Keywordsinternal control South African SMMEs sustainability Sustenance framework

JEL Classification G32

Full Article

1. Introduction

Before the formal recognition of South African SMMEs by the National Government in 1996, many small businesses operated in the national economy (Rogerson, 2008; Bruwer and Van Den Berg, 2017). The decision to recognise these business entities stemmed from historic evidence provided of the socio-economic value added by SMMEs in an international dispensation.

In 1947 the theory of Creative Response was developed to address the increasing global unemployment rates and extreme poverty conditions instigated by World War II (Kai-Sun, 1997; Romer, 1999; Jones and Wadhwani, 2006; Lima and Berryman, 2011; Panfilov, 2012). In particular, Creative Response relates to identifying possible opportunities in times of uncertainty, responding to applicable needs over an extended period and increasing supplies to serve such needs as required (Schumpeter, 1947). As time elapsed, during the 1950s, this theory evolved into the science of Entrepreneurship and during this timeframe, it was first adopted by the United States of America (USA) through the formal recognition of SMMEs (Park, 2001; Wren and Storey, 2002). Though the USA saw SMMEs as a type of solution to combat national unemployment and to eradicate national poverty, most other countries around the globe did not see the need for SMMEs as the global economy flourished during this timeframe (King and Levine, 1993; Chang, 2011).

Only during the late-1970s, amidst volatile global market conditions due to the realisation of unmanaged financial risks, other countries started to see the importance of SMMEs. Particularly during the 1980s governments around the world started to embrace SMMEs as ‘solutions’ to achieve relevant socio-economic objectives; mainly to decrease national unemployment and to alleviate national poverty (Eatwell and Taylor, 2000; Hill, 2001; Karmakar, 2006; Staikouras, 2006; Stokes and Wilson, 2010).

Reverting to South Africa, the formal recognition of SMMEs in 1996 allowed the National Government to brand these business entities as ‘solutions’ to achieve three key socio-economic objectives, namely the reduction of unemployment, the mitigation of poverty and the equal distribution of wealth (Republic of South Africa, 1996; Bruwer, 2016). This was done through the publication of the National Small Business Act No. 102 of 1996 which also led to the establishment of relevant Government Support structures, primarily through the Department of Trade and Industry (Molapo et al. 2008; Timm, 2011). These Government support structures include the Small Enterprise Development Agency (assisting with financing, training, franchising), the National Empowerment Fund (assisting black-owned SMMEs with funding), Khula Finance Limited (assisting with funding) and the Industrial Development Corporation (assisting with funding) (DTI, 2015).

Since the passing of the foregoing Act, three amendments have been made to it, more specifically The National Small Business Amendment Act No. 26 of 2003, the National Small Business Amendment Act No. 29 of 2004 and the legislation with the 2019 revised Schedule 1 of the National Definition of Small Businesses in South Africa (Republic of South Africa, 2003; Republic of South Africa, 2004; Republic of South Africa, 2019). None of these amendments altered the definition of SMMEs which is: “separate and distinct business entities that are managed by one owner or more, which predominantly conduct their business in any sector or subsector of the South African economy” (Republic of South Africa, 1996).

According to the third and most recent amendment to the original Act, the 2019 revised Schedule 1 of the National Definition of Small Businesses in South Africa, these business entities can be categorised in terms of size as “micro enterprises”, “small enterprises” and “medium enterprises” (Safii, 2018; Republic of South Africa, 2019) based on 1) the number of full-time employees they employed and 2) the total annual turnover generated.

Research shows that South African SMMEs are important to the country’s economy as they make a substantial contribution towards the three highlighted key socio-economic objectives. Since 90 per cent of all South African business entities are regarded as SMMEs, it becomes apparent as to why these business entities, combined, significantly contribute to the national Gross Domestic Product (GDP) (Mouloungui, 2012; Smit and Watkins, 2012; Ayandibu and Houghton, 2017; Cant, 2017). The monetary value which South African SMMEs add to the national GDP is estimated to be in the region of R1.83 trillion (Statistics South Africa, 2017a). Also, SMMEs holistically provide employment opportunities to a large proportion of the national workforce (Kongolo, 2010; Mukata and Swanepoel, 2017). The number of people which South African SMMEs are reported to employ, range between 12.84 million and 17.11 million (Statistics South Africa, 2017b).

Although the socio-economic contribution of South African SMMEs is substantial, these business entities’ failure rate compares unfavourably with those operating in an international dispensation. This view is supported by the recent statistic that 75% of South African SMMEs fail after being in existence for 36 months (Cant and Wiid, 2013; Moloi, 2013; Bruwer and Van Den Berg, 2017). Prior research (Vawda et al., 2013; Bruwer, 2016; Masama, 2017; Renault et al., 2018; Petersen, 2018; Masama and Bruwer, 2018) suggests that the high South African SMME failure rate has to do with the non-management of economic factors and associated risks. One manner in which the foregoing can be dealt with is through the implementation of a sound system of internal control.

A system of internal control is regarded as a comprehensive system comprising an array of elements, as established by management, to provide reasonable assurance regarding the achievement of a business’ operational objectives, reporting objectives and compliance objectives (Spira and Page, 2003; Adeniyi and Aramide, 2014). Such a system is best implemented through the use of an internal control framework as a foundation (Tarantino and Cernauskas, 2011; Buhr and Gray, 2012; Caratas and Spatariu, 2014).

Notwithstanding the foregoing, previous studies (Bruwer et al., 2013; Masama, 2017) found that South African SMMEs do not widely make use of existing internal control frameworks despite attempts made by researchers and policymakers to guide smaller businesses on how to use these frameworks (COSO, 2005; Brustbauer, 2016). Unsurprisingly, local studies (Siwangaza, 2013; Siwangaza and Dubihlela, 2016) found that the internal control evident in South African SMMEs is inadequate and/or ineffective. This view is further supported by other local studies where it was found that South African SMMEs have poor control environments (Bruwer and Van Den Berg, 2015), make use of questionable risk assessment practices (Masama, 2017), and make use of internal control activities that are not adequate or effective (Petersen, 2018). Thus, with the above in mind and, to this end, the primary objective of this research study read as follows: “To propose an internal control framework that can assist South African SMMEs to implement adequate and effective internal control systems to, in turn, fortify their sustainability”.

For the remainder of this paper, discussions take place under the following headings: 1) research design, methodology and methods, 2) conceptual framework, 3) the Sustenance framework and 4) conclusion.

2. Research Design, Methodology and Methods

For this research study, non-empirical research was performed which also took on the form of exploratory research. According to Reiter (2017), exploratory research pertains to a learning process of reformulating and adapting explanations, theories and initial hypotheses in an inductive manner. To properly execute this learning process, a literature review was conducted – a systematic, explicit and reproducible method for identifying, evaluating and synthesising existing bodies of knowledge as compiled by researchers, scholars and practitioners (Fink, 2013).

Taking into account the research design above, qualitative research was decided on as an appropriate research methodology. Boote and Beile (2005) explain that a thorough literature review can serve as the basis for substantial and useful research. The literature review conducted involved the scrutinising of non-numeric, secondary data from sources which include journal articles, books and research reports. Furthermore, as an untested framework was developed, in the form of an artefact hypothesis, this study also incorporated inductive reasoning.

A total of 150 secondary sources were both scouted and scrutinised by the researcher. Only 103 secondary sources were found to assist in the achievement of the study’s research objective; resulting in the citation of these secondary sources. A summary of the types of sources cited is shown in Table 1.

Table 1. Sources cited in the paper

| Source type | Quantity cited |

| Journal article | 62 (sixty two) |

| Conference paper | 5 (five) |

| Research report | 1 (one) |

| Working paper | 1 (one) |

| Book | 8 (eight) |

| Website | 5 (five) |

| Policy document / Legislation | 9 (nine) |

| Thesis / dissertation | 12 (twelve) |

| TOTAL | 103 (one hundred and three) |

Source: Author

3. Conceptual Framework

This section provides context to the research study at hand while also conceptualising key aspects that are referred to in the developed artefact hypothesis. Below, discussion takes place under the following two sub-headings: 1) South African SMME sustainability and 2) internal control and internal control systems.

a. South African SMME Sustainability

Recent academic literature states that up to 75 per cent of South African SMMEs fail after being in operation for only 36 months (Ayandibu and Houghton, 2017; Masama, 2017; Bruwer et al. 2017; Bruwer and Coetzee, 2016). Although the failure of South African SMMEs are caused by several factors, previous studies (Van Calker et al., 2005; Jeon et al., 2010; Lebacq et al., 2013; Mwanza, 2017; Bruwer and Van Den Berg, 2017; Renault et al., 2018) support the notion that when most of these business entities fail, it is usually due to their inability to remain sustainable, particularly with the attainment of relevant economic objectives.

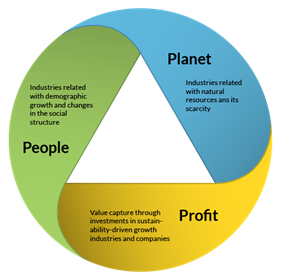

Sustainability refers to the expected long-term continuation of a business entity by properly executing economic, social and/or environmental responsibilities to achieve economic, social and/or environmental objectives (Buys, 2012; Bechtold et al., 2013). The proper execution of these applicable responsibilities to achieve relevant business objectives is strongly related to the Triple Bottom Line framework (Elkington, 1998), as depicted in Figure 1.

Figure 1. The Triple Bottom Line framework

Source: Vallis (2019)

Notwithstanding the above, economic objectives are regarded as fundamental objectives which need to be achieved by business entities to remain operational in the foreseeable future (Villalonga, 2004; Isaksson, 2006; Edwards, 2009; Nhemachena and Murimbika, 2018). Examples of such objectives include being profitable (income exceeds expenses); being solvent (positive net asset value); being liquid (to have sufficient cash on hand); and being reputable among applicable stakeholders (to be in good standing with suppliers, customers and investors). To this end, since any business entity needs to achieve its economic objectives first before it can achieve its social and environmental objectives, the inference can be made that majority of South African SMMEs are not achieving their relevant economic objectives

The view above is supported by previous studies (Kabiawu 2013; Wiese, 2014) where it was found that the economic sustainability of South African SMMEs is weak when compared to SMMEs in operation in other countries. Moreover, taking into account the statistics evident in Table 2, it appears that more South African SMMEs were failing every month in the mid-2010s when compared to those that failed in the early-2000s.

Table 2. South African SMME failure rates between 2000 and 2014

| Period | Estimated failure rate | Failure timeframe |

| 2000 – 2004 | 70 per cent | 48 months |

| 2005 – 2009 | 75 per cent | 42 months |

| 2010 – 2014 | 75 per cent | 36 months |

Sources: Van Eeden et al. (2003); Biyase (2009); Fatoki and Odeyemi (2010); Mutezo (2013); Cant and Wiid (2013); Moloi (2013); Bruwer and Van Den Berg (2017)

Previous studies (Smit, 2012; Sin and Ng, 2013; Siwangaza, 2013; Masama, 2017; Petersen, 2018) suggest that the high South African SMME failure rate can be blamed on these business entities’ non-management of economic factors and subsequent risks. Examples include the scarcity of business skills, volatile and unfavourable exchange rates, increased costs of water and electricity, strict government legislation, high levels of crime and volatile supplies and/or demands for products and/or services (SAICA, 2015; Bruwer, 2016). One manner in which economic factors and their associated risks can be managed is through establishing sound internal control.

b. Internal Control and Internal Control Systems

Internal control was first formally defined in 1992 by the Committee of Sponsoring Organisations (COSO) as follows: “It is a process, effected by a company’s board of directors, management and other personnel, designed to provide reasonable assurance regarding the achievement of objectives relating to the effectiveness and efficiency of operations, the reliability of financial reporting, and the compliance with applicable laws and regulations” (COSO, 1992)

In lay, internal control has to do with a logical sequence, as implemented by a business’ management that can be used to mitigate risks to provide reasonable assurance surrounding the achievement of the relevant business’ objectives (IIA, 2009; Mensah, 2011, Frazer, 2012). One of the best manners in which internal control can be established in a business entity is through using internal control frameworks Gyebi and Quain, 2013; Ejoh and Ejom, 2014). Three of the most used internal control frameworks include the COSO Integrated Internal Control framework, the Criteria of Control (CoCo) framework and the CoBIT framework (CICA, 1995; Spira and Page, 2003; Debreceny et al., 2003; Moeller, 2007; Tuttle and Vandervelde, 2007; Pfister, 2009; Bernroider and Ivanov, 2011). Out of these three internal control frameworks however, the COSO Integrated Internal Control framework is the most popular, as shown in Figure 2.

Figure 2. The COSO Integrated Internal Control Framework

Source: COSO (2013)

The COSO Integrated Internal Control framework suggests that internal control can be cultivated in a business though means of applying a sound system of internal control (Abba and Kakanda, 2017; Irvan et al., 2017). Such a system of internal control typically comprises five inter-related control elements (Coetzee, 2006; Abu-Musa, 2007; Martin et al., 2014) namely: 1) control environment (the attitude of management regarding internal control); 2) risk assessment (the identification and evaluation of risks); 3) internal control activities (the activities to help prevent and detect risks); 4) information and communication (the dissemination of applicable information related to internal control through appropriate media to assist stakeholders to achieve their applicable objectives); and 5) monitoring (the evaluation of the overall soundness of the entire system of internal control).

Although originally developed for implementation in large business entities, attempts have been made by researchers and policymakers to simplify the content of COSO Integrated Internal Control Framework for implementation in smaller business entities (Moeller, 2007; Gao and Jia, 2015; Vovchenko et al. 2017). Regardless of these attempts, research shows that small businesses, particularly those in South Africa, do not widely make proper use of this framework (Bruwer et al., 2013; Masama, 2017). This is supported by the findings in local research studies (Siwangaza, 2013; Bruwer and Van Den Berg, 2015; Siwangaza and Dubihlela, 2016).

4. The Sustenance Framework

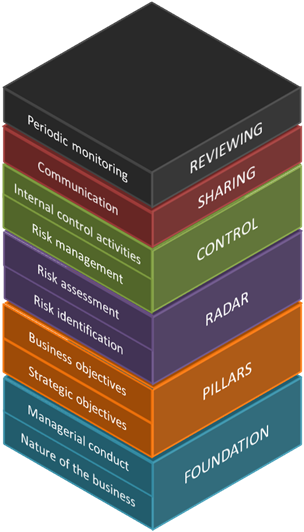

The COSO Integrated Internal Control framework was used as a foundation to develop the Sustenance framework. From a South African SMME perspective, in particular, two inherent weaknesses observed in the COSO Integrated Internal Control framework include: 1) limited guidance exists as to how the “control environment”, the foundation of any system of internal control, is to be properly set and qualitatively measured and 2) no reference is made to the setting of objectives which, in turn, may be subjective to applicable risks. For the remainder of this section, the Sustenance framework is first depicted in Figure 3, after which each of its components is explained.

Figure 3. The Sustenance framework

Source: Author

Foundation: A business is a vivid and clear reflection of its management (Gerber, 1995). Not only should management be aware of the nature of their business, but they should also be aware of their managerial conduct (Bruwer, 2016; Bruwer and Siwangaza, 2016; Bruwer et al., 2018a). Management should, therefore, be very aware of: 1) what their business stands for, 2) why their business was started, 3) where their business operates, 4) how their business operates, 5) whom their business serves, 6) their core values used when managing and 7) the manner in which they manage (managerial operating style).

Pillars: Clear objectives must be set. Objective-setting is a prerequisite for establishing a plan of action as to how a business should conduct its business (Dvoryadkina et al., 2019). Here, management needs to set and/or evaluate is business entity’s vision, mission, strategic objectives and other business-related objectives.

Radar: Management should identify possible events that may or may not happen that can adversely affect the achievement of their business’ vision, mission, strategic objective and other business-related objectives. This is needed as all possible ‘what-can-go-wrong’ scenarios should be considered which may affect the achievement of relevant business objectives (Bruwer et al., 2018b; Masama and Bruwer, 2019). Following this, all identified risks should be assessed concerning their potentially harmful impact and frequency of occurrence, if left unmanaged.

Control: All identified and assessed risks should be properly controlled through preventive measures, detective measures and/or corrective measures. Research suggests (Smit, 2012; Masama, 2017; Ekegbo et al., 2018; Petersen et al., 2018) that risks with a low impact and low frequency should be accepted, risk with a low impact and high frequency should be mitigated, risk with high impact and low frequency should be shared and risk with high impact and high frequency should be avoided. Those risks that should be mitigated should take into account activities such as document usage and design, segregation of duties, independent checks, proper authorisation and/or the safeguarding of assets (Bruwer, 2016).

Sharing: The information related to the “Foundation”, “Pillars”, “Radar” and “Control” segments of the framework, as known by management, should be made available to relevant internal stakeholders, where applicable. A rule of thumb to follow is that where knowledge of such information can assist internal stakeholders to perform his/her/its duties to, in turn, achieve relevant business objectives. It should be shared accordingly.

Reviewing: It should be decided when to review the answers provided by management for each of the segments above, namely: “Foundation”, “Pillars”, “Radar”, “Control” and “Sharing”. As change is a constant in the world of business, it is recommended that reviews take place on a periodical basis.

To assist with the implementation of the Sustenance framework, it is suggested that the management answers the questions posed in Table 3. For the best results, it is suggested that management is as detailed as possible when providing answers.

Table 3. Recommended questions for management to answer for each segment of the Sustenance framework

| Stage | Questions |

| Foundation |

|

| Pillars |

|

| Radar |

|

| Control |

|

| Share |

|

| Review |

|

Sources: Author

5. Conclusion

SMMEs are of vital importance to the South African economy. This is particularly supported by their socio-economic value added regarding the creation of jobs, the eradication of poverty and the equal dissemination of wealth. Unfortunately, academic research suggests that these business entities have among the highest failure rates in the world. The latter dispensation is generally blamed on the non-management of economic factors and related risks. One manner in which economic factors and risks can be managed is through means of internal control.

Internal control has to do with the providence of reasonable assurance, to management, that relevant business objectives will be achieved in the foreseeable future. This can be executed through means of a sound system of internal control which, in turn, can be implemented with the assistance of an internal control framework.

Among the internal control frameworks in existence, perhaps the most popular one in use is the COSO Integrated Internal Control Framework. Even though measures have been put in place to simplify the foregoing internal control framework, for adoption by SMMEs, many South African SMMEs, widely, do properly make use of this framework. This may be a reason as to why the sustainability of South African SMMEs is regarded among the worst in the world.

Taking into account the limited utilisation of the COSO Integrated Internal Control framework by South African SMMEs, including two inherent limitations of the framework, the Sustenance framework was developed as an artefact hypothesis for adoption by these business entities. Further empirical testing of the Sustenance framework is encouraged as an avenue for further research.

References

- Abba, M. and Kakanda, M., 2017. Moderating effect of internal control system om the relationship between government revenue and expenditure. Asian Economic and Financial Review, 7(4), pp.381-392.

- Abu-Musa, A., 2007. Evaluating the security controls of CAIS in developing countries: an examination of current research. Information Management and Computer Security, 15(1), pp.46-63.

- Adeniyi, A. and Aramide, A., 2014. Enhancing the performance of electricity distribution companies in Nigeria via internal control system. Research Journal of Finance and Accounting, 5(22), pp.197-214.

- Ayandibu, A. and Houghton, J., 2017. The role of small and medium scale enterprise in local economic development (LED). Journal of Business and Retail Management Research, 11(2), pp.133-139.

- Bechtold., J., Kaspereit, T., Kirsch, N., Lyakina, Y., Seib, S., Spiekermann, S. and Stengert, K., 2013. Corporate sustainability in the estimation of financial distress likelihood – Evidence from the world stock markets during the financial crisis. Research Journal of Financial and Accounting, 4(5), pp.205-211.

- Bernroider, E.W.N. and Ivanov, M., 2011. IT project management control and the Control Objectives for IT and related Technology (CobiT) framework. International Journal of Project Management, 29(3), pp.325-336.

- Biyase, L., 2009. DTI to look at how crisis hurts small enterprises [Online]. Available from: http://www.highbeam.com/doc/1G1-198340345.html [Accessed on 24/10/2019].

- Boote, D. N. and Beile, P., 2005. Scholars before researchers: On the centrality of the dissertation literature review in research preparation. Educational Researcher, 34 (6), pp.3–15.

- Brustbauer, J., 2016. Enterprise risk management in SMEs: towards a structural model. International Small Business Journal, 34(1), pp.70-85.

- Bruwer, J.-P. and Coetzee, P., 2016. A literature review of the sustainability, the managerial conduct of management and the internal control systems evident in South African small, medium and micro enterprises. Problems and Perspectives in Management, 14(2), 201-211.

- Bruwer, J.-P. and Siwangaza, L. (2016). Is the Control Environment a basis for Customised Risk Management Initiatives in South African Small, Medium and Micro Enterprises?. Expert Journal of Business and Management, 4(2), pp.105-117.

- Bruwer, J.-P. and Van Den Berg, A., 2015. The influence of the control environment on the sustainability of fast food Micro and Very Small Enterprises operating in the Northern suburbs. Journal of Leadership and Management Studies, 2(1), pp.50-63.

- Bruwer, J.-P. and Van Den Berg, A., 2017. The Conduciveness of the South African Economics Environment and Small, Medium and Micro Enterprise Sustainability: A Literature Review. Expert Journal of Business and Management, 5(1), pp.1-12.

- Bruwer, J.-P., Coetzee, P. and Meiring, J., 2017. The empirical relationship between the managerial conduct and internal control activities. South African Journal of Economic and Management Studies, 20(1), pp.1-19.

- Bruwer, J-P., 2016. The relationship(s) between the managerial conduct and the internal control activities of South African fast moving consumer goods SMMEs. Unpublished DTech: Internal Auditing thesis, Cape Peninsula University of Technology, Cape Town, South Africa.

- Bruwer, J-P., Coetzee, P. and Meiring, J., 2018a. Can internal control activities and managerial conduct influence business sustainability? A South African SMME perspective. Journal of Small Business and Enterprise Development, 25(5), pp.710-729.

- Bruwer, J-P., Masama, B., Mgidi, A., Myezo, M., Nqayi, P., Nzuza, N., Phangwa, M., Sibanyoni, S. and Va, N., 2013. The need for a customised risk management framework for small enterprises. Southern African Accounting Association, Somerset West, South Africa, 26 – 28 June, pp.999-1030

- Bruwer, J-P., Siwangaza, L. and Smit, Y., 2018b. Loss control and loss control strategies in SMMEs operating in a developing country: A Literature Review. Expert Journal of Business Management, 6(1), pp.1-11.

- Buhr, N. and Gray, R., 2012. Environmental management, measurement, and accounting: information for decision and control?. Oxford, UK: Oxford University Press.

- Buys, J. A., 2012. A conceptual framework for determining sustainability of SMMEs in Lesedi. Unpublished Manuscript (thesis), North West University, Potchefstroom.

- Cant, M. and Wiid, J., 2013. Establishing the challenges affecting South African SMEs. International Business and Economics Research Journal, 12(6), pp.707-716.

- Cant, M.C., 2017. Do Small, Medium and Micro Enterprises have the capacity and will to employ more people: Solution to unemployment of just a pipe dream?. International Review of Management and Marketing, 7(3), pp.366-372.

- Caratas, M. and Spatariu, E., 2014. Contemporary approaches in internal audit. Procedia Economics and Finance, 15(1), pp.530-537.

- Chang, H.J., 2011. Institutions and economic development: theory, policy and history. Journal of Institutional Economics, 7(4), pp.473-498.

- CICA,1995. Guidance on control Toronto: Canadian Institute of Chartered Accountants.

- Coetzee, G., 2006. Effect of HIV/AIDS on the control environment. Perspectives in Public Health, 126(4), pp.183-190.

- COSO, 1992. Internal control – integrated framework. Jersey City, NJ: Committee of Sponsoring Organizations of the Treadway Commission.

- COSO, 2005. Guidance for smaller public companies reporting on internal control over financial reporting [Online]. Available from: https://www.icjce.es/images/pdfs/TECNICA/C03%20-%20AICPA/C311%20-%20Estudios%20y%20Varios/COSO%20-%20ED%20re%20IC%20Guidance%20-%20Oct%202005.pdf [Accessed on 24/10/2019].

- COSO, 2013. Internal control – integrated framework: executive summary. [Online]. Available from: https://na.theiia.org/standards-guidance/topics/Documents/Executive_Summary.pdf [Accessed on 25/10/2019].

- Debreceny, R., Gray, G.L., Tham, W., Goh, K. and Tang, P., 2003. The development of embedded audit modules to support continuous monitoring in the electronic commerce environment. International Journal of Auditing, 7(2), pp.169-185.

- Dvoryadkina, E.B., Antipin, I.A. and Kaibicheva, E.I., 2019. Objective-Setting is the necessary stage for strategic development of a new industrial city. 2nd International Scientific conference on New Industrialization: Global, national, regional dimension (SICNI 2018), Ekaterinburg, Russia, December 4-5.

- Eatwell, J. and Taylor, L., 2000. Global finance at risk: the case for international regulation. New York, NY: New Press.

- Edwards, M., 2009. An integrative metatheory for organisational learning and sustainability in turbulent times. The Learning Organization, 16(3), pp.189-207.

- Ejoh, N. and Ejom, P., 2014. The impact of internal control activities on financial performance of tertiary institutions in Nigeria. Journal of Economics and Sustainable Development, 5(16), pp.133-143.

- Ekegbo, T-V., Quede, B., Mienahata, C., Siwangaza, L., Smit, Y. and Bruwer, J-P., 2018 Shrinkage risk management initiatives in retail SMMEs operating in the Cape Town City Bowl. International Conference on Business and Management Dynamics, Cape Town, South Africa, 28 – 31 August.

- Elkington, J., 1998. Partnerships from cannibals with forks: The triple bottom line of 21st‐century business. Environmental Quality Management, 8(1), pp.37-51.

- Fatoki, O. and Odeyemi, A., 2010. Which new small and medium enterprises in South Africa have access to bank credit?. International Journal of Business and Management, 5(10), pp.128-136.

- Fink, A., 2013. Conducting research literature reviews: from the Internet to paper. Thousand Oaks, CA: Sage Publications.

- Frazer, L., 2012. The effect of internal control on the operating activities of small restaurants. Journal of Business and Economics Research, 10(6), pp.361-373.

- Gao, X. and Jia, Y., 2015. The role of internal control in equity issue market: evidence from seasoned equity offerings. Journal of Accounting, Auditing and Finance, 32(3), pp.303-328.

- Gerber, M.E., 1995. The e-myth revisited: why most small businesses don’t work and what to do about it. New York, NY: Collins Business.

- Gyebi, F. and Quain, S., 2013. Internal control on cash collection: a case of the Electricity Company of Ghana Ltd, Accra East Region. International Journal of Business and Social Science, 4(9), pp.217-233.

- Hill, H., 2001. Small and medium enterprises in Indonesia: old policy challenges for a new administration. Asian Survey, 41(2), pp.248-270.

- IIA., 2009. IIA Position Paper: The role of internal auditing in enterprise-wide risk management [Online]. Available from https://global.theiia.org/standards-guidance/Public%20Documents/PP%20The%20Role%20of%20Internal%20Auditing%20in%20Enterprise%20Risk%20Management.pdf [Accessed on 25/10/2019].

- Irvan, N., Mus, A., Su'un, M. and Sufri, M., 2017. Effect of Human Resource Competencies, Information Technology and Internal Control Systems on Good Governance and Local Government Financial Management Performance. Institute of Research Advances, 8(1), pp.31-45.

- Isaksson, R., 2006. Total quality management for sustainable development: process-based system models. Business Process Management Journal, 12(5), pp.632-645.

- Jeon, C.M., Amekudzi, A.A. and Guensler, R.L., 2010. Evaluating plan alternatives for transportation system sustainability: Atlanta metropolitan region. International Journal of Sustainable Transportation, 4(4), pp.227-247.

- Jones, G.G. and Wadhwani, R.D., 2006. Schumpeter’s plea: rediscovering history and relevancy in the study of entrepreneurship. Working Paper 06-036, Harvard Business School.

- Kabiawu, O., 2013. Designing a knowledge resource to address bounded rationality and satisficing for ICT decisions in small organisations. Unpublished thesis, University of Cape Town, Cape Town, South Africa.

- Kai-Sun, K., 1997. Private participation with strong government control: Hong Kong. In Mody, A. (ed.). Infrastructure strategies in East Asia: the untold story. Washington, DC: World Bank, pp.51-68.

- Karmakar, M., 2006. Stock market volatility in the long run, 1961–2005. Economic and Political Weekly, 41(18), pp.1796-1802.

- King, R.G. and Levine, R., 1993. Finance and growth: Schumpeter might be right. Quarterly Journal of Economics, 108(3), pp.717-737.

- Kongolo, M., 2010. Job creation versus job shedding and the role of SMEs in economic development. African Journal of Business Management, 4(11), pp.2288-2295.

- Lebacq, T., Baret, P. and Stilmant, D., 2013. Sustainability indicators for livestock farming: a review. Agronomy for Sustainable Development, 33(2), pp.311-327.

- Lima, M. and Berryman, A.A., 2011. Positive and negative feedbacks in human population dynamics: future equilibrium or collapse?. Oikos, 120(9), pp.1301-1310.

- Martin, K., Sanders, E. and Scalan, G., 2014. The potential impact of COSO internal control integrated framework revision on internal audit structured SOX work programs. Research in Accounting Regulation, 26(1), pp.110-117.

- Masama, B., 2017. The utilisation of Enterprise Risk Management in fast food Small, Medium and Micro Enterprises operating in the Cape Peninsula. Unpublished Manuscript (thesis), Cape Peninsula University of Technology, Cape Town.

- Masama, B. and Bruwer, J.-P., 2018. Revisiting the economic factors which influence fast food South African Small, Medium and Micro Enterprise sustainability. Expert Journal of Business Management, 6(1), pp.19-30.

- Mensah, B.E., 2011. Assessing the effectiveness of internal control systems in public institutions: a case study of Takoradi Polytechnic. Unpublished Manuscript (thesis), Kwame Nkrumah University of Science and Technology, Ghana.

- Moeller, R., 2007. Enterprise risk management: understanding the new integrated ERM framework. Hoboken: John Wiley.

- Molapo, S., Mears, R.R. and Viljoen, J.M.M., 2008. Developments and reforms in Small Business Support Institutions since 1996. Professional Accountant, 8(1), pp.27-40.

- Moloi, N., 2013. The sustainability of construction small-medium enterprises (SMEs) in South Africa. Unpublished Manuscript (dissertation), University of Witwatersrand, Johannesburg.

- Mouloungui, S., 2012. Assessing the impact of finance on small business development in Africa: the cases of South Africa and Gabon. Unpublished Manuscript (dissertation), Twsane University of Technology, Pretoria.

- Mukata, C.M. and Swanepoel., E., 2017. Development support for small and medium enterprises in the financially constrained north-eastern regions of Namibia. Southern African Business Review, 21(1), pp.198-221.

- Mutezo, A., 2013. Credit rationing and risk management for SMEs: the way forward for South Africa. Corporate Ownership and Control, 10(2), pp.153-163.

- Mwanza, P.M., 2018. Utilisation of budgets by Small and Medium Enterprises in the manufacturing industry in the Cape Metropole. Unpublished Manuscript (thesis), Cape Peninsula University of Technology, Cape Town.

- Nhemachena, C. and Murimbika, M., 2018. Motivations of sustainable entrepreneurship and their impact of enterprise performance in Gauteng Province, South Africa. Business Strategy and Development, 1(2), pp.115-127.

- Panfilov, V.S., 2012. Transformation of the reproductive mechanism of the world economy and prospects for Russia’s socioeconomic development. Studies on Russian Economic Development, 23(4), pp.327-339.

- Park, H.J., 2001. Small businesses in Korea, Japan and Taiwan. Asian Survey, 41(5), pp.846-864.

- Petersen, A., 2018. The effectiveness of internal control activities to combat occupational fraud risk in fast moving consumer goods Small, Medium and Micro Enterprises (SMMEs) in the Cape Metropole. Unpublished Manuscript (thesis), Cape Peninsula University of Technology, Cape Town.

- Petersen, A., Bruwer, J-P. and Le Roux, S., 2018. Occupational fraud risk, internal control initiatives and the sustainability of Small, Medium and Micro Enterprises in a developing country: A Literature Review. Acta Universitatis Danubius Economica, 14(4), pp.567-580.

- Pfister, J.A., 2009. Managing organizational culture for effective internal control: from practice to theory. Heidelberg: Physica.

- Reiter, B., 2017. Theory and Methodology of Exploratory Social Science Research. International Journal of Science and Research Methodology, 5(4), pp.129-150.

- Renault, B., Agumba, J. and Ansary, N., 2018. An exploratory factor analysis of risk management practices: A study among small and medium contractors in Gauteng. Acta Structilia, 25(1), pp.1-39.

- Republic of South Africa, 1996. National Small Business Act No. 102 of 1996. Pretoria: Government Printer.

- Republic of South Africa, 2003. National Small Business Amendment Act No. 26 of 2003. Pretoria: Government Printer.

- Republic of South Africa, 2019. Revised Schedule 1 of the National Definition of Small Enterprise in South Africa. Government Gazette No. 42304, 15 March 2019. Government Printer, Pretoria.

- Rogerson, C., 2008. Tracking SMME Development in South Africa: Issues of Finance, Training and the Regulatory Environment. Urban Forum, 19(1), pp.61-81.

- Romer, C.D., 1999. Changes in business cycles: evidence and explanations. Journal of Economic Perspectives, 13(2), pp.23-44.

- Safii, 2018. National Small Business Amendment Act No. 26 of 2003 [Online]. Available from http://saflii.org/za/legis/num_act/nsbaa2003331.pdf [Accessed on 24/10/2019].

- SAICA, 2015. 2015 SME insights report [Online]. Available from http://www.saica.co.za/Portals/0/documents/SAICA_SME.PDF [Accessed on 24/10/2019].

- Schumpeter, J.A., 1947. The creative response in economic history. Journal of Economic History, 7(2), pp.149-159, November.

- Sin, I. and Ng, K., 2013. The evolving building blocks of enterprise resilience: ensnaring the interplays to take the helm. Journal of Applied Business and Management Studies, 4(2), pp.1-12.

- Siwangaza, L., 2013. The status of internal controls in fast moving consumer goods SMMEs in the Cape Peninsula. Unpublished manuscript (thesis), Cape Peninsula University of Technology, Cape Town.

- Siwangaza, L. and Dubihlela, J., 2016. Effects of internal organisational environments on preventative, detective and directive internal controls of SMMEs in Cape Town. Southern African Accounting Association, Cape Town.

- Smit, Y. and Watkins, A., 2012. A literature review of small and medium enterprises (SME) risk management practices in South Africa. African Journal of Business Management, 6(21), pp.6324-6330.

- Smit, Y., 2012. A structured approach to risk management for South African SMEs. Unpublished Manuscript (thesis), Cape Peninsula University of Technology, Cape Town.

- Spira, L. and Page, M., 2003. Risk management: The reinvention of internal control and the changing role of internal audit. Accounting, Auditing and Accountability Journal, 16(4), pp.640-661.

- Staikouras, S.S., 2006. Financial intermediaries and interest rate risk: II. Financial Markets, Institutions and Instruments, 15(5), pp.225-272.

- Statistics South Africa., 2017a. Gross domestic product, 4th quarter 2016 [Online]. Available from http://www.statssa.gov.za/publications/P0441/GDP_presentation-Q4_2016.pdf [Accessed on 24/10/2019].

- Statistics South Africa., 2017b. Quarterly Labour Force Survey [Online]. Available from http://www.statssa.gov.za/publications/P0211/P02111stQuarter2017.pdf [Accessed on 24/10/2019].

- Stokes, D. and Wilson, N., 2010. Small business management and entrepreneurship. 6th ed. Andover: Cengage Learning.

- Tarantino, A. and Cernauskas, D., 2011. Essentials of risk management in finance. Hoboken, New Jersey: John Wiley.

- Timm, S., 2011. How South Africa can boost support to small businesses: lessons from Brazil and India [Online]. Available from: http://www.tips.org.za/files/india_brazil_2011_edit_s_timm.pdf [Accessed on 24/10/2019].

- Tuttle, B. and Vandervelde, S., 2007. An empirical examination of COBIT as an internal control framework for information technology. International Journal of Accounting Information Systems, 8(4), pp.240-263.

- Vallis, 2019. Sustainability as a business opportunity [Online]. Available from: https://www.vallis.pt/vsiConceito.do [Accessed on 25//10/2019].

- Van Calker, K., Beremtsen, P., Giesem, G. and Huime, R., 2005. Identifying and ranking attributes that determine sustainability in Dutch dairy farming. Agriculture and Human Values, 22(1), pp.53-63.

- Van Eeden, S., Viviers, S. and Venter, D., 2003. A comparative study of selected problems encountered by small businesses in the Nelson Mandela, Cape Town and Egoli metropoles. Management Dynamics, 12(3), pp.13-23.

- Vawda, M., Padia, N. and Maroun, W., 2013. Islamic banking in South Africa: an exploratory study of perceptions and bank selection criteria. Proceedings of the Biennial Southern African Accounting Association Conference, Somerset West, South Africa, 26–29 June, pp.941-973.

- Villalonga, B., 2004. Intangible resources, Tobin's q, and sustainability of performance differences. Journal of Economic Behaviour and Organization, 54(2), pp.205-230.

- Vovchenko, N., Holina, M., Orobinksiy, A. and Sichev, R., 2017. Ensuring Financial Stability of Companies on the Basis of International Experience and Construction of Risks Maps, Internal Control and Audit. European Research Studies, 20(1), pp.350-368.

- Wiese, J., 2014. Factors determining the sustainability of selected small and medium-sized enterprises. Unpublished Manuscript (dissertation), North-West University, Potchefstroom.

- Wren, C. and Storey, D.J., 2002. Evaluating the effect of soft business support upon small firm performance. Oxford Economic Papers, 54(2), pp.334-365.

Article Rights and License

© 2020 The Author. Published by Sprint Investify. ISSN 2359-7712. This article is licensed under a Creative Commons Attribution 4.0 International License.