, M. J., 2012. El clúster de la industria aeronáutica y espacial del País Vasco: orígenes, evolución y trayectoria competitiva. España: Euko Ikaskunta, Instituto Vasco de Competitividad, Fundación Deusto.

- Niosi, J. and Majlinda Z., 2005. Aerospace Clusters: local or Global Knowledge Spillovers? Industry and Innovation, 2(1), pp. 1-25.

- Obregón, Á., 2014. Industria aeroespacial mexicana mapa de ruta 2014. Ciudad de México: D.R. ProMéxico.

- Porter, M. E., 1991. La ventaja competitiva de las naciones. (Aparicio Martín Rafael Trad.). Barcelona: Vergara.

- PROCEI, 2015. PROMÉXICO. [online] Available at: http://mim.promexico.gob.mx/JS/MIM/PerfilDelSector/Aeroespacial/FC_Aeroespacial_ES.pdf [Accessed 28 January 2018].

- Reyes, N.I. and Vega, A., 2014. La innovación como factor de competitividad en la Industria Aeroespacial del Estado de Baja California, México. Productividad, Competitividad y Capital Humano en las Organizaciones, (1ª Ed.), pp. 525-534.

- Secretaría de Economía, 2017. Programa Estratégico de la Industria Aeroespacial 2012-2020. México, D.F.

Article Rights and License

© 2018 The Authors. Published by Sprint Investify. ISSN 2359-7712. This article is licensed under a Creative Commons Attribution 4.0 International License.