Keywordsbanking credit scoring e-commerce e-entrepreneurs forms of capital microfinance online entrepreneurship Small Business Enterprise (SME) social capital

JEL Classification G2, H81, L81

Acknowledgement:

The Author would like to thank the reviewers for the helpful comments on the manuscript. Also, the Author acknowledges Indonesia Banking School Internal Grant for funding this research.

Full Article

1. Introduction

The role of microfinance to support micro and small business development and growth in emerging nations has been widely known (Malhotra, 2018; Kasemsap, 2018). Microcredit programs have been launched by the government in order to support poverty alleviation strategy over the last three decades (Tahmasebi and Azkaribesayeh, 2020). Studies have been conducted and proved the impact of microcredit programs onthe economy and the wellbeing of society. As the internet has been increasing in popularity, e-entrepreneurs emerged as an important key of economic development (La & To, 2020).

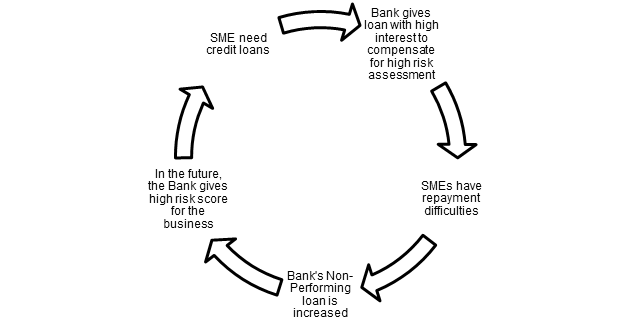

Nevertheless, a study conducted by the Centre for the Study of Financial Innovation states that the microfinance industry is still facing two main challenges. First, a key challenge is to reduce credit risk, which is currently getting worse by the over-indebtedness. Secondly, another challenge is the perception that the microfinance industry has lost sight of its social purpose (Serrano-Cinca, Gutiérrez-Nieto, and Reyes, 2013). These two problems are interrelated and becoming a circular link. The low repayment problem of microfinance clients (micro and small and medium enterprises / SME) have made it difficult for the financial institutions to give an optimum low rate for the microfinance due to the risk involved. The interest rate then becomes very high for SME business lending. When the interest rate is high, the businesses have difficulties in repaying the loan. When a business has a repayment problem, the bank/microfinance institution will give a higher risk score for the same business in the future, which results in a higher interest rate. Finally, when the MFI commands a high-interest rate, the industry is perceived to have lost sight of its social purposes in helping SME business (Figure 1).

Figure 1. Vicious Circle of Microfinance Lending

Source: own compilation

Initially, traditional microfinance has presented a solution to the repayment problem for the community lending or group lending model. In this model, the community members aid in monitoring the repayment process. Nevertheless, this model is mostly found in rural areas where the social bonding remains intact while the effectiveness evidence in the city areas, where most small businesses are now thriving is still rarely found.

This study argues that one of the possible ways to break this vicious chain (Diagram 1) lays in how good microfinance asses the loan in their credit risk evaluation. Credit risk evaluation is the process through which a bank assesses the creditworthiness of prospective loan as the base for measuring its credit risk (Ibtissem and Bouri, 2013). By employing an innovative measure of credit risk assessment, the creditworthiness of a small business can be measured fairly and thus might provide a reasonable interest rate which not leading towards repayment problems.

The method of assessment of a loan is usually subjective, with 5Cs framework as a general approach. In the 5Cs framework, evaluation is based on Character, Capacity, Condition, Capital, and Collateral. The five aspects are calculated for a credit scoring of a loan. However, only a few microfinance institutions use scoring as a statistic method to approach credit evaluation (Dellien and Schreiner, 2005). One of the significant challenges facing microfinance institutions in their quest to provide credit facilities is the availability of sufficient information to assess a loan. Most of clients have scarce financial information (Serrano-Cinca et al., 2013), which makes the assessment difficult. When the assessment is difficult, the propensity to give a higher rate to manage the risk increases. Hence there is a need for a simple way to assess a loan based on available data.

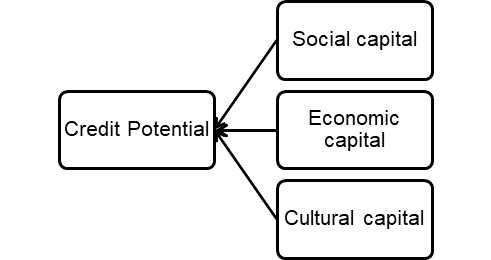

One of the journeys to find an alternative theory to assess a loan application is by incorporating a multidisciplinary theory from other disciplines. The research is interested in investigating a classic sociological theory of Bourdieu (1986), which explained three forms of capital. The three forms of capital are explained as economic capital, cultural capital, and social capital. The three forms of capital have been used in various contexts, including entrepreneurship.

Although the three forms of capital represent a well-known concept, it is still relatively unexplored in terms of the usability for credit application evaluation. In addition, it also rarely tested in terms of the small business industry, especially online business context. The study tries to find an alternative solution for assessing the credit potential and experience of a loan applicant based on a set of simple questions or observations based on Bourdieu's three forms of capital. Hence, the objectives of this research are to confirm the three forms of capital contribution to Credit Potential.

The study is expected to contribute to the academic literature by extending sociological theories to be used in assessing a small business loan. Specifically, it aims to contribute to the academic literature by finding an alternative measurement of the cultural and social capital with a simple set of measures. The previous literature found that religiosity and social media activity might be a promising factor for the measure. Therefore, this study decides to incorporate religiosity factor into the cultural capital variable and social media activity into the social capital variable. Both factors will be the novelty of this study, which contributes to theoretical findings. On the other hand, the study is also expected to contribute to the practical situations by providing insight into building an alternative evaluation method of credit evaluation using a simple alternative measure.

The presentation of the paper starts with the background issue and literature review. The next section explains the methodology and results of the study. Lastly, the conclusion and discussion section will describe the contribution and future study suggestions. To limit the scope of the research, this study decides to focus on small business owners operating in e-commerce environment in the Indonesian market (e-entrepreneurs). Thus, the measurement will also incorporate elements to cater to the digital environment.

2. Literature Review

The study will take root from the theory of human capital from Bourdieu (1986) and will try to add to existing work from various sources to form an unconventional way to measure the credibility of a small business in proposing a loan. The theory of the three forms of capital argues that one’s social life can take form as a multi-dimensional status search in which individuals capitalize their economic, social, and cultural capital resources in order to compete for a certain level of status. These types of capitals are termed "symbolic capital" (Holt, 1998). There are three kinds of capital that interrelate to each other (Bourdieu, 1986). First is the Economic Capital, which is the reproduction of certain forms of capital and sometimes linked to the familial background. Bourdieu has stated that “economic capital is at the root of all other types of capital” (1986:252). Cultural capital includes of a set of socially distinctive tastes, skills, knowledge, and practices that are embodied within individuals as implicit practical knowledge, skills, and dispositions. It is first introduced within a family and later reinforced in one’s life once it enters the educational system. Additionally, social capital is the capital formed by socializing activities and based on social similarity, shared affiliations, and activities. A social connection that involves a degree of mutual interdependence and interconnected activities can enhance social influence to form a close social relationship.

In addition to the classic three forms of capital theory, there are recent developments in using behavioral data as alternative data for loan assessment. In this study, we incorporate the use of new factors into hypothesis development. One of the additions to social capital is social media activity. Social media has continued to gain widespread acceptance. For example, in the year 2012, Facebook had 1 billion users worldwide while in the same year, Twitter had an estimated 517 million users (Dewing, 2012). The social networks provide social media data with the use of networking platform using internet-based and mobile services data. The users of these services participate in online exchanges, join online communities, or contribute user-created content (Dewing, 2012). Several factors have contributed to this rapid growth and embracement of social media services. The growth has contributed by the increased broadband availability, improvement of software tools, development of more powerful computers and mobile services (Dewing, 2012, Mustafa and Hamzah, 2011). An interesting study by Masyutin (2015) has investigated the use of social data from Russia's most popular social network and discriminate between solvent and delinquent debtors of credit organizations. The social network data was found to better predict fraudulent cases rather than ordinary defaults, thus ideal to use in enriching the classical application scorecards. Another study on the use of social media data is from the work of Wei, Yildirim, Bulte, and Dellarocas (2015) which use network data information and relate it with credit scoring. The study was collecting information from a consumer's network where people with an above average chance of interacting with others with similar creditworthiness creating social scoring. The interaction provides a larger chance to the population with limited personal financial history to be offered increased credit due to social scoring.

H1: Social Capital has a significant and positive effect to Credit Potential.

The economic capital consists of revenues, high turnovers, and established positions Difference between big and small business exist, due to the length of period time the company exists. The older companies have been in operation, the higher the economic capital and business reputation. While smaller companies hold less economic capital and lack an established position than a long-term business reputation (Vigerland & Borg, 2017). In addition, symbolic capital is also essential and in line with Bourdieu's conceptual framework. To extend the symbolic economic capital, the study tries to incorporate online badges and feedback reviews as an economic capital measure.

H2: Economic Capital has a significant and positive effect to Credit Potential.

Most of the credit application evaluation measure of cultural capital is only based on formal education. The current study wants to extend the understanding and incorporate the view of religiosity as a possible factor to measure the cultural capital of a loan applicant. The argument is based on several literatures that support this view concerning an economic activity.

Hilary and Hui (2009) argue that religious individuals' propensity for risk aversion will influence their firms' behavior. They explained that individual religious values shape corporate culture; members of a corporation have to conform to their firm's dominant value. Other research also showed that religiosity exerts a positive influence on business ethics (Weaver and Agle, 2002) as more religious managers are likely to be more ethical in their business activities. Lastly, Chen, Huang, Lobo, and Wang (2016) study found that, indeed, stronger religiosity related to favorable terms in loan contracts.

H3: Cultural Capital has a significant and positive effect to Credit Potential.

The model and hypotheses can be depicted as follows in Figure 2.

Figure 2. Model of Three Forms of Capital

Source: own compilation

3. Methodology

In order to achieve the objective of this paper, more specifically to explore the alternative evaluation of microloan lenders, the study initially decided to use qualitative study due to its explorative and flexibility nature. However, there is a difficulty in finding the respondents and the limit of time has forced the researcher to alter the plan towards a more practical quantitative study. Hence, the design of the research is a cross-sectional quantitative study with a survey questionnaire.

The questionnaire is conducted with a sample of e-entrepreneurs with two criteria. First, the owner of a business operating via e-commerce channel as one of their primary channels of distribution. The study is not limited only to full online channel only, but it is also possible for an entrepreneur who has physical stores and traditional brick and mortar business in parallel with their online channel. The second criterion is the business turnover. The entrepreneur should have a daily transaction of the business of more than 50 transactions per day. The definition of a micro business in Indonesia is a business with a turnover of USD 22,222 per month or approximately USD 750 per day. Regardless of the volume and value of the total item sold, we assume the criteria of more than 50 transactions daily can represent the micro and small business profile. There is no limitation for age and geographical region. However, it is for Indonesian respondents only. As the questionnaire is distributed online, it is expected that respondents come from diverse age groups and regions. The number of targeted respondents will follow rules of thumb from Hair, Hult, Ringle, and Sarstedt (2016), which aimed at ten times the largest number of indicators, which equals to 90 respondents.

The data process is using PLS-SEM. The analysis procedure in this study follows the systematic guidelines from Hair et al. (2016). The analysis of PLS-SEM result is done in three stages. The first stage is the measurement model analysis (Outer Model). The outer model analysis is done to ensure that the measurement used is feasible for measurement (valid and reliable). The outer analysis of this model specifies the relationship between the latent variables and the indicators. The statistic tests performed on outer models are focused on convergent validity and discriminant validity, reflected in composite reliability (expected value > 0.7 for high reliability), average variance extracted (AVE) (expected AVE value> 0.5) and Cronbach alpha (the expected value is> 0.6 for all constructs).

The second analysis is the analysis of structural or inner model. Inner model analysis / structural model analysis is carried out to ensure that structural models are built robust and accurate. Inner model evaluation, according to Hair et al. (2016), can be seen from several indicators, namely, coefficient of determination (R2) and Predictive Relevance (Q2).

The last analysis is confirming the hypothesis testing by looking at the probability value of T-statistics. The probability value expected is the P-value value, with a 5% alpha is less than 0.05. The T-table value for alpha 5% is 1.96. So, the criteria for acceptance of hypothesis according to Hair et al. (2016) will be significant if the value of T-statistics is higher than 1.96. However, in some cases, a 10% alpha can also be accepted with T-statistics greater than 1.65.

The study investigates the three aspects of Human Capital, namely: Social Capital, Economic Capital, and Cultural Capital and tests these independent variables against Credit Experience and Potential of e-entrepreneurs. The questions are using a 1 to 5 Likert scale, except for a few questions which scale is adjusted. The measurement of each variable is derived conceptually from several literatures. The Social Capital is measured by three dimensions, the active community involvement, the role of the family, and social media activity. The measures are adapted from Chen, Zhou, and Wang (2016) on the context of online peer to peer lending. The Economic Capital measures physical assets owned to run the business, growth, and prospect of business and feedback and recommendation from the customers. The study refers to Karlan and Zinman (2011) and also Sosha (2014) for the Economic Capital variable. The cultural capital incorporates dimensions such as education level, business experience, and religiosity. The measurement is referenced from supporting studies in the literature (Chen et al. 2016).

All three forms of capital are tested against Credit Experience and Potential. This construct will measure positively if the respondents have had a loan approved in the past, including the status of the loan and whether they are interested in proposing another loan in the future. Some of the measures are adapted from (Fisher, Maritz, and Lobo, 2014). The literature is only as guidance to explore new measurements, and there are no exact measures derived from each article. The aim is not only to test previous studies but also to give alternative measurements besides the ones that have already existed in the literature.

4. Results

4.1. Demographic Profile

The unit of analysis of the research are e-entrepreneurs with a minimum of 50 business transactions per day. This study manages to collect 100 filled surveys. From the result, we can describe the demographic profile of respondents in terms of gender, age, location, and monthly spending. In addition, this study has also identified the education background of the respondents. More than half (59%) of respondents are male. Predominantly young adults, within the age range of respondents, is 20-25 years old (47%), 26-29 years old (29%) and 30-35 years old (15%). Education background of the entrepreneurs is mostly high school graduate (50%) and undergraduate (33%). Around 33% have the average spending per month USD 1000 to 2000 and 20% spend more than the range mentioned. Although they serve business nationally, the respondents are mostly based on Java island (the most populous island in Indonesia).

4.2. Analysis of Outer Model

The analysis of the model starts with the measurement model or outer model analysis. This study found that most of the indicators have passed the criteria and therefore, can be further processed to measure the variable in the structural model (inner model). The value of convergent validity is the value of loading factor on the latent variable with its indicators. The expected value is > 0.5. From the initial 32 indicators, 22 indicators surpassed the criteria. The processed data found that the loading value on the intended construct is greater than the value of loading with other constructs, which means the criterion is fulfilled for discriminant validity. Data found that all of the variable composite reliability is above 0.7, which means all variables have high reliability. In this case, only economic capital that has AVE value> 0.5. The reliability test reinforced with Cronbach Alpha, and the result value is > 0.5 for all constructs. This result implies that the indicators are reliable for measuring the variables and can be further tested in the structural (inner) model.

Table 1. Reliability & Validity of Variables

| Variable | Indicators | Code | Loading Coefficient | Composite Reliability | Cronbach Alpha | Average Variance Extracted | nbsp; |

| nbsp; | |||||||

| Social Capital | Involvement in community activities, associations or other activities (work related or neighborhood) | A1 | 0.737 | 0.821 | 0.728 | 0.481 | nbsp; |

| Relationship with the members of the community/association/ work/neighborhood | A2 | 0.687 | nbsp; | ||||

| Specific role in the community/association | A3 | 0.795 | nbsp; | ||||

| Network in social media | C2 | 0.61 | nbsp; | ||||

| General evaluation of current business network | C3 | 0.621 | nbsp; | ||||

| Economic Capital | Ownership of physical asset to run business | D1 | 0.798 | 0.872 | 0.837 | 0.5 | nbsp; |

| Size of the work team | D2 | 0.738 | nbsp; | ||||

| Business category growth | E1 | 0.526 | nbsp; | ||||

| Profitability of business | E2 | 0.574 | nbsp; | ||||

| Business financial management method | E3 | 0.784 | nbsp; | ||||

| Comparison of no of regular versus new customers | F1 | 0.653 | nbsp; | ||||

| Receive an award or achievement in business | F2 | 0.819 | nbsp; | ||||

| Cultural Capital | Enrolled in training (non formal education) for business | G3 | 0.71 | 0.801 | 0.705 | 0.408 | nbsp; |

| Have previous experience in business | H1 | 0.559 | nbsp; | ||||

| Experience in the current business | H2 | 0.72 | nbsp; | ||||

| Involvement in more than one business | H3 | 0.749 | nbsp; | ||||

| Self-evaluation of religiosity | I1 | 0.521 | nbsp; | ||||

| Physical evidence of a religious artifact | I2 | 0.528 | nbsp; | ||||

| Credit Potential | Evaluation of financial service utilization in business | X1 | 0.696 | 0.813 | 0.718 | 0.526 | nbsp; |

| Previous experience of an approved loan facility | X2 | 0.837 | nbsp; | ||||

| The time period of a previous credit loan facility | X3 | 0.775 | nbsp; | ||||

| Chance to apply for a new credit loan in the future | X5 | 0.565 | nbsp; |

Source: own compilation

4.3. Analysis of Inner Model & Hypotheses

Out of the three hypotheses, the data found support for two of the hypotheses:

− Economic Capital is proven to have a significant and positive effect on Credit Potential (T-Value = 3.101, ![]() =0.430) at a 95% confidence level (p-value = 0.05). The finding implies that when one's business economic capital is high, the more likely they have the experience and potential to be succeeded in the future loan application.

=0.430) at a 95% confidence level (p-value = 0.05). The finding implies that when one's business economic capital is high, the more likely they have the experience and potential to be succeeded in the future loan application.

− Cultural Capital is found to have a significant and positive effect on Credit Potential (T-Value= 1.720, ![]() =0.203) at a 90% confidence level (p-value = 0.1). Therefore, the higher the social capital of the applicant, the more likely they have the experience and potential for future loan applications, which made them a good candidate for a future loan.

=0.203) at a 90% confidence level (p-value = 0.1). Therefore, the higher the social capital of the applicant, the more likely they have the experience and potential for future loan applications, which made them a good candidate for a future loan.

− Social Capital hypothesis is not supported by data (T-Value=0.253, ![]() =-0.033). Interestingly, the study found that social capital does not have a significant effect on credit experience and potential. The social capital does not necessarily translate to a good previous loan experience and potential for a future loan. The social capital is represented by the community activity and role in the family, while social media indicators have been eliminated due to insufficient reliability in the previous stage

=-0.033). Interestingly, the study found that social capital does not have a significant effect on credit experience and potential. The social capital does not necessarily translate to a good previous loan experience and potential for a future loan. The social capital is represented by the community activity and role in the family, while social media indicators have been eliminated due to insufficient reliability in the previous stage

Analysis of the R-square of the model found that the three forms of capital explain 32.9 percent of the occurrence of credit potential, while the rest is explained by other factors. The summary of hypotheses result can be found in the following table.

Table 2. Summary of Hypotheses Result

| Indicators | Coefficient Loading | T Value | Conclusion | nbsp; |

| nbsp; | ||||

| H1: Social Capital has a significant and positive effect on Credit Potential | -0.033 | 0.253 | Not supported | nbsp; |

| H2: Economic Capital has a significant and positive effect on Credit Potential | 0.43* | 3.101 | Supported | nbsp; |

| H3: Cultural Capital has a significant and positive effect on Credit Potential | 0.203* | 1.72 | Supported | nbsp; |

| *at a 90 % level of confidence | nbsp; | |||

Source: own compilation

5. Conclusion

Microfinance is crucial for the growth and development of micro, small, and medium enterprises, especially in emerging countries. Nevertheless, it still faces many challenges. One of the challenges is how to widen access to financial support by providing assessment for credit loan potential. The aims of the current study are to find an alternative measure of credit potential for micro and small business owners borrowers. The theoretical framework that the study use is three forms of capital, namely economic capital, the cultural capital and social capital. After investigating 100 respondents the study arrived at the conclusion that the Economic Capital is having positive and medium effect to the Credit Potential. This is as expected, since economic capital has always been the main basic assessment for the potential of credit worthiness of a business. Surprisingly, social capital is not proven to be effective to measure credit scoring. This is different from a study conducted by Lee and Hallak (2020) which stated that social capital is integral to entrepreneurial success as it will open access to financial, marketing, and human resources, and innovation. Similarly, study by Tahmasebi and Azkaribesayeh (2020) concludes microfinance initiative in form will trigger community social interaction thus increasing the social capital. In the same study it also found that cultural capital such as educational level has no impact on the project. The explanation might be due to different contexts and types of entrepreneurs leading to the discussion. The current study is investigating e-entrepreneurs (online) while Tahmasebi and Azkaribesayeh (2020) analysis is based on the offline entrepreneurs. Supporting study found that online vs offline entrepreneurs have different traits (Yakub, Noor and Jamal, 2020).

Despite the contradiction, the study has found interesting findings which give theoretical and managerial values. In addition, limitations also exist and are further explained along with future research suggestions.

5.1. Theoretical Contributions

The study provides at least two theoretical contributions. First, the study is deriving the alternative measures of utilizing the framework of three forms of capital at the same time the study provides support to previous literature. Second, the study validates the relationship with the variable of credit potential. In addition, the tool also has the novelty by incorporating unique measures of social media activity, non-formal education, and religiosity in social capital and cultural capital, respectively.

Conceptualizing the literature, the cultural capital's measurement consists of three parts to measure: educational level, business knowledge, and the religiosity of the applicant. The study revealed that the indicators that are proven to be valid and reliable are the ones measuring business experience and religiosity. Interestingly, there is one indicator of education which refers to the non-formal education experience. The findings are in line with the study by Gallagher (2001). The study found that in the context of the agribusiness industry, the experience of the lenders' managers matters to the success of a loan application. The Cultural Capital items in this study have also incorporated the religiosity aspect into its measurement. The validated measurement of the cultural capital by religiosity is in line with the research by Chen et al. (2016) which found that religious diversity contributes to further reducing the cost of debt and stronger religiosity is also related to other favorable terms in loan contracting.

This study also confirmed that the data processed does not support the Social Capital to have any significant effect on the Credit Potential. Previous research showed that the effect of social capital on loan repayment vary according to the social-cultural context (Dufhues, Buchenreider, Quoc and Munkung, 2011). The fact that it is not proved to be a significant factor in this research might show that the social capital construct might not yet be suitable to predict Credit Potential in the context of a small business entrepreneur in Indonesia.

5.2. Managerial Implications

The study findings provide implications that can be addressed in the practice world. In evaluating an applicant for a micro and small business loan, it is important to take into consideration not only the economic capital form but also the cultural capital as a factor in assessing a credit applicant. Specifically, the cultural capital can be examined from a perspective of education level, business experience, and also religiosity.

5.3. Limitation and Future Research

There are limitations to this study. Firstly, a limitation is the development of indicators that need refinement to produce better indicators of each form of capital. If it is possible, a qualitative study is needed to be conducted to explore more on the forms of capital to highlight more comprehensive indicators for future research. Secondly, the current study has no criteria for an industry or business line investigated. It is suggested to investigate a specific industry or separating the service vs. goods-producing business. It is suspected that the result might be different, especially for social capital forms.

Similarly, the findings’ generalizability might be limited only for a similar context country, especially regarding the cultural part where religiosity is still the main cultural aspect and plays a significant role in the nation’s life. Future research might have different outcomes, based on each culture in a specific area. Lastly, the model only succeeds to explain partial variance of the credit potential. There are still other factors that might have affected the credit potential of an e-entrepreneur. Certain factors can be internal such as different typologies of e-entrepreneurs. Lee and Hallak (2020) differentiates between e-entrepreneurs characteristics regarding their social activities, such as Active Online Networkers, In-Person Networkers, and the Less Engaged. Future studies can explore each of the types and their relevance towards this avenue for additional research.

References

- Anderson, A. R. and Miller, C. J., 2003. “Class matters”: Human and social capital in the entrepreneurial process. The journal of socio-economics, 32(1), pp.17-36. doi:10.1016/S1053-5357(03)00009-X

- Bourdieu, P., 2010. The forms of capital., 1986. Szeman, I., Kaposy, T. (eds) Cultural Theory: An Anthology, 1, pp.81-93, London, UK: Wiley-Blackwell.

- Chen, H., Huang, H. H., Lobo, G. J. and Wang, C., 2016. Religiosity and the cost of debt. Journal of Banking & Finance, 70, pp.70-85. doi:10.1016/j.jbankfin.2016.06.005

- Chen, X., Zhou, L. and Wan, D., 2016. Group social capital and lending outcomes in the financial credit market: An empirical study of online peer-to-peer lending. Electronic Commerce Research and Applications, 15, pp.1-13. doi:10.1016/j.elerap.2015.11.003

- Daniel, B., and Grissen, D., 2015. Behavior revealed in mobile phone usage predicts loan repayment. Department to Economics, Brown University, Working Paper [online] Available at: doi:10.2139/ssrn.2611775 [Accessed on 11 February 2021].

- Dellien, H. and Schreiner, M., 2005. Credit scoring, banks, and microfinance: balancing high-tech with high-touch. Microenterprise Development Review, 8(2).

- Dufhues, T., Buchenrieder, G., Quoc, H. D. and Munkung, N., 2011. Social capital and loan repayment performance in Southeast Asia. The Journal of Socio-Economics, 40(5), pp.679-691. doi:10.1016/j.socec.2011.05.007

- Fisher, R., Maritz, A. and Lobo, A., 2014. Evaluating entrepreneurs’ perception of success: Development of a measurement scale. International Journal of Entrepreneurial Behavior & Research, 20(5), pp.478-492. doi:10.1108/IJEBR-10-2013-0157

- Gallagher, R.L., 2001. Characteristics of unsuccessful versus successful agribusiness loans. Agricultural Finance Review, 61(1), pp.20-35. doi:10.1108/00214730180001114.

- Hair Jr, J. F., Hult, G. T. M., Ringle, C. and Sarstedt, M., 2016. A primer on partial least squares structural equation modeling (PLS-SEM). London, UK: Sage Publications.

- Ibtissem, B. and Bouri, A., 2013. Credit risk management in microfinance: The conceptual framework. ACRN Journal of Finance and Risk Perspectives, 2(1), pp.9-24.

- Karlan, D. and Zinman, J., 2011. Microcredit in theory and practice: Using randomized credit scoring for impact evaluation. Science, 332(6035), pp.1278-1284. DOI: 10.1126/science.1200138

- Kasemsap, K., 2018. Exploring the Role of Microfinance in Emerging Nations. In Financial Entrepreneurship for Economic Growth in Emerging Nations, pp. 174-193. IGI Global. DOI: 10.4018/978-1-5225-2700-8.ch009

- Lai, L. S. and To, W. M., 2020. E-Entrepreneurial intention among young Chinese adults. Asian Journal of Technology Innovation, 28(1), pp.119-137.

- Lee, C. and Hallak, R., 2020. Investigating the effects of offline and online social capital on tourism SME performance: A mixed-methods study of New Zealand entrepreneurs. Tourism Management, 80, 104128.

- Malhotra, M., 2018. Role of Microfinance in Financial Inclusion in India. In Das, R.C. (ed) Microfinance and Its Impact on Entrepreneurial Development, Sustainability, and Inclusive Growth, pp. 322-343. IGI Global. DOI: 10.4018/978-1-5225-5213-0.ch018

- Masyutin, A. A., 2015. Credit scoring based on social network data. Business Informatics, 3(33), pp. 15- 23.

- Maxwell, J. A., 2008. Designing a qualitative study. The SAGE handbook of applied social research methods, 2, pp.214-253.

- Ntwiga, D. B. and Weke, P., 2016. Consumer lending using social media data. International Journal of Scientific Research and Innovative Technology, 3(2), pp.1-8.

- Serrano-Cinca, C., Gutiérrez-Nieto, B. and Reyes, N. M., 2013. A Social Approach to Microfinance Credit Scoring. Working Papers CEB, 13.

- Siva, W., 2010. Business intelligence and predictive analytics for financial services. The untapped potential of soft information. Center for digital innovation, technology, and strategy, School of Business, University of Maryland.

- Shosha, B., 2014. Profitability of Small and Medium Enterprises in Albania (Focusing in the City of Tirana. Journal of Educational and Social Research, 4(6), 546. DOI: 10.5901/jesr.2014.v4n6p546

- Tahmasebi, A. and Askaribezayeh, F., 2020. Microfinance and social capital formation-a social network analysis approach. Socio-Economic Planning Sciences, 100978.

- Wei, Y., Yildirim, P., Bulte, C., and Dellarocas, C., 2015. Credit scoring with social network data. Marketing Science, 35(2), pp. 1-25. doi:10.1287/mksc.2015.0949

- Vigerland, L. and Borg, E. A., 2017. Cultural Capital in the Economic Field: A Study of Relationships in an Art Market. Philosophy of Management, pp.1-17. doi:10.1007/s40926-017-0061-2

- Yaakub, N. A., Nor, K. M. and Jamal, N. M., 2020. Online versus offline entrepreneur personalities: A review on entrepreneur performance. International Journal of Advanced Science and Technology.

Article Rights and License

© 2021 The Author. Published by Sprint Investify. ISSN 2359-7712. This article is licensed under a Creative Commons Attribution 4.0 International License.