Keywordsairline development airline sales airport competition airport marketing airport profitability airport route development airport sales network development

JEL Classification M19, M31, N70, O18, R4

Full Article

1. Introduction

The prosperity of every community surrounding an airport depends on the growth of it, either we are talking about creating new jobs, new investments, boosting tourism, stimulating businesses by increasing exports, making it more attractive to all passengers. The airport improves the quality of life by providing people of the communities with opportunities for leisure and cultural experiences, but also a good and fast way to travel for business, improving the living standards by contributing to sustainable development: facilitating tourism, creating new jobs, generating economic growth. According to ACI, for every 100 airline jobs, approximately 350 are supported in the community, namely as indirect jobs related to the airline growth at one particular airport, or the creation of 750 on-site jobs for every 1 million carried passengers per year.

On a worldwide level, the aviation industry is becoming more consolidated, airlines merging with others for better economies of scale or big airline groups buying other struggling carriers in order to gain market share. For this reason, airlines have a different view of airports – commercial partners which can provide not only information about the market (catchment area, type of traffic, traffic flows etc) but also incentives to support growth in a turbulent market with the purpose of sharing the commercial risk any new route involves. From an airport perspective, the airline should be the most important customer and the relationship with it should be of mutual understanding of each one’s needs. The airline companies full rely on data which airports provide, the assessment of market opportunity given that airports understand and evaluate the local market more precisely.

The changing market place due to fierce airport competition, especially in Romania where airports are situated very close to one another has changed the ways airports approach airlines. A successful route development strategy for each airport should be all about the relationship the airports build with the airlines which has to be a long-term relationship, even though the short and medium terms efforts do not pay off. As network strategies may happen to change very frequently, airports need to keep airlines up to date with the latest changes in the GDP of the catchment area, changes in the traffic flows, airport fees or new incentives schemes that might help airlines offset the commercial risk. Of importance is the inclusion of tourism boards and economic development agencies which can support airlines with data regarding the number of tourists, the origin, lodging nights in the catchment area or the number of active companies in the catchment area, number of employees, turnover etc. In regards to Romania, air transport creates multiple economic benefits, the footprint of the aviation industry translated by the contribution to the local and national GDP, number of jobs created and revenues from taxes.

2. Theoretical Framework

2.1.The Conceptualization of Route Development Elements

Generally speaking, an airport provides the necessary infrastructure for airlines to carry passengers from point A to point B or from point A to point C via point B. Given the fierce competition, airports cannot expect an airline to operate from their airport only given that their runway is better than their competitor or their airport terminal or equipment are much better – no longer valid reasons in a non-regulated aviation environment or enough to secure new routes. Airports need to understand that given the rising fuel price, pressure on yield and the dynamic economic conditions of different markets determines airlines to seek larger airports with larger catchment area and a higher buying power. According to RDC Aviation (2014) aviation is deeply shaped by risk evaluation given airlines are at a much bigger risk than airports. Risk in the aviation also according to RDC Aviation (2014) can be seen from a double perspective – financial and reputational. The financial risks such as signing contract with handling agents or employing cabin crew are a matter of planning and can be quantified while the reputational risks such as reviews for delayed or cancelled flights, bad passenger experience are not easy to quantify and may take time to solve and gain consumers trust again. Airports as well are not exempt from reputational risks that come from failed routes which have not been marketed enough or the inability to attract airlines that choose other airports or overambitious plans which may result in a financial damage for the airport in the long term. According to Sabre (2017) risks are highly linked to oil prices, being the industry most affected by a rise in the fuel price. It is estimated that 1 dollar increase per barrel of oil can impact the airline industry additional 1 billion dollars per year. Also the emergence of low-cost carriers can be considered as a disruption of the market, but also an evolution in terms of airline business models and what airports and passengers need.

Bernier (Sabre, 2017) believes airlines around the world are constantly looking for to add new destinations to their network, performing route evaluations to see if a route can be profitable in the long-term. Four major elements need to be considered also by airports in their route development strategy: demand for a certain route which takes into account fares, indirect traffic, airlines flying, number of passengers, willingness to pay etc.; hub connectivity – airlines can predict revenue and profitability on a route depending on a different time of the day by analyzing data received from the airports which know the market better according to their market research.; aircraft availability – airlines need to deploy their limited capacity to route where maximum profitability is guaranteed, airport needing to understand which route is best suited for the airline company they are approaching. The last key element according to Bernier (Sabre, 2017) is matching the competition – a thing airport want in order to stimulate demand on a certain route with potential for two or more companies operating the route.

Fu et al. (2010) have been studying route development by defining marketing stimulation which has been widely accepted and can be driven by numerous factors. The market stimulation derives from air transport liberalisation through additional airline services, increased competition leading to lower air fares. The market stimulation might arise given the fare effects and new air services could lead to additional competition, hence lower prices for airline tickets. Fichert and Klophaus (2011) analyzed the financial incentives airports may give to an airline and can be divided into direct payments, either payment per flight or passenger, marketing budget, discounts on airport charges and risk sharing agreements. According to the authors, the short-term impact of the direct payments as well as discounts on airport charges is negative on the operating results of an airport. The losses of public airport or private airports are covered by taxpayer-funded resources. Papadopoulou (2012) defines airport marketing as a function that in line with the corporate strategy, can interact with target groups such as airlines or other stakeholders, identify and address each group’s needs in order to stimulate and accelerate the growth resulting in more aviation or non-aviation revenues, depending on the case.

2.2.Airport Competition Conceptualization

Authors such as Lian and Ronnevik (2011) have focused on traffic leakage, term used by airport

marketers to describe competition when two or more airports catchment areas overlap, which is the case for many Romanian airports situated at a short distance. Forsyth, Gillen, Muller and Niemeier (2010) believe that airports compete at least in 2 situations: overlapping of the catchment area or when two airports are alternative transfer hubs. Morrel (2010) believes that airport compete in order to attract and retain airlines, providing not only direct aeronautical revenues, but also services to the passenger and cargo business complementing the airport revenues. He also believes that as airlines have different business models, they use different kinds of operations, thus airports need to be prepared and offer the airlines the infrastructure they need: e.g. airport fees, discounts on volume and quick turnaround times are essential for low-cost carriers which full service airline demand special check-in counters, larger spaces and facilities for their business passengers which require lounge, dedicated check-in areas or priority boarding.

Airports that have overlapping catchment areas compete for passengers within their area of attraction

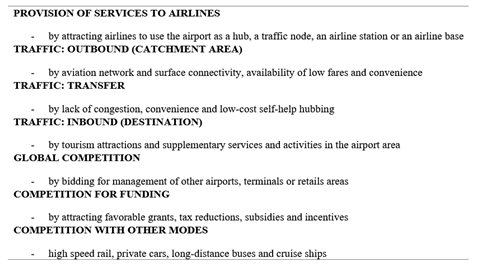

and the ability to compete in such an area can be determined by many factors such as the network of destinations offered at the airport (hub connections or non-stop), the airport connection with surface means of transport, low-cost penetration at an airport and the location of the airport or its size and ease to use. Morrel (2010). Airports need to find their competitive advantage in order to attract both airlines and customers: either located in a highly business environment or touristic location or offer complementary services to increase their non-aeronautical revenues. Moreover, the liberal strategy of air transportation pushed the low-cost carriers to grow faster and the airports to compete even fiercer in order to attract such services. Copenhagen Economics (2012) developed seven areas of competition that the airport industry is facing today given the low-cost competition, the rise of internet which facilitates customers to find the best option for their travel needs.

Figure 1. The areas of competition within the airport industry

Source: Copenhagen Economics, 2012

Nowadays, a vital role is the airport market power which can be limited by the power of airlines, the

final decision making entity, which can switch operations to other airports at much better conditions in terms of passenger experience or airport fees. Thelle et al. (2012) consider that airlines can rapidly, switch operations in case one airport changes the terms and conditions or does not fulfill promises in regards to airport capacity development. In fact, airlines’ buying power which is a consequence of the European single aviation market helps all airlines (but rather LCC) to switch from one airport to another, close bases, relocate airplanes to other bases in Europe, at their earliest convenience or where benefits the airports give are more substantial and helps their long-terms strategy much better. Morell (2010) believes that airports may compete for traffic share, for different traffic types or certain passenger segments. Also, airports with overlapping catchment area compete for origin-destination or P2P traffic and for regional airports, passengers may have the flexibility to choose the best options suited to their needs. Thelle (2012) believes that airports can switch their strategy in attracting certain airlines with particular business models or can dedicated their strategy to attracting different passenger segments as low-yield passengers for LCC (focusing on volume) or high-yield passengers or transfer passenger for airlines with a hub and spoke business model.

3. Romanian Aviation Market – Key Elements for Airport Route Development

3.1. Romanian Airports – Passenger Traffic Evolution, Inbound and Outbound Markets

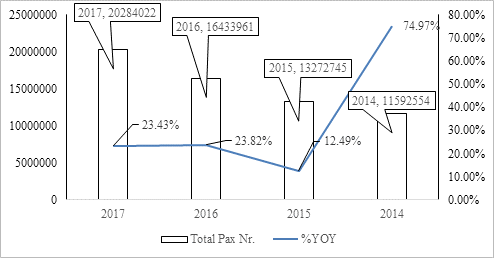

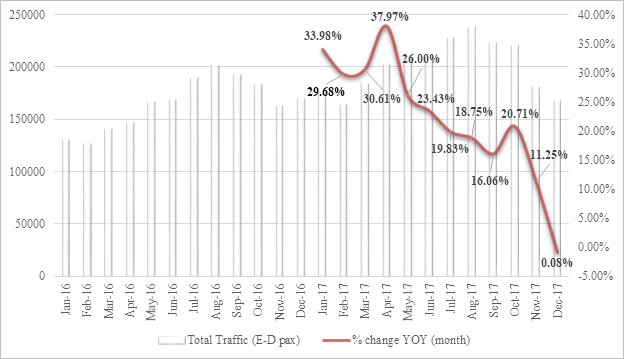

With 16 international airports, all of them with a public owner, Romania has seen a huge expansion in the number of routes airlines operate from all airports. The poor road infrastructure, the political pressure on small regional airports to increase traffic by offering airlines different incentives, the low-cost expansion and the strong VFR (Visiting Family and Friends) traffic, led to an explosion in traffic: +74.97% passenger increase in 2017 to 2014, from almost 12 million pax to 21 million pax in 2017, +12.49% in 2015 to 2014, +23.82% in 2016 to 2015, +23.43% in 2017 to 2016.

Figure 2. Romanian Airports – total traffic evolution per year, 2015-2017

Source: Romanian National Institute of Statistics

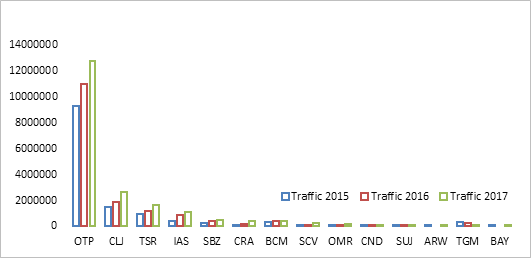

In regards to the airports, Bucharest Otopeni is number 1 in terms of embarked-dismebarked passengers, followed by Cluj, Timisoara, Iasi and Sibiu. For 2017, the top 5 airports in Romania accounted for almost 92% of all traffic.

Figure 3. Romanian Airports – total traffic evolution per airport, 2015-2017

Source: Romanian National Institute of Statistics

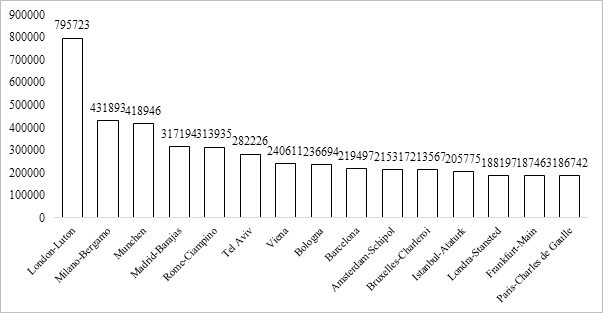

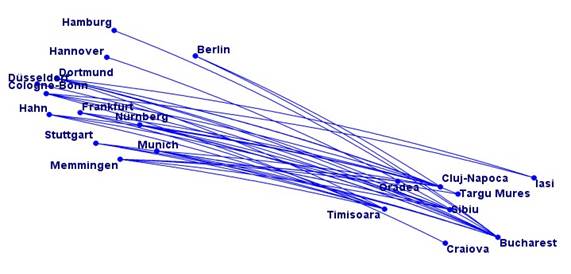

In terms of inbound and outbound traffic for Romania, Romanian National Institute of Statistics provides a complex overview of the flights in 2017, by airports and countries. The inbound traffic by airports classifies London-Luton as first with 800k passengers, followed by Milano Bergamo with 431k passengers and Munich with 418k passengers.

Figure 4. Romanian Airports – inbound traffic by airports in Europe 2017 (top 15 airports)

Source: Romanian National Institute of Statistics

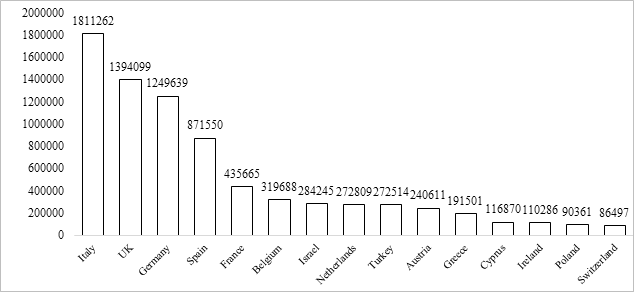

Taking the inbound traffic by countries, Italy is number 1 with a little bit over 1.8M pax, followed by the UK with almost 1.4M pax and Germany with almost 1.3M pax. Compared to the inbound traffic by airports graphic, London Luton (795.723 pax), London Stansted (188.197 pax), London Heathrow (125.824 pax) and London Gatwick (59.407 pax) generate 88.86% out of the total pax traffic UK>RO, while Romanian inbound traffic from Italy is more scattered, more Italian airports having direct connections with Romania.

Figure 5. Romanian Airports – inbound traffic by countries 2017 (top 15 countries)

Source: Romanian National Institute of Statistics

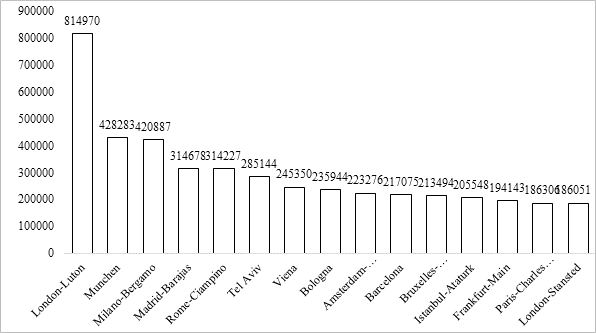

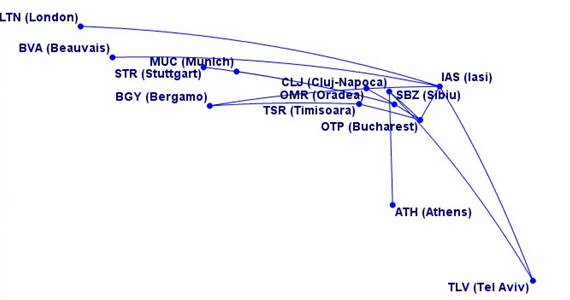

The outbound traffic by airports shows a switch between Munich and Milano Bergamo, while London Luton remains number 1 with a slight decrease to inbound trafic. Other airports are Madrid Barajas and Rome-Ciampino where many Romanian expats live, followed by Tel-Aviv and Vienna.

Figure 6. Romanian Airports – outbound traffic by airports in Europe 2017 (top 15 airports)

Source: Romanian National Institute of Statistics

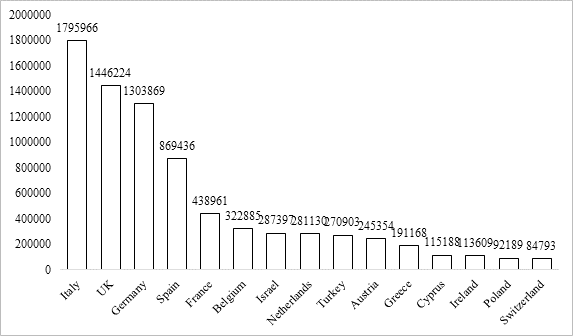

By ranking, the outbound traffic by countries is no different than inbound traffic by airports. On a different note, Romanian National Institute of Statistics show increasing traffic from Middle East countries with 107.595 embarked-disembarked passengers in 2017 for Dubai and Doha with 88.213 embarked-disembarked passengers, both with direct connections to Romania.

Figure 7. Romanian Airports – outbound traffic by countries 2017 (top 15 countries)

Source: Romanian National Institute of Statistics

3.2.Romanian Airports – An Overview of Airport Charges

With one of the highest low-cost penetration rate in Europe and the growing pressure of competition,

Romanian Airports have drastically decreased their airports fees in the attempt to focus on volume and become more profitable in the long-term or find new incentive schemes to motivate airlines. Wizz Air, the biggest low-cost player in the Romanian market had in 2017 (according to capital.ro) a market share of 31% (with operations on 10 Romanian airports), Blue Air a market share of 21% (with operations on 8 Romanian airports), Tarom with a market share of 17% and Ryanair with just over 10% - a small player in the Romanian market. Overall, according to RDC Aviation, the market share of the LCC in Romania was in 2016 at around 57% (should be over 60% due to the major Wizz Air expansion in the Summer 2017) and 43% for legacy carriers. More, according to OAG (2017), Romania was the fastest growing market in Central and Eastern Europe after Bulgaria in terms of departing seat capacity in 2016, 21.6% higher than in 2015.

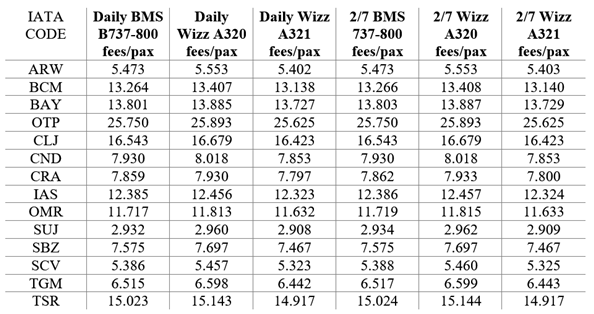

In order to get a better view of the airport charges and how much would an airline like Wizz Air or

Blue Air pay for a 2 weekly frequency versus a daily flight using one of their A320, A321 or 737-800 for all Romanian Airports, it is essential to analyze the landing charges (euros/ ton), lightning charge (euros/ton), parking charges (euro/ton/hour), passenger charge (euro/pax), security charge and transit charge (euro/pax), Passenger Reduced Mobility Charge (euro/pax), and development charge (euro/pax) and landing % or incentives.

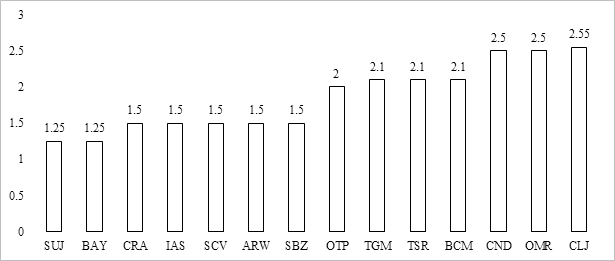

Figure 8. Romanian Airports – landing charge (euro/ton)

Source: Romanian Aeronautical Information Publication

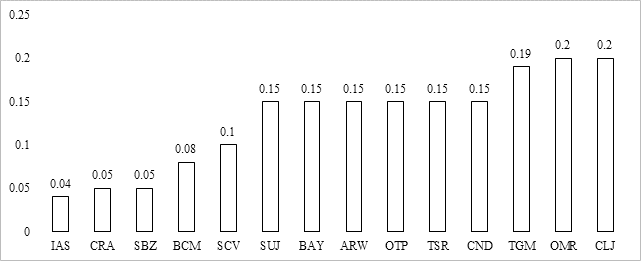

Figure 9. Romanian Airports – lightning charge (euro/ton)

Source: Romanian Aeronautical Information Publication

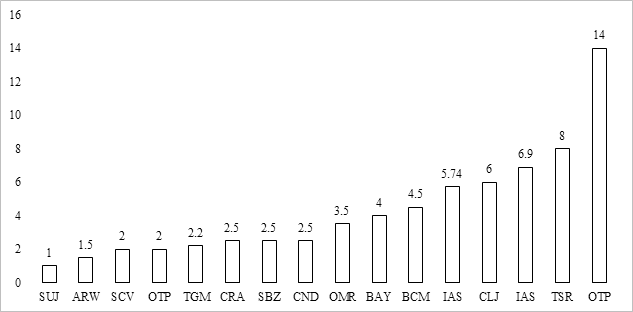

Figure 10. Romanian Airports – parking charges (euro/ton/hour)

Source: Romanian Aeronautical Information Publication

Figure 11. Romanian Airports – passenger charges (euro/pax)

Source: Romanian Aeronautical Information Publication

A strategy to attract low-cost carriers but with very little impact on airport charges is what Suceava, Sibiu and Craiova have been doing – no parking charges for the first 3 hours. Also, in regards to the passenger charges, Iasi and Bucharest airports charge differently for international and domestic flights: 5.74 domestic flights for Iasi and 2 euros for domestic flights from Bucharest Otopeni. Other airport charges include:

- Security charge compulsory for all airports that ranges from 7 euros per passenger for Bucharest and Baia Mare to 1 euro for Sibiu, Suceava and Satu Mare.

- Transit or Transfer charges that apply only to certain airports: 4 euros/pax for Baia Mare, 3 euros/pax for Cluj, 2 euros per pax for Oradea and Suceava, 1.5 for Timisoara, 1 for Arad and Sibiu.

- Bucharest, Baia Mare, Cluj, Bacau and Timisoara charge airlines for PRM while Baia Mare, Cluj and Iasi charge airlines a development fee – 3, 5 and 4 euro.

- All Romanian Airports have an incentive scheme given a certain frequency, the landing charge can be discounted. This is different for all airports, other offering a 5% discount for airlines that operate between 5 and 10 landing per month, others given a certain amount of movement per year will grant a certain amount of discount or a certain number of passengers per year, other airports like Timisoara will grant a 75% for development charge in case of new destinations. Other incentives may include schemes approved by the European Union such as state-aid, ex-ante schemes that may grant financial aid that will reduce airport charges (landing, lighting, parking, passenger service, development fee, airport security charge, transit and transfer tariff) by 50% and will be granted for a maximum period of 3 years.

In order to calculate the airport charges, we will take Blue Air And Wizz Air as an example, both strong players in the Romanian market, Boeing 737-800 (189 maximum seats) for Blue Air and A320 (180 maximum seats)/A321 (230 maximum seats) for Wizz Air, a new international destination for each Romanian airport, a 2/7 destination and a destination operated daily as well as 80% load-factor for each airline. For landing, parking and lightning we are going to apply the MTOW and for passenger charge, security and development the load-factor will be applied.

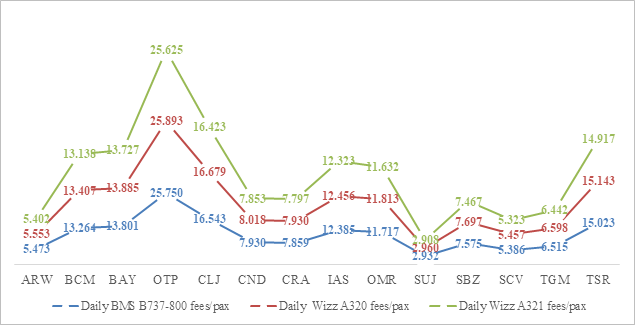

Figure 12. Romanian Airports – fees/departing passenger (euro – 3 decimals)

Source: Romanian Aeronautical Information Publication, Author’s calculations

The airport fees are calculated in euros and an MTOW (Maximum Take-Off Weight) of 78.5 has been applied for 737-800, 77 to A320 and 93 to A321 as well as a load factor of 151.2 for B737-800, 144 passengers for A320 and 184 passengers for A321.

Landing % has not been applied for Satu Mare, Cluj and Bucharest Otopeni as the number of movements or passengers per year do no meet the requirements the airport set to be reached. The fees/pax are a roughly estimate as many airports tend to add new contractual terms that may bring the fees even to a lower level.

The results above start from the hypothesis that neither Blue Air nor Wizz Air operate from any given airport, but plan to start a new route operated with a daily or a 2 weekly frequency, using different aircrafts. Important to be mentioned is that the results above do not include handling fees that the airlines pay to different handling providers and vary from airport to airport.

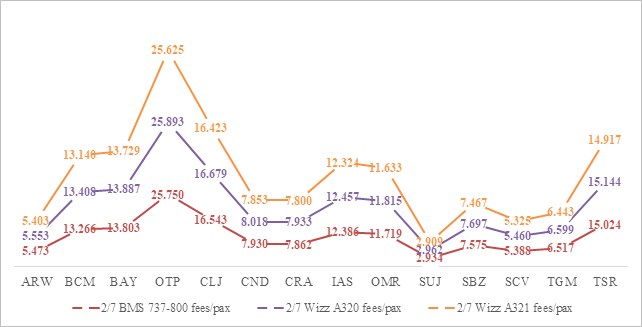

Further, graphics 13 and14, presented below, show and proved what is already known to the aviation industry. Regardless of the airport or the frequency with which a route is operated, the A321 wins in every situation. Romanian Airports should focus their effort while coordinating with airlines to increase volumes while lowering airport fees, all in the benefit of both parties.

The most notable differences are for Timisoara in case of a daily operation: 15.023 euros for departing passenger for a Boeing 737-800, 14.917 euros for an Airbus A321, 15.043 euros for an Airbus A320. Focusing on volume is a key strategy for further development.

Figure 13. Romanian Airports – airport charges/departing passenger (euro, 3 decimals)- daily operation

Source: Romanian Aeronautical Information Publication, Author’s calculations

Figure 14. Romanian Airports – airport charges/departing passenger (euro, 3 decimals)- 2 weekly operation

Source: Romanian Aeronautical Information Publication, Author’s calculations

4. Developing a Route Development Strategy: Market, Competition and Customers

From an airport perspective, a good route development strategy should start from a deep understanding

of the aviation environment, understanding the airline business model and its network while from an airline perspective, elements like the catchment area, demand, traffic flows, demographics should be defined from the very beginning. A route development strategy should be a triangle relationship between the airport, the airline and the tourism authorities or the local business chambers, working together, defining the goals, establishing a fruitful long-term relationship. For an airport, it is crucial to know the business model of the airline and the requirements for the operations. Some airlines demand high-yield premium customers in order to operate a route at a higher frequency, either to transfer passengers via a hub or P2P traffic, some airlines target lower yield markets (VFR – Visiting Family and Friends), airports would they would have monopoly on routes or reach to be in the top 3 in terms of market share etc.

The B2B market approach of the route development activities involves airports to better understand the airline requirements in what infrastructure and operations are concerned. Airports need to facilitate the interaction between the airlines and third parties such as handling companies, non-aviation parties or aeronautical units. The easy facilitation is crucial given that these businesses provide services to the airlines and also to the airport, essential for the activities related to aviation – fuel suppliers, air traffic control, passenger handling, aircraft handling, baggage handling, aircraft cleaning, inflight catering, the airport security etc. The aeronautical third parties ensure that airlines can benefit from quality and competitive services, comply to the rules for smooth operations. The non-aeronautical businesses are essential to complete the airport product with different non-aeronautical services for the passengers such as car rental providers, parking providers, shopping units, cleaning services etc.

4.1.Understanding the Market – Key Elements of the Catchment Area

We can define an airport catchment area as the geographic area from within an airport can expect to

attract passengers or likely to draw passengers who will use the air services from an airport. Understanding the market for each airport is complicated given the multiple elements of the catchment area which need to be considered: airport competition, destinations, fares, market share, airline capacity, flight frequencies, low and high yield traffic potential, traffic flows, seasonality, catchment area overlapping with other airports.

Airports from Romania are very different in terms of routes, some catchment areas being high-yield markets while other focus strict on VFR traffic. Understanding a market also means the airport needs to quantify it in terms of: direct and indirect passengers traveling from a hub from the airport or from a competing airport (surface leakage), the corporate travel potential (the number of weekly seats, how often and how many companies), the employment sector which can vary from IT, finance, tourism, automotive, GDP rates, main trade partners etc. Romania is also known as a tourist attraction, therefore Romanian Airports need tourism indicators such as origin/nationality of visitors, number of lodging nights, events or places of interest in the catchment area, willingness or willingness to pay.

According to the National Institute of Statistics (2018), the number of lodging nights has increased by 6.5% in 2017 to 2016 and the lodging nights for foreign tourists in Romania represents 19.6% out of the total lodging nights. According to the same source, 84.8% of the total foreign tourists came from an European Union country while the average stay was only 1.9 days. Zooming in even further, the majority of the foreign tourists came from Germany (324.371) followed by Israel (292.752), Italy (241.398), France (167.1630) and United States of America (157.179). Other data that must be used in the route development strategy is related to demographics, VFR traffic or ethnic ties or yields, traffic seasonality, traffic forecast. Understanding the competition is another key element that needs to be taken into consideration. Airports need to contrast their passenger yield to other airports (revenue/pax/km), average paid fare or seasonal variation in demand.

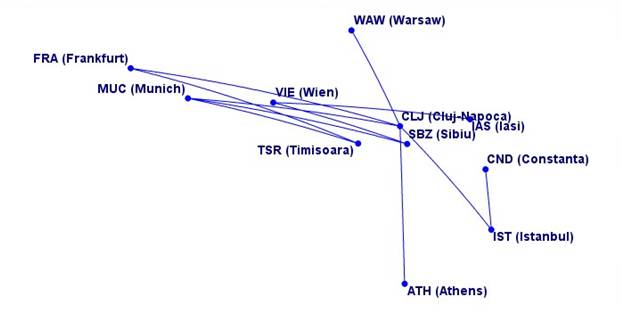

In order to better understand parts of the Romanian market, some examples such hub connectivity, overlapping routes, V route competition, number of connections to Germany or United Kingdom need to be taken into account. Taking the regional hub connectivity in Summer 2018 (let alone Bucharest which has multiple hub connections) Romanian regional airports have been increasing their hub connectivity either via new hub destinations or increasing frequencies on already served destinations. Lufthansa Group is the biggest "player" in the Romanian regional market with 7 routes from their MUC, FRA or VIE hubs, serving Timisoara, Cluj, Iasi and Sibiu (frequencies vary from 6 weekly up to 21 weekly). Turkish Airlines serves 2 regional Romanian Airports with 4 weekly flights to both Cluj (going daily in S19) and Constanta. Also, LOT Polish Airlines connects Cluj and Warsaw with 6 weekly flights served by DH4. On a summer seasonal basis, Aegean Airlines serves Cluj 2/7 with DH4/A320. In terms of alliances, Star Alliance dominates the regional RO market, with oneworld or Skyteam having no presence. This might change in the near future as TAROM will connect Cluj and Timisoara with Paris CDG, 2-3 weekly operation in the beginning. Exceptionally, we might consider Blue Air a part of this analysis as they connect Iasi and Bacau to their Turin "hub" - although they target the large Romanian diaspora living in Northern Italy.

Figure 15. Romanian Airports – Regional Hub connectivity in Summer 2018

Source: Author’s own research.

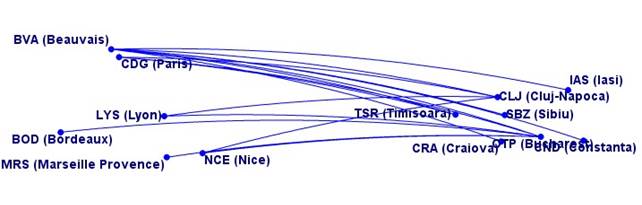

With a large diaspora in countries like Spain, Germany, or France, Romanian airports have been

struggling to find new low-cost connections to these countries. In France, for example, even though almost 230.000 Romanians live and work in France (according to a study of Romanian Minister of Labour, 2016), France has been poorly served from all Romanian Airports in the past few years. However, 2018 seems to bring multiple new frequencies or new connections from all Romanian Airports to/from France. Wizz Air has already increased frequencies from OTP (Bucharest Otopeni) to BVA (Paris Beauvais) to 1 daily, started a 3 weekly route from Sibiu to BVA (Paris Beauvais) and will start a new route in July from Iasi to BVA, complementing Blue Air services on the same route. Other developments include a new route from Nice to Bucharest and increased frequencies from Cluj to BVA. Further expansion of TAROM network will bring Cluj and Timisoara closer to CDG (Paris Charlles de Gaulle), meaning an increased Skyteam presence in the regional market, dominated by Star Alliance.

Figure 16. Romanian Airports – Direct Connectivity with French Airports in Summer 2018

Source: Author’s own research.

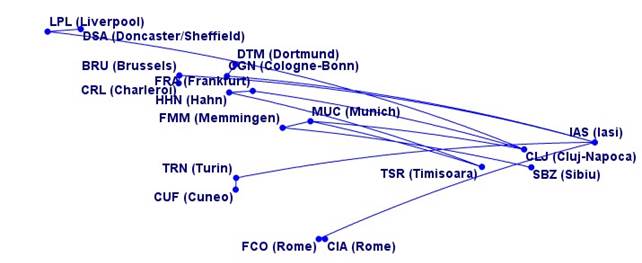

In regards to the German direct connectivity, Transylvania region is the best connected region given

the multiple business relations and very strong ethnic traffic. Airlines flying from Romania to Germany are Wizz Air with 20 routes, Lufthansa with 7 routes, Tarom with 6 routes, Blue Air with 5 routes, Ryanair with 2 routes, Eurowings with 1 route. Bucharest is the best connected city with 10 direct flights, followed by Cluj-Napoca with 8 direct connections, Sibiu and Timi?oara are both connected to 6 German airports while Târgu-Mure? and Ia?i are both connected to 2 German airports. Other cities directly connected to Germany are Oradea with one connection to Memmingen (ends in November 2018) and Craiova to Cologne.

Figure 17. Romanian Airports – Direct Connectivity with German Airports in Summer 2018

Source: Author’s own research.

Not to be ignored is the United Kingdom market from/to Romania. Zooming into London Airports, in

2017, the number of pax traveling from/to London Airports to/from Romanian Airports increased by +21.47%, reaching almost 2.4M pax from almost 2M pax in 2016. In 2017, Wizz had the biggest seat capacity from/to Romania to/from London Airports, while 5 airlines fly from/to 11 Romanian Airports to/from London Airports – Wizz Air, Ryanair, Blue Air, Tarom and British Airways.

Figure 18. Romanian Airports – Number of passengers (Romania-London Airports, 2016-2017)

Source: caa.uk.co

As Fig.18 shows, the traffic to/from London Airport is highly seasonal, with the highest peaks July,

August and September for 2016 and also for 2017. The months with the lowest traffic are January and February for both years while the month of June has seem a slight decrease in traffic compared to May for both years, probably to a cut in capacity.

Finally, airports need to assess their current route network in terms of both direct competition and V-

type competition. As Fig.18 shows, direct overlapping happens on more mature routes, high-frequency potential or high-yield routes with business traffic potential.

Figure 19. Romanian Airports – Overlapping routes in Summer 2018

Source: Author’s own research.

The V-type route competition happens on more VFR routes where 2 airline companies have a base at

an airport. For example, Wizz Air and Blue Air have both bases in Iasi and Cluj, Wizz offering Brussels Charleroi and Blue Air Zavantem from Iasi, Fiumicino and Ciampino from Iasi or Cuneo and Turin (Ernest versus Blue Air), while in Cluj, Blue Air offers Liverpool and Wizz Air offer Doncaster.

Figure 20. Romanian Airports – V-type route competition in Summer 2018

Source: Author’s own research.

4.2.Building a Stronger Relationship between Airports and Airlines: Increasing Revenues and Creating Loyalty Programs

Both airlines and airports can work together in a stimulating way for both parties. The competitive

pressure from the market and given the airport competition in Romania, airlines and airports need to take a further step and develop synergies in all fields. We can name 4 key areas where airports and airlines can work together, enhancing the relationship: sales, loyalty programs, digital programs and real estate or hub operations where necessary. The customer experience can be improved by using and developing the first 3 but also boosting and stimulating the commercial side for both airlines and airports – innovate online sales for example.

Selling can becoming a great way to satisfy passengers’ needs who are always in a hurry, airport and airlines having the ability to integrate sales channels for all retails goods. An airplane to gate strategy means passengers can order something online and airport staff could deliver the products at the gate. Airlines could also promote the channel and advertise the website into their in-flight entertainment system. A home to gate strategy cam allow passengers to browse and buy a full selection of airport’s product when at home and pick them up at the gate.

Moreover, all the airlines offer loyalty programs and work with different partners, but airports rarely have a loyalty program that can attract and make passengers loyal. Airports with loyalty programs can work with airlines to offer passengers discounts, vouchers or gift card for can work with other partners such as car rental, non-aviation businesses within the airport etc. Airports and airlines can join forces and expand the reward program by offering access to airport lounges, free parking, fast-lane where possible and can cumulate points for frequent flyer status. With a joint sales channel, a joint reward program, airlines and airports can see an increase in revenues at a relative low cost for both parties.

Looking from the airline perspective and the evolution of rewarding programs, the more a passenger pays for travel, the more benefits he enjoys. Translated from the airport perspective we may rephrase this to “the more a passengers flies from an airport, the more benefits he enjoys”. So, should an airport loyalty program help the airports convince the airlines of their potential and also help them in their development activities? Also, how should Romanian airports engage with retaining passengers and offer them the best loyalty conditions? Or how should airports convince foreign tourists to start visiting the region from their airport and not from a not-far distance airport with the same service? According to a study provided by Marketer (2017) the best ways companies can build loyalty are customer service 24/7, rewards for feedback, purchases (or travel applied to the aviation industry), exclusive offers, personalize services and products and familiarity to the products or services.

As good as it may sound, it is questionable whether an airport loyalty program should be beneficial for Romanian airports. For Romanian airports, it is important to follow the next goals of an airport loyalty program:

- Bringing the airport brand to a new level

Many airports in Romania struggle to get known by the name of the region they activate in (Transylvania, Moldavia, Bucovina etc). Obviously, every airport wants the travelers to fly from their airport over other airports in region, given the short distance between some of them. Creating an airport loyal program can increase the brand awareness of the airport and stimulate a positive experience that travelers will associate positively with the airport brand.

- Improve the traveler experience in the airport and in the region

Except Bucharest, the other terminals of all regional airports tend to be quite small, thus narrowing the chances of a great traveling experience. Improving the traveler experience means encouraging the members of the program to spend and engage with the program. Also, a great loyal program means using marketing as a great way to closely work with all stakeholders for a more personalized experience, or even offer exclusive deals. For the Romanian airports which tend to have a minimal passenger services (a café-bar, restaurant or a duty-free shop) it is hard to conceive a great traveler experience. But given the characteristics of the market and the low-cost domination, airports have to adapt and create a more tailored experience according to the low-cost passenger profile. But even with this profile, airports need to be careful to the business passengers which tend to aim higher in terms of services.

- Easy to use for members and offer real time feedback

Each loyalty program has to be easy to use and offer real time feedback for the airport. Users should be allowed to offer their opinion on the airport product and also feel engaged in the airport activites. This last often applies to community members who want to take part in the airport development.

Given the current conditions, it is hard to imagine a great customer experience for passengers, but airports need to closely work with all stakeholders to retain travelers. So, in order to attract more tourists as well to keep passengers from flying to nearby airports which may have the same services, it is important to keep in mind that passengers may need that extra something that others airports won’t be offering. This may include, discounts for museums in the region, important events, access to the airport lounge (which in many cases is missing), discounted fees for car-rental or even parking facilities in the airports, discounted fees for local public transport. Also, airports should partner with important hotels in the region or even restaurants given the large number of tourists that may visit the region. Always keeping in mind the brand of the airport and the region, airports may tailor the passenger experience and the airport loyalty program to the local customs.

5. Conclusions and Recommendations

A market whose evolution has been extraordinary in the last years, Romanian Aviation is an unique

market with a full tourism potential for the many years to come. Airports need to focus on attracting volume as the analysis proved the A321 is the cheapest to operate from any given airport but also as new investors decide to open new office branches and employ local people, airports need to focus on creating a route development strategy which targets on attracting full-legacy companies that can open the world of possibilities in terms of connections via their hubs. Airports also need to invest in creating a more pleasant customer experience for all passengers as well as working closely with airlines to develop non-aeronautical revenues, a benefit for both parties. Innovation is part of the future and given the extreme airport competition, airports need to focus their efforts and offer airlines creative incentives scheme which will increase traffic and finally boost confidence in the market for other airlines exploring the Romanian opportunities. As each airport is different, the route development teams need to be aware of the catchment area’s necessities and attract exactly what is needed.

References

- Aviation Economics, 2014. What does a good route development look like? [online] Available at: https://www.sabre.com/insights/4-considerations-airlines-must-make-when-planning-new-routes/ [Accessed 12 July 2018].

- Bush, H., 2010. The development of competition in the UK airport market. Journal of Airport Management, 4(2), pp.114–124.

- Capital Newsroom, 2017. What market shares do Blue Air, Wizz Air or Tarom have in Romania? [online] Available at: http://www.capital.ro/ce-cote-de-piata-au-wizz-air-blue-air-sau-tarom-si-care-sunt-noi.html [Accessed 10 July 2018].

- Copenhagen Economics, 2012. Airport competition in Europe. ACI Europe. [online] Available at: https://www.copenhageneconomics.com/dyn/resources/Publication/publicationPDF/5/195/0/Copenhagen%20Economics%20Study%20-%20Airport%20Competition%20in%20Europe.pdf [Accessed 16 July 2018].

- De Neufville, R., 2008. Low-Cost Airports for Low-Cost Airlines: Flexible Design to Manage the Risks. Transportation Planning and Technology, 31(1), pp.35-61.

- Eurostat, 2016. Statistics regarding migration and migrating population [online] Available at: http://ec.europa.eu/eurostat/statisticsexplained/index.php?title=Migration_and_migrant_population_statistics [Accessed 16 July 2018].

- Forsyth, P., Gillen, D., Müller, J. and Niemeier, H.-M. (Eds.), 2010. Airport Competition: The European Experience. Farnham, UK: Ashgate Publishing, Ltd.

- Franke, M., 2004. Competition between network carriers and low-cost carriers—retreat battle or breakthrough to a new level of efficiency?. Journal of Air Transport Management, 10(1), pp.15–21.

- Fu, X. and Zhang, A., 2010. Effects of airport concession revenue sharing on airline competition and social welfare. Journal of Transport Economics and Policy, 44(2), 119-38.

- Halpern, N. and Graham, A., 2015. Airport route development: A survey of current practice. Tourism Management, 46, pp.213–221. doi:10.1016/j.tourman.2014.06.011.

- Jimenez, E., Pinho de Sousa, J. and Claro, J., 2011. Airport competition and aviation network evolution: An exploratory study on continental Portugal. [online] Available at: https://repositorio.inesctec.pt/handle/123456789/2402 [Accessed 16 July 2018].

- Lian, J.I. and Rønnevik, J., 2011. Airport competition – Regional airports losing ground to main airports. Journal of Transport Geography, 19(1), pp.85–92.

- Malighetti, P., Paleari, S. and Redondi, R., 2008. Connectivity of the European airport network: ‘Self-help hubbing’ and business implications. Journal of Air Transport Management, 14(2), pp.53–65.

- Malighetti, P., Paleari, S. and Redondi, R., 2009. Pricing strategies of low-cost airlines: The Ryanair case study. Journal of Air Transport Management, 15(4), pp.195–203.

- Morrel, P., 2010. Airport competition and network access: A European perspective. Airport Competition: The European Experience. Farnham, UK: Ashgate Publishing, Ltd.

- OAG, 2017. Eastern Europe – low cost and loving it. [online] Available at: http://www.tourism-generis.com/_res/file/4933/52/0/2016-OAG-Eastern-Europe-Report.pdf [Accessed 13 July 2018].

- OAG, 2018. IATA Economics Chart of the Week [online] Available at: https://www.iata.org/publications/economics/Reports/chart-of-the-week/chart-of-the-week-13-jul-2018.pdf [Accessed 16 July 2018].

- Papadopoulou, 2012. Airport Marketing within a highly critical envioronment. [online] Available at: http://web.tecnico.ulisboa.pt/~vascoreis/projects/airdev/Presentation_I_PAPADOPOULOU.pdf [Accessed 9 July 2018].

- Pricewaterhouse Coopers, 2017. Natural partners: How airports and airlines can jointly boost revenues, lower costs and improve customer experience [online] Available at: https://www.strategyand.pwc.com/media/file/Natural-partners.pdf [Accessed 10 July 2018].

- RDC Aviation, 2016. Low cost airline penetration [online] Available at: https://www.rdcaviation.com/News/Low-Cost-Airline-Penetration [Accessed 10 July 2018].

- Romanian National Institute of Statistics, 2018. Number of passengers and cargo – Romanian Airports in 2017 [online] Available in Romanian only at: http://www.insse.ro/cms/ro/content/transportul-aeroportuar-de-pasageri-%C5%9Fi-m%C4%83rfuri-%C3%AEn-anul-2017 [Accessed 9 July 2018].

- Romanian Aeronautical Information Publication, 2018. Overview of airport charges. [online] Available at: https://www.aisro.ro/ [Accessed 8 July 2018].

- Sabre, 2017. 4 considerations airline must make when planning new routes. [online] Available at: https://www.sabre.com/insights/4-considerations-airlines-must-make-when-planning-new-routes/ [Accessed 15 July 2018].

- SeeNews – Business Intelligence for Southeast Europe, 2017. Budget Airlines in Southeast Europe 2017 [online] Available at: http://investsofia.com/wp-content/uploads/2017/06/BUDGET-AIRLINES-IN-SOUTHEAST-EUROPE-2017_lO5NsOe.pdf [Accessed 12 July 2018].

- Thelle, M.H., Pederson, T.T. and Harhoff, F., 2012 Airport Competition in Europe, Copenhagen Economics, Copenhagen.

- Tretheway, M. and Kincaid, I., 2010. Competition between airports: Ocurrence and strategy. Airport Competition: The European Experience. Farnham, UK: Ashgate Publishing, Ltd.

Article Rights and License

© 2018 The Author. Published by Sprint Investify. ISSN 2359-7712. This article is licensed under a Creative Commons Attribution 4.0 International License.