Keywordseconomic sustainability internal control frameworks internal control systems SMME SMME-specific internal control framework South Africa

JEL Classification M41, M42

Full Article

1. Introduction

Small, Medium, and Micro Enterprises (SMMEs) are generally dubbed as the “lifeblood” of economies around the globe (Ayandibu and Houghton, 2017; Masama, 2017). This is especially true in South Africa as SMMEs represent 90% of all businesses operating in the country, generate employment opportunities for approximately 60% of the national workforce, while simultaneously contributing between up to 57% to the national Gross Domestic Product (GDP) (Rungani and Potgieter, 2018; Setshedi et al., 2021). The importance of these business entities is substantiated by the most recent National Development Plan of South Africa where it is envisioned that South African SMMEs should be in a position to create 90% of all jobs by 2030 (Mulibana and Rena, 2021).

Notwithstanding the above, previous research studies (Bruwer et al., 2021; Sitole, 2021) suggest that prior to the CoronaVirus Disease 2019 (COVID-19), as much as 75% of South African SMMEs failed after being in operation for only three years. For reference, a COVID-19 outbreak commenced in late-2019 / early-2020 (Perold et al., 2020) and South Africa attached a “pandemic status” to this outbreak until April 2022. In more recent times, although the post-COVID-19 South African SMME failure rate is still unknown, it is anticipated to be greater than pre-COVID-19 levels (Singh, 2020; Mkhonza and Sifolo, 2022). Apart from the influence of COVID-19, previous research studies (Bruwer, 2016; Bruwer and Coetzee, 2016; Masama and Bruwer, 2018; Botha et al, 2020) suggest that the two most prevailing reasons for the high failure rate of South African SMMEs are 1) the unconducive economic environment of South Africa (e.g. increases in unemployment rates, decreases in economic productivity, and increases in poverty), and 2) the influence of economic factors on the economic sustainability of South African SMMEs (e.g. lack of scarce skills, lack of government support, lack of access to finance, increased interest rates, high inflation and unreliable supply of electricity). Referring to the work of Petersen (2018), South African SMMEs often have to operate in an environment that is synonymous with a “breeding ground for risks to realise”. According to research conducted by Bruwer (2023), the liability of newness also affects South African SMMEs considering that these business entities are mostly affected by having limited real/potential clients and having limited financial- and non-financial resources. To make matters worse, South African SMMEs have been found to “copy-and-paste” practices of established South African SMMEs without considering its pragmatic feasibility (Bruwer and Smith, 2021).

Taking into account the above, it becomes apparent that the objectives of South African SMMEs may not necessarily be achieved on account of a harsh socio-economic landscape, various socio-economic factors, having limited clientele, having limited resources, and following a one-size-fits-all approach with regard to business practices. One manner in which the latter can be addressed is through the implementation of a sound internal control system (Bruwer et al., 2018). For the sake of clarity, an internal control system is a “meticulous process … that should assist in the mitigation of risks, all with the intent to provide reasonable assurance surrounding the attainment of relevant organisational objectives in the foreseeable future” (Bruwer, 2016).

Research shows that, more often than not, internal control systems are built on the foundation of at least one established internal control framework (e.g. COSO internal control integrated framework, CoCo internal control framework and the COBIT framework) (McNally, 2013; Bruwer, 2016). Notwithstanding the latter, most established internal control frameworks in use today were specifically developed for large, established business entities (Yearwood, 2011). Thus, it is plausible that in the event SMMEs implement internal control systems from an internal control framework(s) that are non-SMME-specific, it could adversely influence the adequacy and effectiveness (soundness) of their internal control systems and, evidently, their economic sustainability (e.g. profitability, solvency, and liquidity).

Therefore, using the above as a basis the research problem identified within the ambit of this study is that South African SMMEs have internal control systems in place that do not provide them with reasonable assurance surrounding the attainment of their economic objectives in the foreseeable future. Alternatively stated, the internal control systems of South African SMMEs may be the raison d'être for their high failure rate and little to no research has been conducted in this regard. Therefore, the primary objective of this study was to determine the influence that internal control systems that are evident in South African SMMEs have on their economic sustainability.

For the remainder of this paper, content are provided and grouped under the following headings: 1) literature review, 2) research design, methodology and methods, 3) results and discussion, 4) managerial implications and recommendations, and 5) conclusion and 6) avenues for further research.

2. Literature Review

A literature review was deemed necessary to conceptualise applicable terminology while holistically contextualising the study. Therefore, the content under this heading is grouped under the following two sub-headings: 1) an overview of South African SMMEs, and 2) internal control systems and internal control frameworks.

2.1. An Overview of South African SMMEs

South African SMMEs were first recognised by national government in 1996 in the National Small Business Act No. 102 of 1996. The term “SMME” is defined as follows: “[A] separate and distinct business entity, including co-operative enterprises and non-governmental organizations, managed by one owner or more which, including its branches or subsidiaries, if any, is predominantly carried on in any sector or subsector of the economy …” (South Africa, 1996).

Since the formal recognition of these business entities, over the years, and to date, legislation governing South African SMMEs has been amended at total of three times. The most significant and most recent amendment took place in 2019 when the national government modified the classification criteria of SMMEs in terms of their size. According to this particular legislative document, SMMEs can be classified as “micro-enterprises”, “small-enterprises” or “medium-enterprises”, per sector and/or subsector, based on 1) the number of employees they employ on a full-time basis (i.e. between 0 and 10 full-time employees constitutes a “micro-enterprise”, between 11 and 50 full-time employees constitutes a “small-enterprise”, between 51 and 250 full-time employees constitutes a “medium-enterprise”) and/or, 2) their total annual turnover generated (South Africa, 2019: Bruwer et al., 2020).

Through a socioeconomic lens, SMMEs are indispensable to the South African economy, mainly due to their abilities to reduce unemployment, mitigate poverty, equally disseminate wealth, and boost the national economy (Vawda et al., 2013). Unfortunately, South African SMMEs are failing at an alarming rate - pre-COVID-19 statistics show that up to 75% fail in their first three years of existence (Masama, 2017; Fatoki, 2018). In addition, statistics pertaining to key national socio-economic indicators (e.g. unemployment rate, and the GDP per capita) also show a sharp decline over the years (Petersen, 2018; Renault et al., 2018; Bruwer, 2023) and, as such, the inference can be made that – at least in a theoretical sense – the South African SMME failure rate positively correlates to the holistic economic well-being of the country.

Regardless of the foregoing, though official South African failure rates post-COVID-19 are unknown, the failure rate of these businesses is potentially much greater when compared to pre-COVID-19 statistics (Faltein, 2021; Thamaha et al., 2021). This may likely be attributable to the limitations imposed on South African SMMEs (e.g. halting the operation of all businesses that provided non-essential product and/or services, curfews, and indoor customer limitations) by the national government when COVID-19 was still classified as a pandemic (Perold et al., 2020; Bruwer et al., 2020). Before COVID-19, the high failure rate of South African SMMEs was mainly attributed to an unconducive South African economic environment and the realisation of risks, as brought on by economic factors (Bruwer and Smith, 2018; Masama, 2017; Netshishive, 2021). Considering the destructive impact of COVID-19 on South African SMMEs (Ladzani, 2022), these business entities are now exposed to more risks than before.

According to previous studies (Masama and Bruwer, 2018; Masama et al., 2022), South African SMMEs do not properly manage their economic factors or their associated risks. These risks, in turn, can adversely affect the ability of South African SMMEs to achieve key economic objectives – i.e. their profitability (whether income is greater than expenditure), solvency (whether assets are greater than liabilities), liquidity (whether sufficient cash is on hand to pay current liabilities), and going concern (whether a business will remain in operation for the next 12 months) – often referred to as their economic sustainability (Luis et al., 2015; Petersen et al., 2020). In a South African SMME dispensation, economic sustainability is the most important type of sustainability to achieve on account that it directly impacts whether such a business entity will remain in operation for the foreseeable future or not (Bruwer and Petersen, 2022).

2.2. Internal Control Systems and Internal Control Frameworks

Considering the risks that South African SMMEs face on a daily basis, it is imperative for these business entities to mitigate them as far as possible. One manner in which this can be done is through the implementation of an internal control system. An internal control system is a process that aids in the mitigation of risks, while simultaneously providing reasonable assurance that relevant business objectives will be achieved in the foreseeable future (Sanusi et al., 2015; Okol, 2021). The responsibility for implementing an internal control system rests with management and it is critical that such a system is sound (Siwangaza, 2013; Bruwer, 2016). To assist management with this task, internal control frameworks can be used as a type of map to give guidance on the “how to” aspects to implement an internal control system. The three most widely-used internal control frameworks in existence that were developed for large business entities are that of the COSO internal control integrated framework, the CoCo internal control framework, and the COBIT framework, all of which are briefly expanded on below (Spira and Page, 2003; Tuttle and Vandervelde, 2007; Moeller, 2007; Savage et al., 2008; Fleak et al., 2010; Smit, 2012; Martin et al., 2014; Bruwer, 2016):

The COSO internal control integrated framework: This framework was established in 1992 and is regarded as the first-ever internal control framework. It was developed for large business entities to mitigate risks and to provide reasonable assurance surrounding the achievement of relevant business objectives. The most recent version of this framework comprises five interrelated components, namely: 1) control environment (the tone set at the top by management), 2) risk assessment (the manner in which risks are assessed), 3) control activities (the manner in which risks are controlled), 4) information and communication (the manner in which information is shared), and 5) monitoring activities (the manner in which internal control is monitored).

The CoCo internal control framework: This framework was first established in 1995 and built forth on the foundation set by the COSO internal control integrated framework. It was also developed for large business entities. Unfortunately, this framework did not gain much interest due to its complexity and it has not been updated since its first release. The CoCo internal control framework comprises four interrelated components, namely: 1) purpose (establishment of fundamentals), 2) commitment (ethical values of management), 3) capability (competence of all stakeholders), and 4) monitoring and learning (how internal control is monitored).

The COBIT framework: This framework was first established in 1996 and built forth on the foundation of the COSO internal control integrated framework. What sets this framework apart from the other two internal control frameworks is that it places more emphasis on the management of information and risks in an Information Technology environment. This framework emphasises four domains, namely: 1) planning and organising, 2) acquiring and implementing, 3) delivery and support, and monitoring.

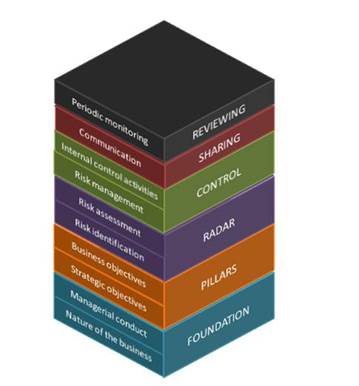

None of these internal control frameworks covered above were specifically developed for SMMEs. Although COSO (2005) made an effort to develop a guideline for internal control over financial reporting for smaller businesses entities, it was mostly applicable to public companies (equivalent to South African companies listed on the Johannesburg Stock Exchange). In 2012, the Risk Architecture Model was developed as a risk management model by Smit (2012) for Small and Medium South African enterprises – a first of its kind. Although related to internal control, no SMME-specific internal control framework existed before 2020 when Bruwer (2020) developed the Sustenance Framework. This framework is depicted below and briefly expanded on:

Figure 1. The Sustenance Framework

Source: Bruwer and Smith (2021)

The Sustenance framework: This framework was established in 2020 and was built on prior research studies that placed emphasis on the internal control evident in South African SMMEs. What makes this framework different from non-SMME-specific internal control frameworks is that it measures the control environment (the foundation of any internal control system) while providing hands-on guidance as to how to establish a customised internal control system in a SMME. This framework comprises six inter-related components, namely that of 1) foundation (the nature of the business and managerial conduct), 2) pillars (strategic objectives and business objectives), 3) radar (risk identification and risk assessment), 4) control (risk management and internal control activities), 5) sharing (communication), and 6) reviewing (periodic monitoring).

It should be noted that since the empirical feasibility of the Sustenance Framework has not yet been tested, this framework was not considered when developing the survey applicable to this research study. This framework is however important in the sense that its logic is later supported by the findings from the study.

3. Research Design, Methodology and Methods

This research study was empirical, positivistic and regarded as descriptive research. Essentially, descriptive research is defined as a research design whereby the characteristics of existing phenomena are described as accurately as possible (Atmowardoyo, 2018). In turn, descriptive research is mainly focused on the “what” of a research study as opposed to the “how” or the “why” of a research study (Nassaji, 2015). The latter was achieved by obtaining primary data form respondents.

Considering the positivistic research paradigm of this study, the best-suited research methodology was a quantitative research methodology. In particular, survey research was deployed as it assisted with the “provi[sion of] insight to individuals’ perspectives and experiences” by collecting “information from a sample of individuals through their responses to questions” (Alderman and Barbara, 2010; Tran et al., 2019). To assist with this, survey research was used.

It should be noted that this research study stems from a larger research study. The questionnaire was developed using the literature review of the larger research study as a basis and, for this paper, only nineteen closed questions (four multiple-choice questions, eight yes-no questions, and seven Likert-scale questions) and two fixed open-ended questions were used. This was done with the main intent to “conceptualise and re-conceptualise the key aims of the study and making preparations for the fieldwork and analysis so that not too much will go wrong and nothing will have been left out” (Oppenheim, 1992). The questionnaire from the larger research study was piloted against one statistician, three academics (holding at least a doctoral degree in the field of study), and two members of the general public. After piloting the questionnaire, relevant changes were made which, in turn, reasonably assured its face validity, construct validity, content validity and criterion validity. The questionnaire was self-administered by the researcher.

The targeted population of this research study was SMMEs operating in the fast-moving consumer goods (FMCG) industry. Considering that the population size was unknown, while also considering the time constraints and financial constraints of the researcher, non-probability sampling methods were used. In particular, a mixture of purposive sampling (where a researcher uses specific criteria to identify possible participants with the intent to glean rich data) and convenience sampling (where a researcher selects possible participants in close proximity, pending availability) were used (Leedy and Ormrod, 2005; Maree, 2020). Data were collected over a duration of two months in 2015 (before the COVID-19 pandemic and the development of the Sustenance Framework) through a data collection firm to eliminate research bias. All potential participants were ‘screened’ twice before they were formally approached to take part in the study. For the first round of ‘screening’, potential respondents had to adhere to the following delineation criteria:

- Be over the age of 18.

- Be a South African citizen.

- Be the owner, manager or owner-manager of a South African SMME.

- Have decision-making power in the applicable South African SMME (see point above).

- Be in the applicable position (see point above) for at least one year.

Out of the 150 respondents approached during the first round, 123 (82%) qualified as they adhered to the delineation criteria for the first round of ‘screening’. For the final round of ‘screening’, the South African SMMEs of first-round qualifying respondents had to adhere to the following delineation criteria:

- Operated in the FMCG industry.

- Be non-franchised.

- Operates in the Cape Metropole.

- Have been in existence for at least one year.

- Have between 0 and 50 full-time employees.

- Have an internal control system in place.

From the 123 respondents, only 99 (80.49%) adhered to the delineation criteria for the second round of ‘screening’. Apart from receiving ethical clearance from the Cape Peninsula University of Technology to conduct this research study (2015FBREC251), it was also subject to relevant ethical considerations (Spies et al., 2020). For this research study, every respondent was safeguarded from physical harm, provided his/her informed consent prior to taking part in the research study, was guaranteed anonymity and assured of his/her right to privacy, was assured of the confidential treatment of information provided.

Voluntarily agreed to partake in the study, and was informed that he/she could withdraw from the study at any time without being discriminated against.

4. Results and Discussion

Respondents were first asked a variety of demographic questions. These questions pertained mostly to the delineation criteria. A summary of the results is shown in Table 1 below:

Table 1. Summary of responses pertaining to demographic questions

| Question | Result |

| How would you describe your SMME? |

Sole trader: 76.8% Partnership: 7.1% Close corporation: 12.1% Private company: 4.0% |

| Is your SMME franchised? | No: 100% |

| How many full-time employees does your SMME employ? |

Between 0 and 10: 85.8% Between 11 and 50: 14.2% |

| How long has your business existed (in years)? |

Minimum: 2 years Maximum: 60 years Mean: 8.4 years Median: 5 years Mode: 5 years |

| Does your SMME operate in the FMCG industry? | Yes: 100% |

| What is your position in your SMME? |

Owner: 31.3% Manager: 37.4% Owner-manager: 31.3% |

| How long have you been in this position? |

Minimum: 1 year Maximum: 3 years Mean: 2 years Median: 2 years Mode: 2 years |

| What is your highest qualification? |

Lower than Grade 12: 16.2% Grade 12: 48.5% Certificate: 14.1% Diploma: 12.1% Bachelor’s degree: 8.1% Honours degree: 1.0% |

| Do you have decision-making power in your SMME? | Yes: 100% |

Source: Author’s own

From the statistics in Table 1, the inference can be made that the average respondent was a manager of a non-franchised South African FMCG SMME who had an average of 2 years of managerial experience while having completed Grade 12. In turn, the average non-franchised FMCG SMME that was owned and/or managed can be described as a micro, sole trader business that has been in existence for 8.4 years.

Next, respondents were asked about their internal control systems. Respondents were first informed what an internal control system is by sharing the following paragraph: “An internal control system is a progress that is implemented by management, be it formal or informal, to help prevent risks from realising, to help detect risks when they realise (loss events) and to correct loss events. It also helps a business achieve its operational objectives, compliance objective and reporting objectives”

Following this, respondents were asked whether their SMMEs, to the best of their knowledge, had an internal control system. After all respondents indicated “yes”; they were asked about the particular internal control framework they used to implement it. From the results:

- 37.9% of respondents used the COSO internal control integrated framework.

- 18% of respondents used the CoCo internal control framework.

- 9.7% use the COBIT framework.

- 17.2% used other internal control frameworks.

- 17.2% of respondents used no internal control frameworks.

Thus, a total of 82.8% of respondents indicated that they made use of internal control frameworks to develop their internal control systems. When respondents who indicated that they “used other internal control frameworks” were asked to elaborate, no comprehensive answers were provided. For transparency, in the larger research study, respondents were asked to describe the characteristics of their internal control systems through a checkbox question. In most instances, respondents selected characteristics which did not correspond to how internal control systems were conceptualised in the larger study, as well as this study (e.g. not informal or formal, not a process, not implemented by management, does not help with risk management of risk, and does not help the business achieve its objectives). Considering this, the author deduced that respondents did not, in fact, conceptualise an internal control system as per literature and hence no further investigation took place to understand why respondents responded in the manner they did above.

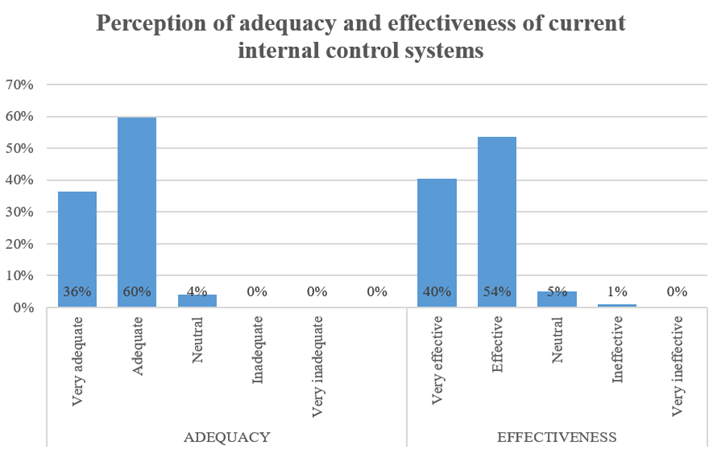

Next, respondents were asked to provide their views on the soundness (i.e. adequacy and effectiveness) of their existing internal control systems by means of a 5-point Likert scale question. A summary of the results is shown in Figure 1 below:

Figure 1. Perception of adequacy and effectiveness of current internal control systems

Source: Author’s own

Stemming from the results above, it is evident that the adequacy and effectiveness of existing internal control systems, in sampled SMMEs, were perceived as mostly adequate and effective. This was quite surprising considering that the bulk of respondents indicated that they based their internal control systems on non-SMME-specific internal control frameworks. To provide insight as to the perceptions of respondents surrounding the perceived adequacy and effectiveness of the internal control systems, a cross-tabulation was performed (see Table 2 below).

Table 2. Summary of responses pertaining to demographic questions

| Element | Based on COSO | Based on Coco | Based on COBIT | Based on other | Based on nothing | SUM |

| ADEQUACY | ||||||

| Very adequate | 11.00% | 9% | 6.90% | 7.60% | 2.10% | |

| Adequate | 25.50% | 9% | 2.80% | 9.00% | 13.80% | |

| Neutral | 1.40% | 0.00% | 0.00% | 0.60% | 1.30% | |

| SUM | 37.90% | 18.00% | 9.70% | 17.20% | 17.20% | 100% |

| EFFECTIVENESS | ||||||

| Very effective | 11.00% | 11.70% | 6.90% | 7.50% | 2.80% | |

| Effective | 25.50% | 5.00% | 2.10% | 6.90% | 12.30% | |

| Neutral | 0.70% | 1.30% | 0.70% | 2.80% | 2.10% | |

| Ineffective | 0.70% | 0.00% | 0.00% | 0.00% | 0.00% | |

| SUM | 37.90% | 18.00% | 9.70% | 17.20% | 17.20% | 100% |

Source: Author’s own

Taking into account the results above, the inference can be made that regardless of the internal control framework used to develop the internal control systems of these SMMEs, the perceived adequacy and effectiveness of their existing internal control systems were viewed in a positive light. In addition to the latter, it should be noted that respondents did not conceptualise an internal control system as per literature. For this reason it may be that the internal control systems evident in these SMMEs may not necessarily help prevent risks from realising, help detect loss events when they occur, correct loss events after they have occurred, or assist with the achievement of relevant economic objectives.

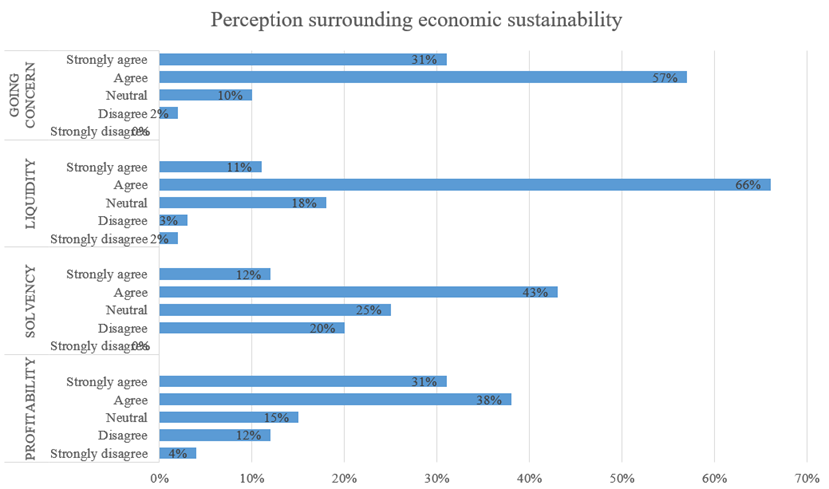

To better understand the economic sustainability of respondents SMMEs, respondents were asked to provide their views on their business entities’ profitability, solvency, liquidity and going concern status. A summary of the responses received is shown in Figure 2 below:

Figure 2. Perception surrounding economic sustainability

Source: Author’s own

From the summary in Figure 5, it becomes evident that respondents favourably viewed the economic sustainability of their SMMEs. The inference can be made that SMMEs were profitable 69.0% of the time; solvent 55.0% of the time; liquid 77.0% of the time; regarded as a going concern 88.0% of the time.

Since the SMMEs of respondents were perceived to achieve their key economic objectives (between 55.0% and 88.0% of the time) it led to the question: “Does the adequacy and effectiveness of existing internal control systems, of these SMMEs, contribute favourably towards their economic sustainability?” To answer this question, a two-tailed Pearson correlation was performed on the data received. The results are summarised in Table 3 below:

Table 3. Pearson correlations surrounding the perceived adequacy and effectiveness of internal control systems in SMMEs and their perceived economic sustainability

| Element | Profitability | Solvency | Liquidity | Going concern | |

| Adequacy | Correlation | -0.411** | -0.256** | -0.201* | -0.095 |

| Sig. | 0.000 | 0.010 | 0.050 | 0.351 | |

| Effectiveness | Correlation | -0.190 | -0.218* | -0.051 | -0.080 |

| Sig. | 0.059 | 0.030 | 0.617 | 0.433 |

Source: Author’s own

Of the eight tested relationships, four were found to be statistically significant – two being significant at the 99% level and two being significant at the 95% level. For the sake of clarity, each of the four statistically significant relationships is listed and discussed below:

- Adequacy and profitability: When the adequacy of internal control systems of sampled SMMEs increased, it had a moderate, negative statistically significant influence on profitability (β = -0.411; p-value = 0.00).

- Adequacy and solvency: When the adequacy of internal control systems of sampled SMMEs increased, it had a weak, negative statistically significant influence on solvency (β = -0.256; p-value = 0.01).

- Adequacy and liquidity: When the adequacy of internal control systems of sampled SMMEs increased, it had a weak, negative statistically significant influence on liquidity (β = -0.201; p-value = 0.05).

- Effectiveness and solvency: When the effectiveness of existing internal control systems of sampled SMMEs increased, it had a weak, negative statistically significant influence on solvency. (β = -0.218; p-value = 0.03).

From the Pearson correlation performed, it becomes evident that the internal control systems of sampled SMMEs did, for the most part, not assist with the attainment of economic sustainability. This view is justified by four non-statistically significant relationships (between adequacy and going concern; effectiveness and profitability; effectiveness and liquidity, and effectiveness and going concern), and the four statistically significant negative relationships mentioned above. This result also corresponds with the fact that respondents understanding of internal control systems were disparate compared to existing literature; as conceptualised within the ambit of this study.

5. Managerial Implications and Recommendations

Most respondents rated the internal control systems of their SMMEs as adequate and effective. From the research conducted however, it becomes apparent that these internal control systems are not contributing towards the attainment of these business entities’ economic sustainability. It should be noted that the importance of an adequate and effective internal control system rests in its ability to prevent risks, detect loss events, and correct loss events. The results of this study are therefore in line with previous studies however (Masama and Bruwer, 2018; Masama et al., 2022) in the sense that South African SMMEs have difficulty in the management of their applicable risks. This may also have to do with the fact that respondents’ views of internal control systems were not in line with literature. The analogy can therefore be drawn that where sampled SMMEs were regarded as going concerns by respondents, such business entities remained afloat by chance. Specifically, when the adequacy and/or effectiveness of sampled SMMEs’ internal control systems increased, it either had a statistically significant negative influence on their economic sustainability or no statistically significant influence at all. Alternatively stated, sampled SMMEs are more likely to remain economically sustainable without their current internal control systems.

An adequate and effective internal control system should provide management with reasonable assurance surrounding the attainment of objectives, including the prevention of risks, detection of loss events, and correction of loss events. To this end, sampled SMMEs need to re-evaluate their current internal control systems and/or establish new internal control systems. One manner in which this can be accomplished is by going back to the proverbial drawing board to redesign their internal control system based on SMME-specific internal control frameworks, one of which is the Sustenance Framework.

6. Conclusion and Avenues for Further Research

SMMEs are of grave socio-economic importance to South Africa. These business entities provide employment opportunities to a large proportion of the national workforce while also contributing a significant proportion to the national GDP. Notwithstanding the latter, these business entities, unfortunately, have among the highest failure rates in the world. Two main reasons for the high failure rate of South African SMMEs are the unconducive South African economic environment, and the realisation of risks, as brought upon by economic factors. Bluntly stated, South African SMMEs operate in a “breeding ground” where risks can easily realise.

To combat risks, sound internal control systems can be used. Not only does it assist in the mitigation of risks, but it also provides reasonable assurance surrounding the achievement of business objectives. While the onus is on management to implement an internal control system, the most popular internal control frameworks that are used as guidelines by SMMEs have been developed for large business entities.

From the research conducted, it is evident that although the adequacy and effectiveness of internal control systems of sampled SMMEs were perceived in a good light, they did not have any statistically significant influence on sampled South African SMMEs’ achievement of economic sustainability. This may be attributable to the fact that respondents, based their business entities’ internal control systems on internal control frameworks that were not specifically designed for SMMEs.

In fundamental nature, from the research conducted, it is suggested that South African SMMEs need to go back to the proverbial drawing board and re-design their internal control systems based on SMME-specific internal control frameworks. From the research conducted, the following avenues for further research are suggested, which are not limited to:

- Using the Sustenance Framework to enhance the adequacy of internal control systems of South African SMMEs.

- Using the Sustenance Framework to enhance the effectiveness of internal control systems of South African SMMEs.

- The influence of internal control systems, as developed on the Sustenance Framework, in South African SMMEs, on economic sustainability.

---

Conflicts of Interest: The authors state that they have no conflicts of interest.

References

- Alderman, A. and Barbara, S., 2010. Survey research. Plastic and Reconstructive Surgery, 126(4), pp.1381-1389. doi: 10.1097/PRS.0b013e3181ea44f9

- Atmowardoyo, H., 2018. Research Methods in TEFL Studies: Descriptive Research, Case Study, Error Analysis, and R & D. Journal of Language Teaching and Research, 9(1), pp.197-204. doi: http://dx.doi.org/10.17507/jltr.0901.25

- Ayandibu, A.O. and Houghton, J., 2017. The role of small and medium scale enterprise in local economic development (LED). Journal of Business and Retail Management Research, 11(2), pp.133-139. doi: https://jbrmr.com/cdn/article_file/i-26_c-262.pdf

- Botha, A., Smulders, S.A., Combrink, H.A. and Meiring, J., 2020. Challenges, barriers and policy development for South African SMMEs – does size matter?. Development Southern Africa, 38(2), pp.153-174. doi: 10.1080/0376835X.2020.1732872

- Bruwer, J.-P. and Coetzee, P., 2016. A literature review of the sustainability, the managerial conduct of management and the internal control systems evident in South African small, medium and micro enterprises. Problems and Perspectives in Management, 14(2), pp.201-211. doi: http://dx.doi.org/10.21511/ppm.14(2-1).2016.09

- Bruwer, J.-P., 2016. The relationship(s) between the managerial conduct and the internal control activities of South African fast moving consumer goods SMMEs. Doctoral degree, Cape Peninsula University of Technology.

- Bruwer, J-P. and Petersen, A., 2022. The perceptions of South African Small, Medium and Micro Enterprise Management on occupational fraud risk, economic sustainability and key employee characteristics: What are the relationships?. Journal of Accounting, Finance and Auditing Studies, 8(4), pp. 29 - 58. doi: 10.32602/jafas.2022.026

- Bruwer, J-P., 2020. The Sustenance Framework, Nova Publishers, New York, NY.

- Bruwer, J-P., 2023. The relevance of the liability of newness in a post-COVID-19 South African Small, Medium, and Micro Enterprise dispensation. International Conference on Business and Management Dynamics, 27 - 28 September 2023, Cape Town, South Africa (in press).

- Bruwer, J-P. and Smith, J., 2021. The Sustainability of Newly Established Business Entities: The Sustenance Framework. Expert Journal of Business and Management, 9(2), pp.75-87.

- Bruwer, J-P. and Smith, J., 2018. The Role of Basic Business Skills Development and Their Influence on South African Small, Medium and Micro Enterprise Sustainability. Journal of Economics and Behavioral Studies, 10(2), 48-62. doi: https://doi.org/10.22610/jebs.v10i2(J).2216

- Bruwer, J-P., Mabasele, L., Benting, V., Cloete, J., Jacobs, C., Marais, J., Rabalao, K and Spangenberg, M., 2021. The Theoretical Link Between Cash Flow Statement Usage and Decision Making In South African Small, Medium and Micro Enterprises. International Journal of Business Research Management, 12(4), pp.191-204. doi: https://www.cscjournals.org/manuscript/Journals/IJBRM/Volume12/Issue4/IJBRM-298.pdf

- Bruwer, J-P., Perold, I. and Hattingh, C., 2020. Probable Measures to Aid South African Small Medium and Micro Enterprises’ Sustainability, Post-COVID-19: A Literature Review [online]. Available from: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3625552 [Accessed 20 April 2023].

- Bruwer, J-P., Siwangaza, L. and Smit, Y., 2018. Loss Control and Loss Control Strategies in SMMEs Operating in a Developing Country: A Literature Review. Expert Journal of Business and Management, 6(1), pp. 1-11. doi: https://business.expertjournals.com/23446781-601/

- COSO., 2005. Guidance for Smaller Public Companies Reporting on internal Control over Financial Reporting [online]. Available at: https://www.icjce.es/images/pdfs/TECNICA/C03%20-%20AICPA/C311%20-%20Estudios%20y%20Varios/COSO%20-%20ED%20re%20IC%20Guidance%20-%20Oct%202005.pdf [Accessed on 20 June 2023].

- Faltein, N., 2021. The challenges and survival strategies for black SMMEs in Nelson Mandela Metro during COVID19. Master’s Degree, Nelson Mandela University.

- Fatoki, O., 2018. The impact of Entrepreneurial Resilience on the Success of Small and Medium Enterprises in South Africa. Sustainability, 10(1), pp.1-12. doi: https://doi.org/10.3390/su10072527

- Fleak, S.K., Harrison, K.E. and Turner, L.A., 2010. Sunshine Center: an instructional case evaluating internal control in a small organization. Issues in Accounting Education, 25(4), 709-720. doi: https://doi.org/10.5555/1558-7983-25.4.1

- Ladzani, M.W., 2022. The impact of COVID-19 on small and micro-enterprises in South Africa. International Journal of Global Environmental Issues, 21(1), pp. 23-38. doi: doi.org/10.1504/IJGENVI.2022.122935

- Leedy, P.D.O. & Ormrod, J.E., 2005. Practical research: Planning and design (8th Edition). Prentice Hall, New Jersey, NJ.

- Luís, A., Lickorish, F. and Pollard, S., 2015. Assessing interdependent operational, tactical and strategic risks for improved utility master plans. Water Research, 74(1), pp. 213-226. doi:10.1016/j.watres.2015.02.021

- Maree, K., 2020. First Steps in research (3rd Edition). Van Schaik, Pretoria.

- Martin, K., Sanders, E. and Scalan, G., 2014. The potential impact of COSO internal control integrated framework revision on internal audit structured SOX work programs. Research in Accounting Regulation, 26(1), pp.110-117. doi: https://doi.org/10.1016/j.racreg.2014.02.012

- Masama, B. and Bruwer, J-P., 2018. Revisiting the Economic Factors which Influence Fast Food South African Small, Medium and Micro Enterprise Sustainability. Expert Journal of Business and Management, 6(1), pp.19-28. doi: https://business.expertjournals.com/23446781-603/

- Masama, B., 2017. The utilisation of Enterprise Risk Management in Fast-Food Small, Medium and Micro Enterprises operating in the Cape Peninsula. Master’s degree, Cape Peninsula University of Technology.

- Masama, B., Gwaka, L. & Bruwer, J-P., 2022. The feasibility of implementing the COSO ERM framework in South African SMMEs: A literature review. International Journal of Business Continuity and Risk Management, 12(3), pp. 208-225.

- McNally, J.S., 2013. The 2013 COSO framework and SOX compliance: one approach to an effective transition. Strategic Finance [online] Available at: http://www.coso.org/documents/COSO%20McNallyTransition%20Article-Final%20COSO%20Version%20Proof_5-31-13.pdf [Accessed on 17 August 2023].

- Mkhonza, V.M. and Sifolo, P.P., 2022. Investigating small, medium and micro-scale enterprises strategic planning techniques in Johannesburg central business district post-COVID-19 lockdown. Southern African Journal of Entrepreneurship and Small Business Management, 14(1), pp.1-13. doi: https://doi.org/10.4102/sajesbm.v14i1.483

- Moeller, R.R., 2007. COSO Enterprise risk management: understanding the new integrated ERM framework, John Wiley, Hoboken, NJ.

- Mulibana, L. and Rena, R., 2021. Innovation activities of informal micro-enterprises in Gauteng, South Africa: A systematic review of the literature. African Journal of Science, Technology, Innovation and Development, 13(4), pp.1-11. doi: https://journals.co.za/doi/full/10.1080/20421338.2020.1818921.

- Nassaji, H., 2015. Qualitative and descriptive research: Data type versus data analysis. Language Teaching Research, 19(2), pp.129-132. Doi: https://doi.org/10.1177/1362168815572747

- Netshishive, C., 2021. The challenges impacting the growth of small-, micro- and medium-sized textile enterprises (SMMEs): A case of Ekurhuleni Metropolitan Municipality. Master’s degree, University of the Free State.

- Okol, E., 2021. Internal Control Systems and Financial Performance of Institution of Higher Learning: A Case of Uganda Colleges of Commerce. Master’s degree, Kyambogo University.

- Oppenheim, A.N., 1992. Questionnaire design, interviewing and attitude measurement, Printer Publishers, New York, NY.

- Perold, I., Hattingh, C. & Bruwer, J-P., 2020. The forced cancellation of four jewel events amidst COVID-19 and its probable influence on the Western Cape economy: A literature review (working paper BRS/2020/002) [online]. Available from: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3604132 [Accessed on 13 July 2023].

- Petersen, A., 2018. The Effectiveness of internal control activities to combat occupational fraud risk in fast-moving consumer goods Small, Medium and Micro enterprises (SMMEs) in the Cape Metropole. Master’s degrees, Cape Peninsula University of Technology.

- Petersen, A., Bruwer, J-P. and Mason, R., 2020. Source Document Usage and the Financial Sustainability of South African Small, Medium and Micro Retailers. Expert Journal of Business and Management, 8(1), pp.110-119. Doi: https://www.zbw.eu/econis-archiv/bitstream/11159/6190/1/1769382615_0.pdf

- Renault, B., Agumba, J. and Ansary, N., 2018. An exploratory factor analysis of risk management practices: A study among small and medium contractors in Gauteng. Acta Structilia, 25(1), pp.1-39. doi: 10.18820/24150487/as25i1.1

- Rungani, E.C. and Potgieter, M., 2018. The impact of financial support on the success of small, medium and micro enterprises in the Eastern Cape province. Acta Commercii, 18(1), pp.1-12. doi: https://doi.org/10.4102/ac.v18i1.591

- Sanusi, Z.M., Johari, R.J., Said, J. & Iskandar, T., 2015. The Effects of Internal Control System, Financial Management and Accountability of NPOs: The Perspective of Mosques in Malaysia, Procedia Economics and Finance, 28(1), pp.156-162. doi: https://doi.org/10.1016/S2212-5671(15)01095-3

- Savage, A., Norman, C.S. and Lancaster, K.A.S., 2008. Using a movie to study the COSO Internal Control Framework: an instructional case. Journal of Information Systems, 22(1), pp.63-76. doi: https://doi.org/10.2308/jis.2008.22.1.63

- Setshedi, A.B.S., Mkwanazi, M.S. and Mbohwa C., 2021. Small-scale Manufacturing of Aluminium & Steel Products Inclusion in the Mainstream Economy. Proceedings of the International Conference on Industrial Engineering and Operations Management, Monterrey, Mexico, IEOM Society International, pp.2803-2814.

- Singh, S., 2020. Supporting the SMME sector A driver of economic reformation and growth in South Africa following Covid 19 pandemic. Tax Professional, 2020(38), pp.36-38.

- Sitole, V.D., 2021. An assessment of the relationship between entrepreneurial orientation and business performance in SMMEs in KwaZulu-Natal. Master’s degree, North West University.

- Siwangaza, L., 2013. The status of internal controls in fast moving consumer goods SMMEs in the Cape Peninsula. Master’s degree, Cape Peninsula University of Technology.

- Smit, Y., 2012. A structured approach to risk management for South African SMEs. Doctoral degree, Cape Peninsula University of Technology.

- South Africa., 1996, National Small Business Act No. 102 of 1996, Government Printer, Pretoria

- South Africa., 2019. Revised Schedule 1 of the National Definition of Small Enterprise in South Africa. Government Gazette No. 42304, Government Printer, Pretoria

- Spies, J.B., Barbara, M. and Lynne, R., 2020. Ethical considerations when using online research methods to study sensitive topics. Translational Issues in Psychological Science, 6(3), pp.235-239. doi: https://doi.org/10.1037/tps0000266

- Spira, L.F. and Page, M. 2003. Risk management: the reinvention of internal control and the changing role of internal audit Accounting. Auditing & Accountability Journal, 16(4), pp.640-661. doi: https://www.emerald.com/insight/content/doi/10.1108/09513570310492335/full/html

- Thamaha, R., Dickason, Z. and Ferreira-Schenk, S. 2021. Analysing the Risk Management Perception of Small, Micro and Medium Enterprises, Economic Development. Technological Change, and Growth, 17(3), pp.209-228, doi: https://dj.univ-danubius.ro/index.php/AUDOE/article/view/985/1372

- Tran, E.M., Tran, M.M., Clark, M.A., Scott, I.U., Margo, C.E. and Cosenza, C., 2019. Assessing the Quality of Published Surveys in Ophthalmology. Ophthalmic Epidemiology, 27(5), pp.339-343. doi: https://doi.org/10.1080/09286586.2020.1746359

- Tuttle, B. and Vandervelde, S.D. 2007. An empirical examination of COBIT as an internal control framework for information technology. International Journal of Accounting Information Systems, 8(4), pp.240-263. doi: https://doi.org/10.1016/j.accinf.2007.09.001

- Vawda, M., Padia, N. and Maroun, W. 2013. Islamic banking in South Africa: an exploratory study of perceptions and bank selection criteria, Proceedings of the Biennial Southern African Accounting Association Conference, Somerset West, South Africa, Southern African Accounting Association, pp.941-973.

- Yearwood, L.D.A. 2011. A Conceptual Framework for the Prevention and Detection of Occupational Fraud in Small Businesses. Master’s degree, Concordia University College of Alberta.

Article Rights and License

© 2023 The Author. Published by Sprint Investify. ISSN 2359-7712. This article is licensed under a Creative Commons Attribution 4.0 International License.