KeywordsSmall Businesses sustainability Sustenance framework

JEL Classification L20, M10, M20

Full Article

1. Introduction

Small businesses are of paramount importance to the economies of countries’ around the world (Wiklund and Shepherd, 2005). Small businesses can take on the form of micro enterprises, small enterprises and medium enterprises – often abbreviated as MSMEs, SMMEs, or SMEs (Bruwer, 2016). Before expanding on the latter, it should be noted that the term “small business” has various definitions. Based on the work of Hollander, small businesses are “those enterprises, which are involved in all or most of ... business functions and decisions ... which do not exceed a [certain] size which, concerning the nature of the business, permits personalized management by one or few executives” (Hollander, 1967). In turn, Street and Cameron define a small business as “an independently owned and operated enterprise that is not dominant in its field or industry ... which has relatively fewer resources than other companies in its markets” (Street and Cameron, 2007). From these definitions, the inference can be made that a small business is a privately owned entity, which can operate in various industries while being owned and/or managed by at least one natural person.

Small businesses are also directly associated with the discipline of entrepreneurship; as built on the creative response theory. The discipline of entrepreneurship is defined as the study surrounding “the creation of new business enterprises by individuals ... with the entrepreneur assuming the role of society’s major agent of change, initiating the industrial progress that leads to wider cultural shifts” (Kent et al., 1982). Moreover the creative response theory, as developed by the economist and political scientist, Joseph Schumpeter in 1947 (Bruwer and Van Den Berg, 2017), suggested that innovation is critical “whenever the economy ... do[es] something else, something that is outside of the range of existing practice, we may speak of creative response ... [it] changes social and economic situations for good ... it creates situations for which there is no bridge to those situations that might have emerged in its absence ... and [it is] coterminous with a study of entrepreneurship” (Schumpeter, 1947). To this end, it becomes apparent that small businesses, through the power of innovation, have the potential to make a significant socio-economic impact in the areas in which they operate.

To place the above inferences in perspective, since the start of 2010, globally, small businesses have been reported to make up at least 90% of all businesses in operation (Hayder and Lussier, 2016; Rikhardsson and Dull, 2016; Sellitto et al., 2016; Ward and Rhodes, 2014). Using the foregoing as a basis, it is not surprising that small businesses have been reported to contribute significant socio-economic value to the national economies in which they operate; including inter alia contributing to national Gross Domestic Products (GDP), assisting with the equal dissemination of wealth and the alleviation of poverty (Bruwer and Vand Den Berg, 2017; Turyakira et al., 2019). In core, the International Monetary Fund estimates the most recent global GDP at US$80.935 trillion (IMF, 2020); research suggests that small businesses are responsible for contributing at least 33% of this amount (Williams and Horodnic, 2016). In terms of employment, research shows that small businesses are responsible for 70% of global employment opportunities created (Jimenez et al., 2020). Notwithstanding the aforementioned, small businesses around the world suffer from high failure rates (Ayandibu et al., 2019). This view is substantiated by small business failure statistics for a few countries evident in Table 1 below.

Table 1. Small Business Failure Rates (prior to COVID19).

| Country | Failure rate | Source |

| Canada |

More than 66.67% within their first 10 years of operation. |

Le and Needham (2019) |

| China |

Approximately 50% within their first five years of operation |

Sidek et al. (2019) |

| India |

More than 90% within their first three years of operation. |

Kumar (2019) |

| New Zealand |

Approximately 50% within their first five years of operation |

Ward (2020) |

| South Africa |

Approximately 75% within their first three years of operation. |

Bruwer et al. (2020) |

| United States of America |

Approximately 90% within their first five years of operation. |

Mukherjee and Hollenbaugh (2019) |

| European Union countries |

Approximately 50% within their first five years of operation. |

European Union (2007) |

The statistics in Table 1 above speak to the observation that almost all newly established small businesses, on average, have an expected lifespan that ranges between three years and five years before they fail (Mabunda and Chinomona, 2019; Makwi, 2019). Over the years, reasons for the high small business failure rate have been pinned on internal factors (Internal factors are those factors that are within the control of management to manage (Franco and Haase, 2010), for example, lack of basic business skills, lack of financing, and having limited resources) and external factors (External factors are those factors that are not within the control of management to manage (Franco and Haase, 2010), for example supply and demand, harsh economic environments (the term “economic environment” refers to the overall well-being of a country’s economy (Guilhoto et al., 2002)), volatile interest rates, crime, taxation, protests, and changes in legislation) (Denton, 2020; Karanovic et al., 2019; Masama and Bruwer, 2018; Akaeze and Akaeze , 2017; Crutzen, 2010). Prior research suggests that although small businesses are affected by similar external factors, it is internal factors that most adversely affect their sustainability (Li and Zheng, 2017; Kennedy et al., 2006). For the sake of clarity, the term sustainability pertains to a business’ ability to meet responsibilities for its people (its stakeholders), the planet (the environments which it affect), and its profit (the attainment of economic objectives) (Beattie, 2019; Spiliakos, 2019; Bruwer and Coetzee, 2016).

Regardless of the foregoing, almost nothing has improved in terms of small business failure rates over the past two decades (Amankwah et al., 2019). Two prominent aspects for the latter dispensation, as contained in two theories, may be the reason why small business failure rates have not improved. First, newly established small businesses generally have a limited reputation (related to trust and loyalty), due to inherent limitations. Because of the latter, it makes matters difficult for newly established small businesses to conduct business and become sustainable (the liability of newness). Lastly, small businesses tend to undergo isomorphic change to become like other established businesses. Among the change small businesses undergo is that of mimetic isomorphic change – small businesses generally adopt a copy-and-paste approach by implementing “best practices” from at least one established business, as-is, to perform relevant business operations without testing its feasibility (the neo-institutional theory).

Stemming from the above, two questions arise, namely 1) “How can newly established small businesses build their reputation despite their inherent limitations?”, and 2) “How can small businesses limit the adverse influence from copying-and-pasting best practices without testing their feasibility?”. Particularly for this study, the primary aim was to ascertain whether the two prominent aspects contained in the two theories can be addressed by a newly developed framework, namely the Sustenance Framework, at least in a theoretical dispensation.

The Sustenance Framework comprises six inter-related steps – “Foundation”, “Pillars”, “Radar”, “Control”, “Sharing” and “Reviewing” – that assist small businesses with step-by-step guidance to fortify their sustainability (Bruwer, 2021). Essentially, if small business sustainability can be enhanced, it may lead to added socio-economic value to be generated in economies around the globe – allowing for the reduction of unemployment, the dissemination of wealth, and the eradication of poverty.

For the remainder of this paper, relevant discussions take place under key headings. First, the research design followed in this study is covered after which the theoretical framework of this study is provided. Here, discussions cover the liability of newness, the neo-institutional theory, as well as the Sustenance Framework. Afterwards, the theoretical framework is discussed in depth to address the primary aim of the study, from where it is concluded. In the conclusion, propositions for further empirical testing are provided.

2. Research Design

This study was exploratory as it pertained to the exploration of new ideas and insights on which little and/or no prior research has been conducted (Leedy and Ormrod, 2010; Collis and Hussey, 2009). Moreover, this study was nascent as the primary aim of this study is synonymous with “topics [that] have attracted little research or formal theorizing to date ... they [are] represent[ative of] net phenomena in the world (Cristofaro, 2020; Edmondson and McManus, 2007).

Furthermore, this study took on the form of a conceptual paper; defined as “a paper which [contains] content [that] is mostly discursive and develop[s] hypotheses based on comparative studies or others’ work of previous studies” (Mulatiningsih, 2017). One of the biggest pros of a conceptual paper is its “focus on integration and proposing new relationships among constructs” (Gilson and Goldberg, 2015). Notwithstanding the latter, such papers should ideally take on a problem-based-focus that contains fresh perspectives (with identified relationships between theories and/or phenomena) while still having relevance (Cropanzano, 2009). Despite the pros of conceptual papers, a major limitation of a conceptual paper is the aspect of generalisability – the pragmatic usefulness of findings in specific environments (Hubbard et al., 1998). If properly addressed, however, generalisability may open up avenues for further research, be it empirical or non-empirical (Hanafizadeh et al., 2020).

Since the primary aim of this study was to conceptualise how the Sustenance Framework can address two prominent aspects contained in two theories to, in turn, enhance small business sustainability, while also considering the fact that this study was exploratory, a conceptual paper best suited this study‘s research design. Throughout this study, how literature was sourced was through means of searching academic databases for keywords – separately and/or combined – such as “neo-institutional theory”, “small business”, “newly established small business”, “small businesses”, “sustainability”, and “liability of newness”. In core, this research study serves as a foundation for future empirical research to be conducted in the sense that evidence was provided on the theoretical feasibility of using the Sustenance Framework to address the sustainability concerns of newly developed small business entities.

3. Conceptual Framework

For the remainder of this section, relevant discussion takes place under the following three sub-headings: 1) liability of newness, 2) neo-institutional theory, and 3) the Sustenance Framework.

3.1. Liability of Newness

During the course of the mid-1960s, the liability of newness was developed by Arthur Stinchcombe (Abatecola et al., 2012). This phenomenon pertains to the observation that newly established business entities have a higher tendency to fail when compared to established business entities (Soto-Simeone. 2020). The latter is primarily attributable due to newly established businesses having: 1) limited existing and/or potential clients, 2) limited resources (e.g. human resources, financial resources and physical resources) on hand, 3) diverse internal stakeholders with different views when compared to the vision, and 4) to develop and implement new roles and tasks (Josefy et al., 2017; Odell and Spielman, 2009). The foregoing, in turn, directly affects a business’ reputation - comprising loyalty and trust (Ettenson and Knowles, 2008; Yoon et al., 1993) – and ultimately the manner in which the business achieves its relevant objectives (Lines, 2004; Gambetta, 1998).

According to recent studies (Partanen and Goel, 2017; Parente et al., 2015) small businesses are, by default, often perceived as not-credible and non-reputable. Reasons for the latter dispensation pertain to small businesses not always being creditworthy, not always possessing trusting entrepreneurial traits such as resilience (O’Toole and Ciuchta, 2019; Korber and McNaughton, 2018), and having little or no track record [portfolio] of work that has been successfully completed on behalf of its clients (Winborg, 2015). Another prevailing reason as to why small businesses are negatively perceived is due to their high failure rate – the longer a small business exist, the better the perception associated with the small business becomes (Dele-Ijagbulu et al., 2020; Prieto et al., 2020).

To this end, it becomes apparent that apart from facing “standard” internal factors and external factors, small businesses are disadvantaged due to the negative perceptions coupled to them. In the same vein, it also becomes apparent that if small businesses can remain in operation for an extended period of time, they will be perceived as better credible and better reputable.

3.2. Neo-Institutional Theory

In the early-1980s Paul DiMaggio and Walter Powell developed the neo-institutional theory (DiMaggio and Powell, 1983). This theory holds relevance to the observation that every business entity, though unique, undergoes change to become like other business entities while being influenced by similar external forces (Suddaby, 2010; Hu et al., 2007). This change comprises three stages of isomorphism, namely: 1) normative isomorphism (brought about by professional standards and/or networks, for example, accountants, lawyers, doctors, engineers and architects), coercive isomorphism (brought about by institutions on which business entities directly and/or indirectly rely on, for example, government departments, government agencies, and community agencies), and 3) mimetic isomorphism (brought about by uncertainty and/or desire, for example, trends set by established business entities, and practices instilled by competitors) (Benders et al., 2006; Haveman, 1993).

Among the three isomorphic changes, business entities undergo, newly established business entities are more susceptible to mimetic isomorphism (Lehner and Harrer, 2019; Haunschild and Miner, 1997). This view is supported by at least one study where it was found that newly established business entities imitate “best practices” as instilled by established/successful business entities rather than following a “trial-and-error” approach (Mähönen, 2020).

With small business management generally managing from the top-down (Spady and Clark, 1989; Fayol, 1937), is it not surprising that stakeholders rely on management to give guidance by setting a clear “tone at the top” (Ramutsheli and Janse van Rensburg, 2015). Such guidance directly affects business’ ability to achieve its relevant objectives (Edwards, 2018; Mbalamula et al., 2017; Heames, 2010; Yoo et al., 2006Wren et al., 2002). Considering that a business is a vivid and clear reflection of its management (Bruwer and Coetzee, 2018; Bruwer, 2016; Gerber, 1995), while keeping in mind that many small businesses reply on a “copy-and-paste approach” surrounding best practices, it becomes evident that such an approach may result in the business losing its identification; leading it to fail.

According to recent studies (Kesore, 2020; Lévesque and Shepherd, 2004) small businesses, world-wide, actively copy-and-paste selected practices and procedures from established businesses without considering it influence on operations. Probable reasons as to why small businesses do so include the increasing of its competitive edge (Cooper and Crowther, 2008), the modernisation of its operations (Sebestyén, 2016; Csaszar and Siggelkow, 2010), and the reduction of uncertainty caused by crises (Kern, 2013). Considering the fact that business processes and business practices of established businesses are customized to achieve their relevant objectives (Parthasarathy and Sharma, 2014), it is almost certain that a copy-and-paste approach adopted by small businesses will result in failure. This view is supported by Csaszar and Siggelkow through the following direct quote: “As firms copy more practices [and procedures] from each other, strategic convergence ensues, decreasing differentiation among firms, increasing competition, and consequently leading to profit erosion ... while held up in the industry as “key success factors” [it] may not be economically viable” (Csaszar and Siggelkow, 2010).

3.3. The Sustenance Framework

Using the above as a foundation, it is not surprising that international studies found that: 1) newly established businesses are often perceived as not-credible or non-reputable (Partanen and Goel, 2017; Parente et al., 2015), and 2) globally, small businesses are actively copying selected practices from established businesses without considering their fit in their own operations (Kesore, 2020; Cooper and Crowther, 2008; Lévesque and Shepherd, 2004). Considering that these prominent aspects highlighted above are current realities in small businesses, further exploration on how to mitigate their adverse influence on small business sustainability is justified; one of which is the Sustenance Framework.

The Sustenance Framework was developed by Juan-Pierré Bruwer during 2020 in an attempt to provide reasonable assurance to small business management surrounding the attainment of objectives (Bruwer, 2021). The Sustenance Framework was developed after discovering one major inherent limitation in the Committee of Sponsoring Organisations (COSO) Integrated Internal Control Framework (Bruwer, 2020), namely that there is no measurement tool to ascertain the “tone at the top” in a business entity.

This inherent limitation was investigated by making use of the first two steps of the Control Legacy-K (CLK) Framework (Bruwer, 2016); later becoming the Foundation of the Sustenance Framework. Specifically, the first two steps of the CLK Framework was found to adequately cover the definition of the control environment – better known as the “tone of the top” set by management (Bruwer et al., 2019). Considering that a business is a vivid and clear reflection of its management (Gerber, 1995), it is not surprising that the “tone at the top”, as set by management, serves as the foundation of any system of internal control (COSO, 2013). A system of internal control is defined as a comprehensive system, consisting of various elements, that provides management with reasonable assurance surrounding the attainment of a business entity’s objectives in the foreseeable future (Spira and Page, 2003).

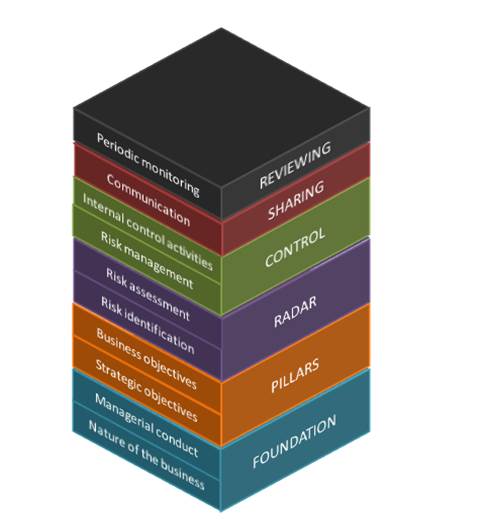

The Sustenance Framework, a newly developed internal control framework, guides small business management, in a step-by-step approach, to ascertain:

- Why the business exists and how the business is managed (Foundation).

- What the business’ objectives are (Pillars).

- What imminent risks the business faces to achieve its objectives (Radar).

- How these risks will be prevented and detected (Control).

- How the above information needs to be communicated with stakeholders (Sharing).

- When the entire process needs to be reviewed (Reviewing).

Though this Framework is related to the COSO Integrated Internal Control Framework, the Sustenance Framework is more feasible for small businesses due to the manner in which the “tone at the top” can be assessed, while also providing hands-on guidance on how to establish a system of internal control (Bruwer, 2021; Bruwer, 2020). In quintessence, considering the latter, the Sustenance Framework may be suitable to assist small businesses to build their reputation, while simultaneously addressing the copy-and-paste pitfall of mimetic isomorphic change. The Sustenance Framework is depicted in Figure 1, after which each of its components is discussed in more depth.

Figure 1. The Sustenance Framework

Source: Bruwer (2021).

Foundation: This is the first component of the Sustenance Framework. Here, the emphasis is placed on understanding the nature of the business (for example, the industry(ies) in which it operates, the location(s) where it operates, and the markets which it serves), as well as the managerial conduct (for example, the core values of management, and the manner in which management manages). In core, the bigger picture for starting the business is gleaned, as well as how business operations take place; as influenced by the managerial conduct of management.

Pillars: The second component builds on the Foundation as it entails the development of relevant objectives. This includes strategic objectives (for example, vision and mission), including business objectives (for example, operational objectives, reporting objectives, social objectives, and compliance objectives).

Radar: Following suit, this component builds forth on the Pillars. Here, relevant risks which may hamper the attainment of relevant strategic objectives and business objectives are first identified, and then assessed in terms of frequency and potential impact.

Control: With the Radar in place, the next component allows for the mitigation of risks that were identified and assessed. This takes place through risk management initiatives (for example, sharing, avoiding, and accepting) and the implementation of proper internal control activities (for example, preventive controls, detective controls, and corrective controls).

Sharing: With the “blueprint” in place - stemming from the previous four components - relevant information can be communicated with internal stakeholders and/or external stakeholders. Such communication needs to take place to allow relevant stakeholders to perform applicable tasks to, in turn, contribute towards the attainment of strategic objectives and business objectives.

Reviewing: Periodically, it is recommended that every component of the Sustenance Framework is reviewed. This is especially the case in events where, inter alia, the business expands, objectives are achieved, and new management comes on board.

Notwithstanding the above, it is worth noting that, over the years, researchers have investigated how managers can best execute their controlling-function (Griffin, 2013). The four functions of management pertain to the planning-function, organising-function, directing-function, and controlling-function (Griffin, 2013). In quintessence, this function has to do with the manner in how management maintains, improves and monitors business processes to provide reasonable assurance regarding the attainment of objectives in the foreseeable future (Schermerhorn, 2013). The controlling-function of management is by no means an easy task to execute, especially considering that limited principles are attached to it (Koontz, 1959). More often than not these principles pertain to characteristics of good corporate governance which include that of discipline, transparency, independence, accountability, responsibility and fairness (Idowu et al., 2015; Njegomir and Tepavac, 2014)

Therefore, it is not surprising that a primary challenge of properly executing the control-function has to do with the controlling of people (i.e. internal stakeholders) who, in turn, may affect the efficiency of business processes, as well as the reputation of a business entity; directly or indirectly (Dolphin, 2004; Louisot, 2004). This better explains the need for internal control systems, especially since they have been found to curb both reputational risks and operational risks in established business entities (Gatzert and Schmt, 2020; D’Aquila and Hournes, 2014; Soin and Collier, 2013).

4. Discussion

The importance of small businesses, to economies around the world, rest in the significant socio-economic value they add (Turyakira et al., 2019; Bruwer and Van Den Berg, 2017; Wiklund and Shepherd, 2005). Essentially, the socio-economic value added by these businesses, to the global GDP, is estimated at US$26.71 trillion (IMF, 2020); simultaneously providing employment opportunities that are equivalent to 70% of all employment opportunities worldwide (Jimenez et al., 2020). Notwithstanding the foregoing, unfortunately, small businesses have been found to suffer from high failure rates - a great proportion failing between three and five years (Mabunda and Chinomona, 2019; Makwi, 2019).

In China, New-Zealand and European countries, 50% of small businesses have been found to fail within their first five years of existence (Ward, 2020; Sidek et al., 2019); 75% small businesses in South Africa have been found to fail within their first three years of existence (Bruwer et al., 2020). In turn, 66.67% of Canadian small businesses fail after their first 10 years of operation (Le and Needham, 2019); 90% of Indian small businesses fail after their first three years of operation (Kumar, 2019); 90% of small businesses in the United States of America fail after their first five years of operation (Mukherjee and Hollenbaugh, 2019). These high failure rates, as reported on before COVID19 (Perold et al., 2020), have not improved notably over the past two decades (Amankwah-Amoah et al., 2019), though they are constantly blamed on harsh economic environments (Akaeze and Akaeze, 2017) that have their own subsequent economic factors and political factors (Denton, 2020; Karanovic et al., 2019; Masama and Bruwer, 2018; Crutzen, 2010). Therefore, the focus was shifted to two theories to better understand the high small business failure rates, namely the liability of newness, and the neo-institutional theory.

When placing emphasis on the liability of newness, the notion exists that small businesses fail due to having limited reputation (comprising loyalty and trust) (Ettenson and Knowles, 2008; Lines, 2004; Gambetta, 1998; Yoon et al., 1993). The latter may stem from small businesses having: 1) limited clients (potential and/or existing), 2) limited resources on hand, 3) diverse internal stakeholders with differing views, and 4) new roles and/or tasks that have to be implemented (Josefy et al., 2017; Odell and Spielman, 2009). Then, based on the neo-institutional theory, small businesses strive to become like established businesses while operating in similar conditions (for example, harsh economic environments with their applicable economic factors and political factors) (Suddaby, 2010; Hu et al., 2007). To become like established businesses, small businesses undergo isomorphic change (Benders et al., 2006; Haveman, 1993) which are, more often than not, aligned towards mimetic isomorphism (Lehner and Harrer, 2019; Haunschild and Miner, 1997). Alternatively stated, small businesses appear to imitate “best practices” by established businesses, as-is (copy-and-paste), without considering customized solutions using a “trial-and-error” approach (Mähönen, 2020).

Using the above as a basis, from the two theories, it becomes apparent that two pertinent aspects contribute towards small business failure rates, namely: 1) small businesses generally have limited reputation as they have not established sufficient loyalty and trust with stakeholders, and 2) in order for small businesses to perform their operations, most choose to adopt a copy-and-paste approach by implementing “best practices” from at least one established business without considering whether they are suitable fits. Reverting to the controlling function of management, it should be noted that it includes the controlling of internal stakeholders – people with feelings, thoughts and ambition (Koontz, 1959). Though it is not possible to specifically measure (or manage) principles such as discipline, transparency, independence, accountability, responsibility and fairness (Idowu et al., 2015; Njegomir and Tepavac, 2014), internal stakeholders of a business entity will, most likely, always influence the efficiency of business processes, including its reputation (Dolphin, 2004; Louisot, 2004). Therefore, to address the two identified aspects of limited reputation and “copying-and-pasting” practices, the Sustenance Framework is suggested (Bruwer 2021; Bruwer, 2020).

The aspect of limited reputation may be addressed through ascertaining the bigger picture as to why the business was started (nature of the business) and how the business is managed (managerial conduct), as well as what the business strives to achieve (strategic objectives, and business objectives). With all of the latter phenomena in alignment, small businesses will be able to better convince a prospective client(s) to do business with them – related to the characteristics of transparency, and integrity. In turn, the aspect of “copying-and-pasting” may be addressed by the same phenomena mentioned above (nature of the business, managerial conduct, strategic objectives, and business objectives) as small businesses form their own unique identity by understanding why they were started, how it is managed, and what it wants to achieve.

Using the above as a basis, the envisioned result of using the Sustenance Framework include that clear direction will be provided to small business management (and relevant stakeholders) about, inter alia, expectations, objectives, managerial conduct, risks affecting the objectives, and controls that combat risks. Moreover, particularly amidst (and after) COVID-19, the Sustenance Framework may prove useful to business entities, especially existing small businesses, that need restructuring (e.g. change of objectives, operations and/or managerial operating styles) to better accommodate for change.

5. Conclusion

Worldwide, small businesses are of paramount socio-economic importance. Not only do these businesses contribute towards national GDPs; they also assist in the alleviation of poverty and the dissemination of wealth through the creation of employment opportunities. Unfortunately, the failure rate of small businesses leaves much to be desired as a large proportion fails after being in existence for between three and five years. Though research suggests that harsh economic environments, and subsequent economic- and political factors are to blame for the latter dispensation, these same reasons are still applicable nearly two decades after being first identified.

To this end, in this conceptual paper, two theories were discussed, namely the liability of newness, and the neo-institutional theory. In quintessence, these two theories give rise to pertinent aspects that may contribute towards high small business failure rates, namely: 1) small businesses generally have limited reputation, and 2) for small businesses to perform their operations, most choose to adopt a copy-and-paste approach by implementing “best practices” from at least one established business, as-is. These observations were justified by studies where it was found that small businesses, by default, are often perceived as not-credible and non-reputable (due to not being creditworthy, not possessing trusting entrepreneurial traits, having little or no track record of completed work, and their high failure rates), and small businesses worldwide blatantly copy-and-paste practices and processes from established businesses (to have a competitive edge, to modernize operations, and to overcome uncertainties) without considering their fit.

Using the above as a basis, it became apparent that small businesses: 1) could decrease the liability of newness by remaining in operation for an extended period of time, and 2) require their own unique practices and processes that speak to the achievement of their relevant objectives. The latter can be addressed by implementing the Sustenance Framework. In layperson’s terms, this framework provides clear direction to small business management on expectations, customized objectives that should be achieved, and how these customized objectives should be achieved. In turn, this framework allows for the building of a sound reputation while limiting the adverse influence of mimetic isomorphism.

Although the Sustenance Framework has not yet been empirically tested, it may have both theoretical implications and practical implications when implemented in small businesses. Theoretically, the Sustenance Framework may become a viable tool to address the pitfalls of the liability of newness and mimetic isomorphism (as contained in the neo-institutional theory). In a practical dispensation, the Sustenance Framework may [will] allow small businesses to develop customized objectives which can be achieved through customized business process and business practices which, in turn, can allow them to remain in operation for the foreseeable future. In addition to the above, small businesses that have already started their operations can make use of the Sustenance Framework to re-evaluate the nature of their business, especially in relation to the viability and feasibility of offering particular products and/or services amidst (and post) COVID-19.

In fundamental nature, from the theoretical evidence provided the Sustenance Framework, if used by newly established small businesses, may enhance their sustainability, while also addressing the aspect of limited reputation and the aspect of “copying-and-pasting” of business practices. To better understand the feasibility of the Sustenance Framework, in an empirical dispensation, further research is suggested on, inter alia, the influence of the Sustenance Framework on small business reputation-building, and the influence of the Sustenance Framework on the attainment of economic objectives.

References

- Abatecola, G., Cafferata, R. and Poggesi, S., 2012. Arthur Stinchcombe’s “liability of newness”: contribution and impact of the construct. Journal of Management History, 18(1), pp. 402 – 418.

- Akaeze, N.S. and Akaeze, C., 2017. Exploring the survival strategies for small business ownership in Nigeria. Australian Journal of Business and Management Research, 5(1), pp. 35 - 48.

- Amankwah-Amoah, J., Hinson, R.E., Honyenuga, B. and Lu, Y., 2019. Accounting for the transitions after entrepreneurial business failure: An emerging market perspective. Structural Change and Economic Dynamics, 50(1), pp.148 - 158.

- Ayandibu, A.O., Ngobese, S., Ganiyu I.O. and Kaseeeram, I., 2019. Constraints that Hinder the Sustainability of Small Businesses in Durban, South Africa. Journal of Reviews on Global Economics, 8(1), pp.1402 - 1408.

- Beattie, A., 2019. The 3 Pillars of Corporate Sustainability [Online]. Available from: https://www.investopedia.com/articles/investing/100515/three-pillars-corporate-sustainability.asp [Accessed on 24/11/2019].

- Benders, J. Batenburg, R. and Van der Blonk, H., 2006. Sticking to standards; technical and other isomorphic pressures in deploying ERP-systems. Information and Management, 43(1), pp. 194 – 203.

- Bruwer, J-P. and Coetzee, P., 2016. A literature review of the sustainability, the managerial conduct of management and the internal control systems evident in South Africa small, medium and micro enterprises. Problems and Perspectives in Management, 14(1), pp., 201 - 211.

- Bruwer, J-P. and Van Den Berg, A., 2017. The conduciveness of the South African economic environment and small, medium and micro enterprise sustainability. Expert Journal of Business and Management, 5(1), pp. 1 - 12.

- Bruwer, J-P., 2016. The relationship(s) between the managerial conduct and the internal control activities of South African fast moving consumer goods SMMEs. Doctoral degree, Cape Peninsula University of Technology, Cape Town.

- Bruwer, J-P., 2020. Fortifying South African Small Medium and Micro Enterprise sustainability through a proposed internal control framework: The Sustenance Framework. Expert Journal of Business and Management, 8(1), pp. 147 – 158.

- Bruwer, J-P., 2021. The Sustenance Framework. New York: Nova Publishers.

- Bruwer, J-P., Beck, T. and Fourie, H., 2019. Considering the Control Legacy-K (CLK) Framework to serve as a basis for a mixed-method measuring instrument to assess the control environment of non-JSE listed business entities. Expert Journal of Business and Management, 7(1), pp. 271 - 279.

- Bruwer, J-P., Coetzee, P. and Meiring, J., 2018. Can internal control activities and managerial conduct influence business sustainability? A South African SMME perspective. Journal of Small Business and Enterprise Development, 25(1), pp. 710 - 729.

- Bruwer, J-P., Hattingh, C. and Perold, I., 2020. Probable measures to sustain South African Small Medium and Micro Enterprises' existence, post COVID19: A literature review. [Online]. Available from: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3625552 [Accessed on 16/11/2020].

- C.A. Kent, C.A., Sexton, D.L. and Vesper, K.H., 1982. Encyclopedia of entrepreneurship. University of Illinois at Urbana-Champaign’s Academy for Entrepreneurial Leadership Historical Research Reference in Entrepreneurship.

- Caratas, M.A. and Spatariu, E.C., 2014. Contemporary approaches in internal audit. Procedia Economics and Finance, 15(1), pp. 530-537.

- Collis J. and Hussey, R. 2009. Business Research: A Practical Guide for Undergraduate and Postgraduate Students. New York: PalgraveMacMillan.

- Cooper, S. and Crowther, D., 2008. The adoption of value‐based management in large UK companies. Journal of Applied Accounting Research, 9(1), pp. 148-167.

- COSO, 2013. Internal control – integrated framework: executive summary. [Online]. Available from: https://na.theiia.org/standards-guidance/topics/Documents/Executive_Summary.pdf [Accessed on 26/01/2021].

- Cristofaro, M., 2020. Unfolding irrationality: how do meaningful coincidences influence management decisions?. International Journal of Organizational Analysis. In press.

- Cropanzano, R., 2009. Writing nonempirical articles for Journal of Management: General thoughts and suggestions. Journal of Management, 35(1), pp. 1304 – 1311.

- Crutzen, N., 2010. The origins of small business failure: A Taxonomy of Five Explanatory Business Failure Patterns. Conférence annuelle de l' AIMS, 4 Dec 2010.

- Csaszar, A.F. and Siggelkow, N., 2010. How Much to Copy? The Contingent Value of Imitation Capabilities. Organization Science, 21(1). pp. 661 – 676.

- D’Aquila, J.M. and Hournes, R., 2014. COSO’s Updated Internal Control and Enterprise Risk Management Frameworks. The CPA Journal, 84(1), pp. 54 – 59.

- Dele-Ijagbulu, O., Moos, M. and Eresia-Eke, C., 2020. The Relationship Between Environmental Hostility and Entrepreneurial Orientation of Small Businesses. Journal of Entrepreneurship and Innovation in Emerging Economies, 6(1), pp. 347 - 362.

- Denton, A., 2020. Why Do Most Small Businesses in Liberia Fai. Open Journal of Business and Management, 8(1), pp.1771 - 1815.

- DiMaggio, P.J. and Powell, W.V. 1983. The iron cage revisited: Institutional isomorphism and collective rationality in organizational fields. American sociological review, 48(1), pp. 147 - 160.

- Dolphin, R.R., 2004. Corporate reputation – a value creating strategy. Corporate Governance, 4(1), pp. 77 - 92.

- Edmondson, A.C. and McManus, S.E., 2007. Methodological fit in management field research. Academy of Management Review, 32(1), pp. 1246 - 1264.

- Edwards, R., 2018. An Elaboration of the Administrative Theory of the 14 Principles of Management by Henri Fayol. International Journal for Empirical Education and Research, 1(1), pp.41 - 51.

- Ettenson, R. and Knowles, J., 2008. Don't confuse reputation with brand. MIT Sloan Management Review, 49(1), pp.19 - 23.

- European Union, 2021. Communication from the Commission to the Council, the European Parliament, the European Economic and Social Committee and the Committee of the Regions - Overcoming the stigma of business failure – for a second chance policy - Implementing the Lisbon Partnership for Growth and Jobs [Online]. Available from: https://eur-lex.europa.eu/legal-content/EN/TXT/?uri=celex:52007DC0584 [Accessed on 12/01/2021]

- Franco, M. and Haase, H., 2010. Failure factors in small and medium-sized enterprises: qualitative study from an attributional perspective. International Entrepreneurship and Management Journal, 6(1), pp. 503 - 521.

- Gambetta, D., 1998. Trust: Making and breaking cooperative relations. Oxford, United Kingdom:Basil Blackwell Science.

- Gatzert, N. and Schmit, J., 2020. Supporting strategic success through enterprise-wide reputation risk management. Journal of Risk Finance, 17(1): 26 – 45.

- Gerber, M.E., 1995. The E-Myth Revisited: Why Most Small Businesses Don’t Work and What to do About it. New York: Collins Business.

- Gilson, L.L. and Goldberg, C.B., 2015. Editor’s Comment: So, What Is A Conceptual Paper?. Group and Organization Management, 40(1), pp. 127 – 130.

- Griffin, R.W., 2013. Fundamentals of management. Ohio: South-Western Cengage Learning.

- Guilhoto, J., Marjotta-Maistro, M. and Hewings, G., 2002. Economic Landscapes: What are They? An Application to the Brazilian Economy and to Sugar Cane Complex. Berlin: Springer.

- Fayol, H. 1937. The administrative theory in the state. Papers on the Science of Administration. Institute of Public Administration, New York, pp.99 - 114.

- Hanafizadeh, P., Khosravi, B. and Tabatabaeian, S.H., 2020. Rethinking dominant theories used in information systems field in the digital platform era. Digital Policy, Regulation and Governance.

- Haunschild, P.R. and Miner, A.S., 1997. Modes of interorganizational imitation: the effects of outcome salience and uncertainty. Administrative Science Quarterly, 42(1), pp. 472 – 500.

- Haveman, H.A., 1993. Follow the leader: Mimetic isomorphism and entry into new markets. Administrative Science Quarterly, 38(1), pp. 593 - 627.

- Heames, J., Pryor, M.G. and Taneja, S., 2010. Henri Fayol, practitioner and theoretician–revered and reviled. Journal of Management History, 16(1), pp. 489 – 503.

- Heaton, J., 2003. Secondary data analysis. The AZ of Social Research. London, UK: Sage.

- Hollander, E.D., 1967. In The Future of Small Business. New York: Preager Publishers.

- Hu, Q., Hart, P. and Cooke, D., 2007. The role of external and internal influences on information systems security – a neo institutional perspective. Journal of Strategic Information Systems, 16(1), pp. 153 – 172.

- Hubbard, R., Vetter, D.E. and Little, E.L., 1998. Replication in strategic management: Scientific testing for validity, generalizability, and usefulness. Strategic Management Journal, 19(1), pp. 243 - 254.

- Hyder, S. and Lussier, R.N., 2016. Why businesses succeed or fail: a study on small businesses in Pakistan. Journal of Entrepreneurship in Emerging Economies, 8(1), pp. 82 - 100.

- Idowu, S.O., Frederiksen, C.S., Mermod, A.Y. and Nielsen, M.E.J., 2015. Corporate social responsibility and governance. Cham: Springer, 2015.

- IMF., 2020. GDP, current prices [Online]. Available from: https://www.imf.org/external/datamapper/NGDPD@WEO/OEMDC/ADVEC/WEOWORLD [Accessed 16/11/2020].

- Jimenez, W.P., Xu, X., Campion, E.D. and Bennett, A.A., 2020. Takin' Care of Small Business: The Rise of Stakeholder Influence. Academy of Management Perspectives, 10(1), in press.

- Josefy, M., Harrison, J., Sirmon, D. and Carnes, C., 2017. Living and dying: Synthesizing the literature on firm survival and failure across stages of development. Academy of Management Anals, 11(1), pp. 770 – 799.

- Karanović, B., Nikolić, G. and Karanović, G., 2019. Examining financial management practices in the context of smart ICT use: recent evidence from Croatian entrepreneurs. Zagreb International Review of Economics and Business, 22(1), pp.107 - 123.

- Kennedy, J., Tennent, B. and Gibson, B., 2006. Financial management practices in small businesses: regional and metropolitan. Small Enterprise Research, 14(1), pp. 55 - 63.

- Kern, P., 2013. Institutional Change After the Global Financial Crisis: Why a Whimper, Not a Bang?. SASE 25th Annual Conference, 27-29 June, 2013.

- Kesore, L.V., 2020. Sustainability reporting in the airline industry: a comparative case study analysis of four selected European passenger airlines and their countries of registration on the basis of the airlines’ annual reports and sustainability report from 2018. Master’s degree, University of Twente, Haaksbergen, Netherlands.

- Koontz, H., 1959. Management Control: A Suggested Formulation of Principles. California Management Review, 1(1), pp. 47 – 55.

- Korber, S. and McNaughton, R., 2018. Resilience and entrepreneurship: a systematic literature review. International Journal of Entrepreneurial Behavior Research, 24(1), pp. 1129 - 1154.

- Kumar, M., 2019. A study on startup in India: Issues, challenges and opportunities by government policies. Doctoral degree, Jayoti Vidyapeeth Women’s University, Jaipur, India.

- Le, P.N. and Needham, C.R., 2019. Factors Contributing to the Success of Ethnic Restaurant Businesses in Canada. Open Journal of Business and Management, 7(1), pp.1586 - 1609.

- Leedy, P. and Ormrod, J., 2010. Practical Research – Planning and Design. New York: Pearson.

- Lehner, O.M. and Harrer, T., 2019. Crowdfunding revisited: a neo institutional field-perspective. Venture Capital, 21(1), pp.75 - 96.

- Lévesque, M. and Shepherd, D.A., 2004. Entrepreneurs' choice of entry strategy in emerging and developed markets. Journal of Business Venturing, 19(1), pp.29 - 54.

- Li, Z. and Zheng, X., 2017. A Critical Study of Commercial Banks’ Credit Risk Assessment and Management for SMEs: The Case of Agricultural Bank of China. Journal of Applied Management and Investments, 6(1), pp.106 - 117.

- Lines, V.L., 2004. Corporate reputation in Asia: Looking beyond bottom-line performance. Journal of Communication Management, 8(3), pp. 233 - 245.

- Louisot, J-P., 2004. Managing Intangible Asset Risks: Reputation and Strategic Redeployment Planning. Risk Management, 6(1), pp. 35 – 50.

- Mabunda, T. and Chinomona, R., 2019. Enterpriseneurship: A Solution to Small Business Failure and Enterprise Development in South Africa. Journal of African Problems and Solutions, 1(1), pp.1 - 37.

- Mähönen, J., 2020. Comprehensive approach to relevant and reliable reporting in Europe: A Dream impossible?. Sustainability, 12(1), pp. 5277 – 5314.

- Makwi, C., 2019. Factors affecting SMEs growth in Tanzania: A case study of selected SMEs in Dar es Salaam. Doctoral degree, Mzumbe University, Mzinga, Tanzania.

- Masama, B. and Bruwer, J-P., 2018. Revisiting the Economic Factors which Influence Fast Food South African Small, Medium and Micro Enterprise Sustainability. Expert Journal of Business and Management, 6(1), pp.19 – 28.

- Mbalamula, Y.S., Suru, M.H. and Seni, A.J., 2017. Utility of Henri Fayol’s fourteen principles in the administration process of secondary schools in Tanzania. International Journal of Education and Research, 5(1), pp. 103 - 116.

- Mbandlwa, Z. and Dorasamy, N., 2020. The impact of substance abuse in South Africa: a case of informal settlement communities. Journal of Critical Reviews, 7(1), pp. 1 - 15.

- Mensah, B.E., 2011. Assessing the effectiveness of internal control systems in public institutions: a case study of Takoradi Polytechnic. Master’s degree, Kwame Nkrumah University of Science and Technology, Ashanti, Ghana.

- Mukherjee, D. and Hollenbaugh, E.E., 2019. Do social media help in the sustainability of small businesses? A pedagogical study using fictional business cases. International Journal of Higher Education Management, 6(1), pp. 1 - 9.

- Mulatiningsih, B., 2017. # networkedLISprofessionals: Library and information science professionals' experience of social media. Doctoral degree, Queensland University of Technology, Queensland, New Zealand.

- Njegomir, V. and Tepavac, R., 2014. Corporate governance in insurance companies. Management, 71, pp. 81 - 95.

- O’Toole, J. and Ciuchta, M.P., 2019. The liability of newer than newness: aspiring entrepreneurs and legitimacy. International Journal of Entrepreneurial Behavior and Research, 26(1), pp. 539-55.

- Odell, C. and Spielman, C., 2009. Global Positioning: Managing the Far-Reaching Risks of an International Assignment Program. Benefits Quarterly, 25(1), pp. 23 - 29.

- Parente, R. Feola, R. Cucino, V. and Catolino, G., 2015. Visibility and reputation of new entrepreneurial projects from academia: The role of start-up competitions. Journal of the Knowledge Economy, 6(1), pp. 551-567.

- Partanen, J. and Goel, S., 2017. Interplay between reputation and growth: the source, role and audience of reputation of rapid growth technology-based SMEs. Entrepreneurship and Regional Development, 29(1), pp. 238 - 270.

- Parthasarathy S. and Sharma, S., 2014. Determining ERP customization choices using nominal group technique and analytical hierarchy process. Computers in Industry, 65(1), pp.1009 - 1017.

- Perold, I., Hattingh, C. and Bruwer, J-P., 2020. The Forced Cancellation of Four Jewel Events Amidst COVID19 and Its Probable Influence on the Western Cape Economy: a Literature Review [Online]. Available from: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3604132 [Accessed on 16/11/2020].

- Prieto, F. Sarabia, J.M. and Calderín-Ojeda, E., 2020. The risk of death in newborn businesses during the first years in market [Online]. Available from: arXiv preprint arXiv:2011.11776 [Accessed on 06/12/2020].

- Ramutsheli, M.P. and Janse van Rensburg, J.O., 2015. The root causes for local government's failure to achieve objectives. Southern African Journal of Accountability and Auditing Research, 17(1), pp.107 - 118.

- Rikhardsson, P. and Dull, R., 2016. An exploratory study of the adoption, application and impacts of continuous auditing technologies in small businesses. International Journal of Accounting Information Systems, 20(1), pp.26 - 37.

- Schermerhorn, J.R., 2013. Introduction to management. Hoboken, New Jersey: John Wiley.

- Schumpeter, J.A., 1947. The creative response in economic history. Journal of Economic History, 7(1), pp.149-159.

- Sebestyén, D., 2016. Something old, Something new, Something borrowed. Master’s degree, Copenhagen Business School, Denmark.

- Sellitto, C., Banks, D., Bingley, S. and Burgess, S., 2016. Small Businesses and Effective ICT: Stories and Practical Insights. London, UK: Routledge.

- Sidek, S., Mohamad, M.R. and Mohd, W.M.N.W., 2019. Sustaining Small Business Performance: Role of Entrepreneurial Orientation and Financial Access. International Journal of Academic Research in Business and Social Sciences, 9(1), pp. 66 - 80.

- Soin, K. and Collier, P., 2013. Risk and risk management in management accounting and control. Management Accounting Research, 24(1), pp. 82 – 87.

- Soto‐Simeone, A., Sirén, C. and Antretter, T., 2020. New venture survival: A review and extension. International Journal of Management Reviews, 22(4), pp.378-407.

- Spady, R.J. and Clark, R.W. 1989. Democratic Strategic Planning: Democratic Strategic Planning in Schools through Inclusive Small-Group Discussions Using Many-to-Many Communication Technology. Annual Meeting of the American Educational Research Association, California.

- Spiliakos, A., 2019. What does “Sustainability” means in Business? [Online]. Available from: https://online.hbs.edu/blog/post/what-is-sustainability-in-business [Accessed on 24/11/2019].

- Spira, L.F. and Page, M., 2003. Risk management: the reinvention of internal control and the changing role of internal audit. Accounting, Auditing and Accountability Journal, 16(1), pp. 640 - 661.

- Street, C.T. and Cameron, A.F., 2007. External relationships and the small business: A review of small business alliance and network research. Journal of Small Business Management, 45(1), pp.239-266.

- Suddaby, R., 2010. Challenges for institutional theory. Journal of Management Inquiry, 19(1), pp. 14 - 20.

- Turyakira, P., Kasimu, S., Turyatunga, P., and Kimuli, S.N., 2019. The joint effect of firm capability and access to finance on firm performance among small businesses: A developing country perspective. African Journal of Business Management, 13(1), pp.198 - 206.

- Ward M. and Rhodes C., 2014. Small businesses and the UK economy. Standard Note: SN/EP/6078. Office for National Statistics.

- Ward, D., 2020. The Perceived Importance of the Changing Political Environment on SME Market Entry: New Zealand SMEs Entering the United States. Doctoral degree, Auckland University of Technology, Auckland, New Zealand.

- Wiklund, J. and Shepherd, D., 2005. Entrepreneurial orientation and small business performance: a configurational approach. Journal of Business Venturing, 20(1), pp.71 - 91.

- Williams, C.C. and Horodnic, I.A., 2016. Cross-country variations in the participation of small businesses in the informal economy. Journal of Small Business and Enterprise Development, 23(1), pp. 3 - 24.

- Winborg, J., 2015. The role of financial bootstrapping in handling the liability of newness in incubator businesses. The International Journal of Entrepreneurship and Innovation, 16(1), pp.197 - 206.

- Wren, D.A., Bedeian, A.G. and Breeze, J.D., 2002. The foundations of Henri Fayol’s administrative theory. Management Decision, 40(1), pp. 906 - 918.

- Yoo, J.W, Lemak, D.J. and Choi, Y., 2006. Principles of management and competitive strategies: using Fayol to implement Porter. Journal of Management History, 12(1), pp. 352 - 368.

- Yoon, E., Guffey, H.J. and Kijewski, V., 1993. The effects of information and company reputation on intentions to buy a business service. Journal of Business Research, 27(1), pp. 215 - 228.

Article Rights and License

© 2021 The Authors. Published by Sprint Investify. ISSN 2359-7712. This article is licensed under a Creative Commons Attribution 4.0 International License.