Keywordsenvironmental green microfinance microcredit microfinance MSMEs

JEL Classification E00, M20

Full Article

1. Introduction

Environmental risk stands as a pressing global challenge today (Ossebaard and Lachman, 2021). Human activities are the primary drivers of environmental problems, with mitigation efforts predominantly focused on large corporations, often overlooking micro, small, and medium-sized enterprises (MSMEs). Although individual actions by MSMEs may seem inconsequential, their cumulative impact is substantial (Singh et al., 2019). Climate change threatens MSMEs, individuals, and households, undermining their financial stability (Satterthwaite et al., 2018).

The UN's three-decade commitment to Conference of the Parties (COP) global climate summits shows that environmental awareness has gained international recognition. These gatherings address climate change and environmental imbalances exacerbated by anthropogenic activities.

In 2009, rich countries pledged to raise $100 billion by 2020 to assist vulnerable nations in mitigating environmental challenges. However, at the time of this investigation, this commitment remains unfulfilled (Robert and Schleyer-Lindenmann, 2021; Chowdhury and Tadjoeddin, 2023). This underscores the Conference of the Parties' recommendation for developing countries to formulate their Nationally Determined Contributions (NDCs) with reduced reliance on wealthy nations. It implies that developing countries must devise pragmatic measures to establish national programs addressing environmental problems and climate change.

Ghana, for instance, implemented its Environmental and Social Risk Management (ESRM) legislative framework for green financing in November 2019, focusing primarily on commercial banks. This approach, effective for large-scale enterprises regulated by government institutions, has limited coverage for MFIs, which predominantly fund dispersed, often unregistered, and less regulated MSMEs (Agyapong, 2020; Boon and Yeboah, 2018).

In the realm of microfinance, some experts, donors, and international organizations posit that MFIs can play a role in fostering environmentally friendly attitudes among their MSME clients (Allet, 2012). Every economy relies on MSMEs for job creation, economic growth, productivity, and poverty reduction. Their ability to innovate products and processes can considerably impact national financial well-being (Madrid-Guijarro et al., 2009). The expansion of these enterprises reinforces the economic fabric of emerging countries, with global recognition for their role in sustainable grassroots economic development (Pandya, 2012).

On a global scale, MSMEs account for approximately 95% of enterprises worldwide and 60% of private sector jobs (Ayyagari et al., 2007). The United Nations Industrial Development Organization (UNIDO), highlights that over 90% of African enterprises are MSMEs. In Ghana, MSMEs contribution to GDP surged by 49% in 2012 (PWC, 2013). According to Abor and Quartey (2010), Ghana's MSMEs form approximately 92% of businesses, create about 85% of manufacturing jobs, and contribute nearly 70% to GDP.

Gakpo, Wujangi, Kwakye, and Asante (2021) emphasize the role of Ghana's MSME sector in employment creation and poverty reduction. According to Chetama et al. (2016), a thriving MSME sector is critical for poverty reduction and growth, especially in Sub-Saharan Africa. Liedholm and Mead (2005) used surveys from many African nations to estimate that 17%–27% of the working population is employed by MSMEs, approximately twice as many as large firms and the governmental sector. USAID (2010) later reported that MSMEs employ a third or more of low-income countries' labour force.

However, despite their significant contributions, it is evident that many operational activities of MSMEs contribute to ecological issues such as species extinction, land degradation, deforestation, poor waste disposal, and pollution (Brahmbhatt, Haddaoui and Page, 2017). Addressing the environmental impact of MSMEs becomes imperative in fostering sustainable growth and development.

The European Commission (EC) (2022) reports that over 23 million SMEs in the EU account for 63% of overall company carbon footprints. SMEs generate nearly 50% of Europe's GDP and 100 million jobs. In Europe, SMEs account for 60 to 70% of aggregate pollution, constituting nearly 99% of companies (Yadav et al., 2018; European Commission, 2014). UNIDO notes that MSMEs make up more than 90% of all registered African enterprises, providing over 80% of job avenues. Given their significant environmental footprint, it is crucial to ensure that MSMEs in Africa are environmentally sensitive.

MFIs help MSMEs grow by providing loans, savings, insurance, remittances, and other non-financial services. As financial intermediaries for MSMEs, MFIs have the potential to influence and reposition MSMEs to incorporate environmental concerns into their goals and operations. The growing desire for MFIs to integrate environmental issues into their operating strategies is evident in the literature (Allet and Hudon, 2015; Mia et al., 2018; Allet, 2014). Therefore, this study aims to investigate the perceived ability of microfinance institutions to influence MSMEs to adopt green operations.

Research on green microfinance (GM) has diverse focal points, including the sustainability of MFIs, the environmental and social performance of MSMEs, and the sustainable environmental performance of MSMEs (Atahau et al., 2021; Abid and Kacem, 2018, Allet, 2014). This study aims to offer a comprehensive review, delving into the potential of GM to steer MSMEs towards adopting green practices in manufacturing and services.

The following sections of the paper provide a comprehensive literature assessment on microfinance concept, the triple bottom line, and green microfinance. The next section explains the methodology employed for the study, followed by a discussion of MSMEs' definition, environmental impacts, the potential of GM to inspire sustainable practices, microfinance institutions' influence on MSMEs to go green, and MSMEs' environmental consciousness. In conclusion, the article summarizes key observations and provides relevant recommendations.

2. Theoretical Framework of Microfinance Concept

In the 1970s, Professor Muhammad Yunus introduced microfinance. According to this theory, the poor are capable of utilizing credit to generate enough income to repay a loan and its associated interest under appropriate conditions. Additionally, this approach aims to stabilize income, smoothen consumption, protect against risk, facilitate asset acquisition, and ultimately alleviate poverty (Zhang and Posso, 2019; Khan, Ahmad and Shireen, 2021).

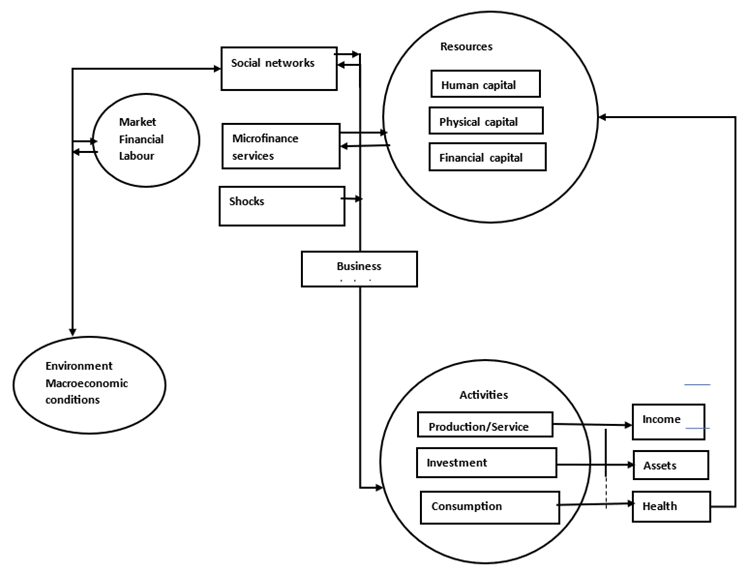

Lack of collateral and inability to meet traditional credit conditions prevent the poor from getting mainstream bank loans (Zhang and Posso, 2019). Consequently, the impoverished turn to alternative sources, relying on family, friends, neighbours, traders, rotating savings and credit associations, and, to a greater extent, moneylenders for financial assistance (Egbide, 2020). Unfortunately, moneylenders often impose usurious interest rates, exacerbating the financial hardships of the poor. In response to this issue, the concept of microcredit emerged to address this issue by lending money to micro and small entrepreneurs and economically engaged people without access to traditional banking services (Egbide, 2020). Figure 1 shows a schematic representation of microfinance. The notion of microfinance evolved from microcredit by integrating savings, insurance, money transfer, and other non-financial services(Cosgrove, 2021; Moyo, 2020, Kyereboah-Coleman and Osei, 2008, Obaidullah, 2008).

Figure 1: Schematic representation of the microfinance concept

Source: Adapted from Nghiem (2005)

2.1 The Triple Bottom Line Theory

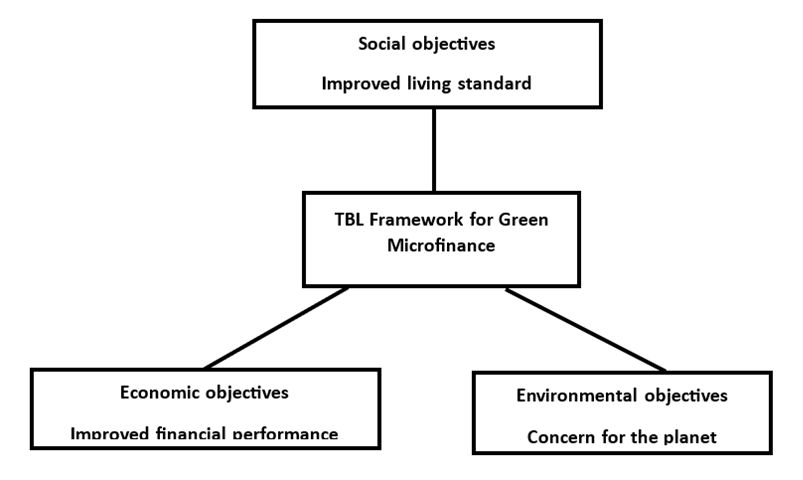

One of the theories supporting sustainability of MSMEs is triple bottom-line framework. John Elkington propounded this theory in 1994 to encourage firms to balance environmental, financial, and social responsibility. He believed firms should issue three reports. These included the traditional corporate financial report, social and environmental responsibility reports of the firm. (Hindle 2008). The triple bottom line framework is shown in figure 2.

Figure 2: Triple bottom line framework of Green Microfinance

Source: Developed by the researcher from literature

Triple bottom line encourages firms to consider both financial advantages and the impact of their activities on the environment and society, which can be raised or lessened (Shou, Shao, Lai, Kang, and Park, 2019). The term "triple bottom line" is the set of concepts, issues, and procedures a company must follow to maximize economic, social, and environmental value while reducing negative impacts. Allet (2014) defines the triple bottom line as a business concept in which organizations track their social and environmental impact as well as their financial success. According to Majid and Koe (2012), the "Triple Bottom Line" structure is divided into "3Ps" that stand for concern for profit, people, and the planet.

2.2 Green Microfinance

GM is a developing research topic that aims to broaden the scope of microfinance to include environmental concerns. In recent years, the term "green microfinance" has come to refer to the practice of MFIs incorporating environmental sustainability themes into their operations and promoting environmentally friendly activities and solutions. Meanwhile, traditionally, microfinance has two goals: economic and social.

GM is a unique strategy that has received little attention in Sub-Saharan Africa, particularly Ghana (Abid and Kacem, 2018). GM incorporates environmental issues into the financial and social goals of microfinance, shifting the paradigm from a double bottom line to a triple bottom line (Allet, 2014). GM attempts to impact the decision-making and behaviour of MFIs, as well as the behaviour of MSMEs who are predominantly MFI clients (Huybrechs, Bastiaensen, and Forcella, 2015). GM either prohibits credit for non-eco-friendly businesses or vigorously designs loan programs to boost pro-environmental firm activity to minimize MSMEs' environmental sensitivity. GM attempts to reduce the environmental impact of business actions, assist in decreasing monetary risk, improve standard of living, and/or conserving and restoring natural resources (Huybrechs et al., 2015).

Contemporary microfinance experts continue to argue for GM, which promotes environmental responsibility alongside social and financial goals. This means MFIs should consider the "Triple Bottom Line" when serving their numerous clients (Allet, 2014).

3. Methodology

The methodology employed for this study aimed to conduct a thorough and scientific literature review to ensure a comprehensive analysis of the subject matter. The process involved accessing multiple online databases renowned for scholarly publications, including Elsevier, Google Scholar, PROQUEST, EMERALD, Science Direct, Research Gate, IEEE, and JSTOR. The choice of these databases was strategic, encompassing a diverse range of disciplines to gather relevant information and valuable insights related to the study's focus on GM and its potential impact on inspiring MSMEs to adopt environmentally friendly practices.

The literature review was designed as a systematic and exhaustive search, adhering to established research methodologies to enhance the reliability and validity of the findings. The objective was to collate a broad spectrum of scholarly articles, research papers, conference proceedings, and other relevant publications to create a robust foundation for understanding the concepts of microfinance, the triple bottom line, green microfinance, MSMEs, and the environmental consequences of MSME activities.

The initial step involved defining the scope and parameters of the literature search. Keywords related to green microfinance, MSMEs, environmental sustainability, and related topics were identified to guide the search process effectively. Boolean operators such as "AND" and "OR" were utilized to refine search queries and narrow down results to the most relevant and significant publications. The inclusion criteria for selecting literature encompassed scholarly articles and research papers published in peer-reviewed journals, conference proceedings, and authoritative books. The relevance and quality of each source were carefully evaluated to ensure the inclusion of high-impact and credible information in the review.

The search process involved systematically querying each database with the identified keywords and reviewing the abstracts of the retrieved articles. Subsequently, selected full-text articles were critically examined to extract pertinent information addressing the objectives of the study. The review was not limited to a specific period, allowing for the inclusion of both recent and seminal works.

Synthesizing the information obtained from diverse sources facilitated the creation of a comprehensive narrative on the state of knowledge regarding GM and its potential influence on MSMEs' environmental practices. The methodology adopted ensures that the study is grounded in a robust understanding of existing literature, providing a solid basis for insights, observations, and recommendations presented in subsequent sections of the article.

4. Discussion

4.1. Definition and Overview of Micro, Small and Medium Enterprises

MSMEs are viewed as independent enterprises with a modest market share that are run by their owners or co-owners (Afful-Koomson and Fonta, 2015; Kadarisman, 2019). Countries and institutions define MSMEs differently (Esubalew and Raghurama, 2017; Agyapong and Arthur, 2018; Verma, 2019). Thus, defining small firms globally is problematic. According to Samantha (2018), Peprah et al. (2020) and Nadyan et al. (2021) the criteria normally used to define MSMEs include; number of employees, the enterprises turnover, assets and market share. Esubalew and Raghurama (2020) posit that the heterogeneous definitions of MSMEs are attributed to the diversity of enterprises involved. What exactly an MSME is depends on who is doing the definition.

SMEs, according to the World Bank, have up to 300 employees or $15 million in revenue. The European Union (EU) classifies a firm with fewer than 10 people as micro, less than 50 as small, and less than 250 as medium (Gibson and Van der Vaart, 2008). The cut-off point for SMEs in Norway is 100 workers (Johansen, 2017). According to Ferraz and Pereira (2017), an SME in the US and Canada is any company with 5 to 500 employees and less than $50 million in annual gross revenues. A microbusiness has less than 5 workers. In South Africa MSMEs are termed as SMMEs which stands for small, medium, and micro enterprises. According to ILDP (2014) the amended National Small Business Act (2003 and 2004, NSB Act), SMME is a registered enterprise with less than 250 employees.

Ghana's government has standardized the concept of MSMEs for all institutions to enable uniformity in support systems and incentives, progress monitoring, and efficient research. According to the micro, small, and medium enterprises regulation (2021) by Ghana Enterprise Agency (GEA), formerly known as National Board for Small Scale Industry (NBSSI), a micro enterprise is defined as a business with fewer than 5 permanent employees and a turnover or assets of GH¢150,000. Small firms have 6-30 permanent employees, GH¢150,006-6,000,000 turnover or assets. Medium-sized businesses have 31 to 100 permanent employees. They have a turnover or asset range of GH¢6,000,006 to 18,000,000.

4.2 Environmental Consequences of Micro, Small and Medium Enterprises Activities

MSMEs work in close proximity to the environment (Joseph, 2020) and are therefore less attentive to environmental issues. Human activity exacerbates climate change (Liu et al., 2022). Sukumaran (2022) posits thatover consumption of natural resources for human needs is a trigger for natural disasters. Banholzer et al. (2014) and Sloggy et al. (2021) found a correlation between natural disasters and climate change that harm humans worldwide. Extreme precipitation, drought, earthquake, greater storms, heat waves, and sea level rise from melting polar ice caps threaten the ecology, MSMEs, the community, and coastal towns. It also has a deleterious impact on coral reefs and other marine species.

According to Singh et al. (2018), individual MSMEs' income-generating activities have a little influence on the environment, but the cumulative impact is substantial. MSMEs contribute to air pollution (AP), which is described by World Bank (2020) as the main environmental risk in Ghana. According to Darko et al. (2022), MSMEs contribute to both household and ambient air pollution (HAP and AAP).

Stanaway et al. (2018) found that ambient and residential air pollution kill 105 people per 100,000. About 16,000 Ghanaians die prematurely each year, 8,500 in cities and 7,600 in rural regions. AP accounts for 8% of all deaths. Ghana's AP is anticipated to cost 4.2 percent of GDP in 2017, or US$2.5 billion (World Bank, 2020).

Studies show that most Ghanaian water contamination is anthropogenic and MSMEs are significantly responsible (Darko et al., 2022). MSMEs' mining activities release cyanide, mercury, and other organic pollutants into waterways (Obiri-Yeboah et al., 2021). Many MSMEs prioritize profits over the environment (Joseph and Kulkarni, 2020; Nugroho et al., 2017).

Kyere-Boateng and Marek (2021) attribute Ghana's deforestation and forest degradation to agricultural expansion, illegal logging and mining, population growth, and inefficient laws. Charcoal burning, farming with weedicides, pesticides, and inorganic fertilizer, improper solid waste disposal into drainage, toxic liquid disposal, brick making, fish smoking, and sand winning harm the environment and communities (Arshad et al., 2020). Studies estimate yearly forest losses at 2.6% of agricultural GDP (Damnyag et al., 2011).

The aforementioned environmental issues have negative financial consequences for the very existence of the firms that generate the environmental imbalance. Similarly, the quality of life of MSMEs' clientele is also affected.

Environmental impacts also stretch beyond the community to the global environment through emission of greenhouse gases (Adamo et al., 2021, Shahidullah and Haque, 2015). As a result, GM is interconnected with other areas such as credit risk management, MSMEs' financial performance, food sufficiency, access to affordable energy, health, climate change adaptation and mitigation, rural development, and social mission.

4.3 Microfinance Institutions Influence on MSMEs to Go Green

One of the primary issues that MSMEs face is the inability to obtain financing from traditional banks. MSMEs face capital constraints, which prevents them from surviving and growing (Agyapong, 2020; Amoah and Amoah, 2018). Their main sources of funding include retained earnings, informal savings, credit associations, and money lenders. Among other things, this challenge inspired the microfinance concept, which provides financial assistance to MSMEs (Bali and Rathod, 2019, Bongomin, 2020).

Because MFIs serve primarily as financial intermediaries for MSMEs, there is a growing desire for them to incorporate environmental considerations into their operating strategies to reposition MSMEs to embrace and include environmental concerns into their goal setting and operations. (Allet and Hudon, 2015, Mia et al., 2018, Allet, 2014).

According to Sachs et al., (2019), MFIs that use green finance have an impact on the socially responsible conduct of other businesses while also improving their performance. Furthermore, GM holds MFIs accountable for the activities that they fund. GM institutions, as a result, tend to incorporate environmental issues into their objectives, which are reflected in their credit practices. Allet, (2014). notes that microcredit programs can assist MSMEs in thriving by promoting and achieving environmental, social, and financial benefits by channeling loans toward ecologically friendly actions.

As proposed in GM circles, a key link between microfinance and the environment is the impact that the MFI has on the environment through the activities of their clients, and how this may contribute to environmental degradation or restoration at various levels (Allet and Hudson, 2015; Allet, 2014; García-Pérez et al., 2018; Ashraf et al., 2022).

Green MFls also investigate and develop procedures and strategies for mitigating MSMEs' environmental deprivation risks, promoting more resilient investments, risk transfer via microinsurance, and supporting MSMEs (Huybrechs et al., 2015). MFIs offer microcredit in conjunction with technical assistance and environmental awareness. This decreases environmental imbalances and their effects, which can have a detrimental influence on an MSMEs' loan repayment capacity and, as a result, raise the risk of default for MFIs (Kapitsa, 2020).

Microfinance's micro enterprise investment training helps clients manage their businesses and reduce transaction risks (Irene et al., 2015) and grow sustainably (Putri et al., 2020). Nugroho et al. (2017) contend that MFIs help MSMEs adopt green technologies, eco-friendly packaging and designs, energy-efficient equipment, solar energy, organic farming, and other eco-friendly practices, thus reducing their environmental impact.

In South-East Asia, Mia et al. (2020) examined how MFIs contribute to environmental sustainability, with a specific focus on reducing greenhouse gas (GHG) emissions in agriculture. The study’s findings showed that green MFIs have a good impact on environmental greening initiatives. Rouf (2012) contrasted Grameen Bank's Bangladeshi lending system with Alterna Savings' Canadian program and their effects on Toronto's economy and environment. The findings indicate that microfinance has a favorable influence on environmental performance in both Bangladesh and Canada.

In rural southern Bangladesh, Shahidullah and Hague (2014) investigated six green-microcredit-based microenterprises' environmental impacts. The survey found that most of these businesses were sustainable, compliant with environmental laws, and profitable enough to survive. Case study and participatory research were used by Shahidullah and Hague (2015) to study a microfinance organization headquartered in two different areas in Bangladesh. The study evaluated green and traditional microfinance-assisted firms' environmental challenges and calculates their greenhouse gas (GHG) emissions. According to the data, microenterprises that receive loans from MFIs and apply green procedures emit fewer greenhouse gases than those that use traditional strategies.

Perez et al. (2020) used MIX Market sustainability data to examine microfinance institutions' operations and sustainability efforts. The survey covered Europe, Asia, Africa, America, Oceania, and the Caribbean. The researchers analyzed the data using content analysis. Findings from the study reveal that the impact of microfinance on environmental performance is different in the various countries considered in the study. Finally, Uddin et al. (2021) examined the profitability of Bangladeshi MFIs from green microfinancing using data from 365 stakeholders, clients, and officials. MFI profitability was found to be positively correlated with green microfinance. The review identified several empirical studies in the field of microfinance that support the claim that GM has the potential to encourage MSMEs to adopt environmentally friendly operations.

4.4 Influential Factors on Environmental Consciousness in MSMEs

A critical analysis of the available literature on GM was undertaken in order to assess whether microfinance can incorporate environmental dimension in their objective setting and succeed to reorient MSMEs to be more environmentally friendly. The review of literature has established the contribution of MFIs to mitigate the effect of anthropogenic environmental issues. The literature evaluation observed that microfinance had varying impacts on environmental performance in different countries. (Perez et al. 2020).

The analysis of the literature indicates that MFIs of greater scale and those that are registered as banks exhibit superior performance in terms of environmental policy implementation and environmental risk assessment. It was revealed that MFIs' financial and non-financial services can influence MSMEs to go green. The main source of financing for MSMEs is MFI, therefore including environmental issues in lending policies will encourage greening given attractive interest rates and larger loan amounts.

Green MFls investigate and develop procedures and strategies for lowering MSMEs' environmental deprivation risk, fostering more resilient investments, risk transfer via microinsurance, and supporting MSMEs' activities. The literature review revealed that there are other factors that affect the environmental consciousness of small businesses. The other germane factors that were noted in a study conducted by Agarwal et al. (2020) included i) owner/manager commitment to sustainability ii) Legislation iii) economic benefits, iv) stakeholder pressure, v) firm performance Vi) demand for eco-friendly products and vii) competition.

5. Conclusion

An analytical assessment was conducted to examine the capacity of microfinance institutions to incentivize MSMEs to adopt environmentally friendly practices in Ghana and globally. The literature analysis revealed that MFIs can use targeted adaptation strategies to manage the environmental issues arising from small enterprises in Sub-Saharan Africa. A thorough evaluation of GM shows that when MFIs integrate environmental awareness guidelines into their operations, MSMEs adopt and implement environmentally friendly activities.

The review highlights a lack of research conducted in Sub-Saharan Africa regarding the topic area, indicating the necessity to address this gap. The disregard for environmental issues stemming from the unregulated activities of MSMES has significant consequences for both the environment and the communities that accommodate these small firms. A general suggestion is to promote the development of practical operational policies and strategies by MFIs in Ghana, with the aim of encouraging MSMEs to adopt environmentally friendly practices in order to protect the environment.

The government must establish a dedicated fund to provide financial support for MSMEs' green initiatives. MFIs should have low-interest access to this money to lend to their clients.

To encourage MSMEs to adopt green practices, government initiatives like the National Entrepreneurship and Innovation Programme (NEIP) and Ghana Enterprise Agency (GEA) SME grant, which provide financial assistance to selected entrepreneurs, should require a thorough environmental impact assessment as a prerequisite for qualification. This will inspire entrepreneurs to devise inventive methods to mitigate their environmental effect. Furthermore, it is essential to conduct regular monitoring following the disbursement of the money to verify that they are being utilized for their intended purpose.

Since MFIs influence MSMEs' environmental performance differently across nations, the potential of MFIs to influence MSMEs in a specific area to adopt environmentally friendly practices needs to be examined. MFIs have a vested interest in encouraging MSMEs to implement environmentally friendly practices since this would reduce the credit risk associated with the management of environmental risks caused by MSMEs. The contention posited here is that environmental hazards have the potential to diminish the financial stability of MSMEs. The depletion of natural resources may render a business unsustainable, leading to potential reputational issues and adverse impacts on its operations. Pollution can cause health issues and fines for environmental violations. MFIs must manage their clients’ environmental hazards to reduce credit risk.

It is worthy to note that MSMEs' decisions to adopt sustainable practices are influenced by many other factors, including the owner’s/manager's orientation, regulation, the cost of adopting environmentally friendly practices, stakeholder pressure, competition, firm performance, and demand for eco-friendly products. Therefore, in order to effectively implement green microfinance, these factors must be considered.

5.1 Policy Implications

The study is expected to assist policymakers in formulating policies for MSMEs to incorporate environmental considerations into their financial activities utilized for earning a livelihood through microfinancing. The implementation of such policies would provide benefits not just for the country as a whole, but also for MSMEs, as it would strengthen their sustainability by mitigating self-imposed risk factors. MFIs would equally benefit from such policies since the credit extended to MSMEs would be invested in sustainable businesses, thereby reducing loan defaults. Secondly, this paper can assist the government in establishing a specialized green fund that microfinance institutions can utilize at a preferential interest rate to subsequently lend to MSMEs for environmentally sustainable initiatives. The significance of green microfinance underscores the necessity for a policy framework to facilitate the effective implementation of green microfinance practices in Ghana.

5.2 Limitations of the Study and Future Directions of Research

The study has certain limitations as it is exclusively theoretical and lacks empirical investigation. This study can be confirmed in the future by gathering quantitative data directly from green MFIs and MSMEs. Further analysis can be done to examine the role of green microfinance institutions in facilitating socio-ecological development.

---

Funding: The present study did not receive any external financial support.

Conflicts of Interest: The authors declare that there are no conflicts of interest regarding the publication of this paper.

---

Disclaimer/Publisher’s Note: The views, statements, opinions, data and information presented in all publications belong exclusively to the respective Author/s and Contributor/s, and not to Sprint Investify, the journal, and/or the editorial team. Hence, the publisher and editors disclaim responsibility for any harm and/or injury to individuals or property arising from the ideas, methodologies, propositions, instructions, or products mentioned in this content.

References

- Abid, L. and Kacem, S., 2018. Why are we going to green microfinance in Tunisia? Environmental Economics, 9, p.1.

- Abor, J., and Quartey, P., 2010. Issues in SME development in Ghana and South Africa. International research journal of finance and economics,39(6), pp.215-228.

- Adamo, N., Al-Ansari, N. and Sissakian, V., 2021. Review of climate change impacts on human environment: past, present and future projections. Engineering, 13, pp.605-630.

- Afful-Koomson, T., and Fonta, W., 2015. Economic and financial analyses of small and medium food crops agro-processing firms in Ghana: United Nations University Institute for Natural Resource.

- Agarwal, S., AgrawaL, V. and Dixit, J. K., 2020. Green manufacturing: A MCDM approach. Materials today: proceedings, 26, pp.2869-2874.

- Agyapong, D., 2020. Review of entrepreneurship, micro, small and medium enterprise financing schemes in Ghana. Enterprising Africa. Routledge.

- Agyapong, D., and Arthur, K. N. A., 2018. Sustainable Business Practices Among MSMEs: Evidence from four Metropolitan Areas in Ghana. Paper presented at the ECIE 2018 13th European Conference on Innovation and Entrepreneurship.

- AlleT, M. and Hudon, M., 2015. Green microfinance: Characteristics of microfinance institutions involved in environmental management. Journal of Business Ethics, 126, pp.395-414.

- Allet, M., 2012. Mitigating environmental risks in small-scale activities: what role for microfinance? A case study from El Salvador. ULB--Universite Libre de Bruxelles.

- Allet, M., 2014. Why do microfinance institutions go green? An exploratory study. Journal of Business Ethics, 122, pp.405-424.

- Amoah, S. K. and Amoah, A. K., 2018. The role of small and medium enterprises (SMEs) to employment in Ghana. International Journal of Business and Economics Research, 7, pp.151-157.

- Arshad, Z., Robaina, M., Shahbaz, M. and Veloso, A. B., 2020. The effects of deforestation and urbanization on sustainable growth in Asian countries. Environmental Science and Pollution Research, 27, pp.10065-10086.

- Ashraf, D., Rizwan, M. S. and L’Huillier, B., 2022. Environmental, social, and governance integration: The case of microfinance institutions. Accounting and Finance, 62, 837-891.

- Atahau, A. D. R., Sakti, I. M., Huruta, A. D. and Kim, M.-S., 2021. Gender and renewable energy integration: The mediating role of green-microfinance. Journal of Cleaner Production, 318, 128536.

- AyyagarI, M., Beck, T. and Demirguc-Kunt, A., 2007. Small and medium enterprises across the globe. Small business economics, 29, 415-434.

- Bali, M. and Rathod, P. P. 2019. “Microfinance Bank, A panacea for SME’s sickness” A Case of Gulbarga District, Karnataka.

- Banholzer, S., Kossin, J. and Donner, S., 2014. The impact of climate change on natural disasters. Reducing disaster: Early warning systems for climate change, pp.21-49.

- Bastiaensen, J., Merlet, P., Craps, M., DE Herdt, T., Flores, S., Huybrechs, F., Mendoza, R., Steel, G. and Van Hecken, G., 2015. Making sense of territorial pathways to rural development: a proposal for a normative and analytical framework.

- Berguiga, I., Adair, P. and Berguiga, I., 2019, Funding MSMEs in North Africa and Microfinance: the Issue of Demand and Supply Mismatch. Economic Research Forum (ERF).

- Blackman, A., 2000. Informal sector pollution control: what policy options do we have? World Development, 28, pp.2067-2082.

- Bongomin, G. O. C., Woldie, A. and Wakibi, A., 2020. Microfinance accessibility, social cohesion and survival of women MSMEs in post-war communities in sub-Saharan Africa: Lessons from Northern Uganda. Journal of Small Business and Enterprise Development, 27, pp.749-774.

- Boon, E. K. and Yeboah, E., 2018. Indigenous social security systems and government policies: Impacts on the development of micro, small and medium scale enterprises in Ghana. Indigenous social security systems in Southern and West Africa, pp.125-146.

- Brahmbhatt, M., Haddaoui, C., and Page, J., 2017. Green industrialisation and entrepreneurship in Africa. Contributing paper for African Economic Outlook, pp.1-60.

- Chetama, J. C., Dzanja, J., Gondwe, S., and Maliro, D., 2016. The Role of Microfinance on Growth of Small-Scale Agribusinesses in Malawi: A Case of Lilongwe District. Journal of Agricultural Science, 8(6), pp.84-93.

- Chowdhury, A. and Tadjoeddin, Z., 2023. Financing green transformation in developing countries. Canadian Journal of Development Studies/Revue canadienne d'études du développement, 44, pp.430-453.

- Cosgrove, S., 2021. Financial services for the poor. Understanding Global Poverty. Routledge.

- Damnyag, L., Tyynelä, T., Appiah, M., Saastamoinen, O. and Pappinen, A., 2011. Economic cost of deforestation in semi-deciduous forests—A case of two forest districts in Ghana. Ecological Economics, 70, pp.2503-2510.

- Darko, G., Obiri-Yeboah, S., TakyI, S. A., Amponsah, O., Borquaye, L. S., Amponsah, L. O. and Fosu-Mensah, B. Y., 2022. Urbanizing with or without nature: Pollution effects of human activities on water quality of major rivers that drain the Kumasi Metropolis of Ghana. Environmental Monitoring and Assessment, 194, p.38.

- Egbide, B.-C., 2020. Rotating and savings credit association (ROSCAs): A veritable tool for enhancing the performance of micro and small enterprises in Nigeria. Asian Economic and Financial Review, 10, pp.189-199.

- Esubalew, A. A., and Raghurama, A., 2017. Revisiting the global definitions of MSMEs: parametric and standardization issues. Asian Journal of Research in Business Economics and Management, 7(8), pp.429-440.

- Esubalew, A. A., and Raghurama, A., 2020. The mediating effect of entrepreneurs’ competency on the relationship between Bank finance and performance of micro, small, and medium enterprises (MSMEs). European Research on Management and Business Economics, 26(2), pp.87-95.

- Ferraz, D. E., and Pereira, E. T., 2017. The importance of small knowledge intensive firms in European countries. International Entrepreneurship Review, 3(1), pp.85-108.

- Forcella, D. and Hudon, M., 2016. Green microfinance in Europe. Journal of Business Ethics, 135, pp.445-459.

- Gakpo, M. D. Y., Wujangi, M., Kwakye, M., and Asante, V. G., 2021. The impact of MICROFINANCING on poverty alleviation and small businesses in Ghana. International Journal of Social Sciences and Humanity Studies, 13(1), pp.1-28.

- García-Pérez, I., Fernández-izquierdo, M. Á. and Muñoz-Torres, M. J., 2020. Microfinance institutions fostering sustainable development by region. Sustainability, 12, p.2682.

- García-Pérez, I., Muñoz-Torres, M. J. and Fernández-Izquierdo, M. Á., 2018. Microfinance institutions fostering sustainable development. Sustainable Development, 26, pp.606-619.

- Gibson, T., and Van der Vaart, H., 2008. Defining SMEs: A less imperfect way of defining small and medium enterprises in developing countries.

- Hindle, T., 2008. Guide to management ideas and gurus, John Wiley and Sons.

- Huybrechs, F., Bastiaensen, J. and Van Hecken, G., 2019. Exploring the potential contribution of green microfinance in transformations to sustainability. Current opinion in environmental sustainability, 41, pp.85-92.

- Irene, R., Charles, L. and Japhet, K., 2015. Effects of microfinance services on the performance of small and medium enterprises in Kenya. African Journal of Business Management, 9, pp.206-211.

- Johansen, S., 2017. Norwegian Regional Development and the Role of SMEs. In Regional Economic Growth, SMEs and the Wider Europe (pp. 149-160): Routledge.

- Joseph, C., 2020. Problems and resolutions in GHG impact assessment. Impact Assessment and Project Appraisal, 38(1), pp.83-86.

- Joseph, S. and Kulkarni, A. V., 2020. Creating sustainable contribution to the environment: case studies from MSMEs in Pune. International Journal of Social Ecology and Sustainable Development (IJSESD), 11, pp.1-14.

- Kadarisman, M., 2019. The influence of government and MUI mediations towards marketing strategy of Warteg and its impact on developing MSMEs in Jakarta, Indonesia. Cogent Business and Management, 6(1), 1629096.

- Kapitsa, L., 2020. Climate Change and Micro, Small and Medium Enterprises. Вестник МГИМО Университета, pp.216-231.

- Khan, A., Ahmad, A., and Shireen, S., 2021. Ownership and performance of microfinance institutions: Empirical evidences from India. Cogent Economics and Finance, 9(1), 1930653.

- Kyereboah‐Coleman, A. and Osei, K. A., 2008. Outreach and profitability of microfinance institutions: the role of governance. Journal of Economic Studies, 35, pp.236-248.

- Kyere-Boateng, R. and Marek, M. V., 2021. Analysis of the social-ecological causes of deforestation and forest degradation in Ghana: Application of the DPSIR framework. Forests, 12, 409.

- Liedholm, C., and Mead, D., 2005. Small enterprises and economic development: the dynamics of micro and small enterprises, Routledge.

- Loan, P. T., 2018. Crowdfunding–A new form of Capital mobilization for Small and Medium sized enterprises (SMES) in Vietnam. Paper presented at the 5th IBSM International Conference on Business, Management and Accounting, pp.19-21.

- Madrid‐Guijarro, A., Garcia, D. and Van Auken, H., 2009. Barriers to innovation among Spanish manufacturing SMEs. Journal of small business management, 47, pp.465-488.

- Majid, I. A., and Koe, W.-L., 2012. Sustainable entrepreneurship (SE): A revised model based on triple bottom line (TBL). International Journal of Academic Research in Business and SocialSciences, 2(6), 293.

- Mia, M. A., Zhang, M., Zhang, C. and Kim, Y., 2018. Are microfinance institutions in South-East Asia pursuing objectives of greening the environment?. Journal of the Asia Pacific Economy, 23, pp.229-245.

- Moyo, Z., 2020. Financial sustainability, liquidity and outreach of deposit-taking microfinance institutions: evidence from low-income Sub-Saharan Africa.

- Nadyan, A. F., Selvia, E., and Fauzan, S., 2021. The Survival Strategies of Micro, Small and Medium Enterprises in The New Normal Era. Dinamika Ekonomi, 12(2), pp.142-149.

- Nghiem, H. S., 2005. Analysing the effectiveness of microfinance in vietnam: A conceptual framework. Unpublished manuscript, School of Economics, The University of Queensland.

- Nugroho, L., Utami, W., Akbar, T. and Arafah, W., 2017. The challenges of microfinance institutions in empowering micro and small entrepreneur to implementing green activity. International Journal of Energy Economics and Policy, 7, pp.66-73.

- Obaidullah, M., 2008. Introduction to Islamic microfinance. Mohammed Obaidullah, IBF Net Limited.

- Obiri-Yeboah, A., NyantakyI, E. K., Mohammed, A. R., Yeboah, S. I. I. K., Domfeh, M. K. and Abokyi, E., 2021. Assessing potential health effect of lead and mercury and the impact of illegal mining activities in the Bonsa river, Tarkwa Nsuaem, Ghana. Scientific African, 13, e00876.

- Ossebaard, H. C. and Lachman, P., 2021. Climate change, environmental sustainability and health care quality. International Journal for Quality in Health Care, 33, mzaa036.

- Pandya, V. M., 2012. Comparative analysis of development of SMEs in developed and developing countries. 2012 International Conference on Business and Management, pp.1-20.

- Pearce, D., 2011. Financial inclusion in the Middle East and North Africa: Analysis and roadmap recommendations. World Bank policy research working paper.

- Peprah, C., Abdulai, I., and Agyemang-Duah, W., 2020. Compliance with income tax administration among micro, small and medium enterprises in Ghana. Cogent Economics and Finance, 8(1), 1782074.

- Putri, V., Ridloah, S. and Wijaya, A., 2020. Strategy for increasing green economic performance of small and medium enterprises based on green business management. IOP Conference Series: Earth and Environmental Science 2020. IOP Publishing, 012063.

- Robert, S. and Schleyer-Lindenmann, A., 2021. How ready are we to cope with climate change? Extent of adaptation to sea level rise and coastal risks in local planning documents of southern France. Land Use Policy, 104, 105354.

- Rouf, A.K., 2012. Green microfinance promoting green enterprise development. Humanomics, 28, pp.148-161.

- Sachs, J. D., Woo, W. T., Yoshino, N. and Taghizadeh-Hesary, F., 2019. Importance of green finance for achieving sustainable development goals and energy security. Handbook of green finance, 3, pp.1-10.

- Samantha, G., 2018. The impact of natural disasters on micro, small and medium enterprises (MSMEs): A case study on 2016 flood event in Western Sri Lanka. Procedia engineering, 212, pp.744-751.

- Satterthwaite, D., Archer, D., Colenbrander, S., Dodman, D., Hardoy, J. and Patel, S., 2018. Responding to climate change in cities and in their informal settlements and economies. International Institute for Environment and Development, Edmonton, Canada, 61.

- Shahidullah, A. and Haque, C. E., 2014. Environmental orientation of small enterprises: can microcredit-assisted microenterprises be “green”? Sustainability, 6, pp.3232-3251.

- Shahidullah, A. and Haque, E. C., 2015. Green microfinance strategy for entrepreneurial transformation: validating a pattern towards sustainability. Enterprise development and microfinance, 26, pp.325-342.

- Shi, A., and Michelitsch, R., 2013. Assessing private sector contributions to job creation: IFC open source study. International Finance Corporation.

- Shou, Y., Shao, J., Lai, K.-h., Kang, M., and Park, Y., 2019. The impact of sustainability and operations orientations on sustainable supply management and the triple bottom line. Journal of Cleaner Production, 240, 118280.

- Singh, D., Khamba, J. and Nanda, T., 2018. Problems and prospects of Indian MSMEs: a literature review. International Journal of Business Excellence, 15, pp.129-188.

- Singh, S. K., Chen, J., Del Giudice, M. and El-Kassar, A.-N., 2019. Environmental ethics, environmental performance, and competitive advantage: Role of environmental training. Technological Forecasting and Social Change, 146, pp.203-211.

- Sloggy, M. R., Suter, J. F., Rad, M. R., Manning, D. T. and Goemans, C., 2021. Changing climate, changing minds? The effects of natural disasters on public perceptions of climate change. Climatic Change, 168, pp.1-26.

- Stanaway, J. D., Afshin, A., Gakidou, E., Lim, S. S., Abate, D., Abate, K. H., Abbafati, C., Abbasi, N., Abbastabar, H. and Abd-Allah, F., 2018. Global, regional, and national comparative risk assessment of 84 behavioural, environmental and occupational, and metabolic risks or clusters of risks for 195 countries and territories, 1990–2017: a systematic analysis for the Global Burden of Disease Study 2017. The Lancet, 392, pp.1923-1994.

- Sukumaran, K., 2022. Impact of Human Activities Inducing and Triggering of Natural Disasters. A System Engineering Approach to Disaster Resilience: Select Proceedings of VCDRR 2021. 17-31. Springer.

- Verma, T. L., 2019. Role of micro, small and medium enterprises (MSMES) in achieving sustainable development goals. Small And Medium Enterprises (MSMEs) in Achieving Sustainable Development Goals (April 1, 2019).

- World Bank 2020, Ghana, country environmental analysis. The World Bank Group, 1818 H Street NW, Washington, DC 20433, USA.

- Yadav, N., Gupta, K., Rani, L. and Rawat, D., 2018. Drivers of sustainability practices and SMEs: A systematic literature review. European Journal of Sustainable Development, 7, pp.531-531.

- Zhang, Q. and Posso, A., 2019. Thinking inside the box: A closer look at financial inclusion and household income. The Journal of Development Studies, 55, pp.1616-1631.

Article Rights and License

© 2024 The Authors. Published by Sprint Investify. ISSN 2359-7712. This article is licensed under a Creative Commons Attribution 4.0 International License.